JGBS: Cash Bonds Little Changed Out To 20Y But Richer Beyond

In Tokyo morning trade, JGB futures are slightly weaker, -9 compared to settlement levels.

- Today, the local calendar will see IP and Capacity Utilisation data alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

- Headlines have crossed following US and Japan issuing a joint statement on FX. Japanese officials noted that the joint statement came out in the aftermath of settling the trade deal. At face value, the headlines from the statement on FX look to largely reaffirm what both sides already broadly agree to on FX markets. FX markets should be market-determined and that manipulating exchange rates for competitive purposes should be avoided. Domestic policies on monetary and fiscal policy should also not be geared towards driving FX rates.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest post-CPI gains.

- Cash JGBs are little changed across benchmarks out to the 20-year but 1-2bs richer beyond. The benchmark 10-year yield is 0.2bp higher at 1.583% versus the cycle high of 1.649%.

- Swap rates are 1-2bps higher. Swap spreads are wider.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

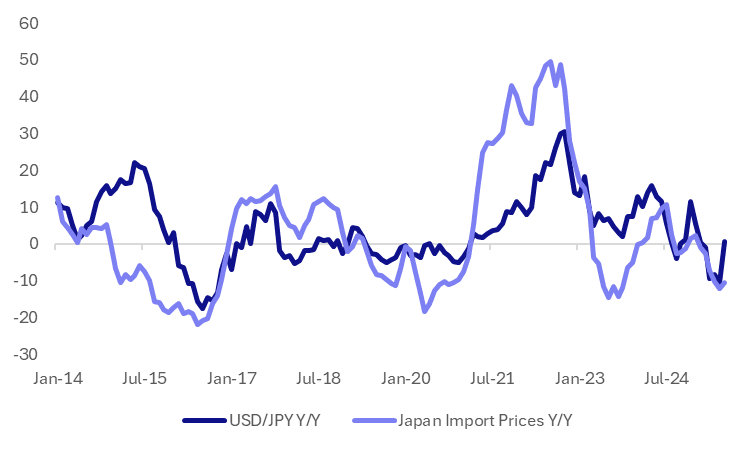

JAPAN DATA: Import Prices Up For First Month Since Jan, Y/Y Still Negative

For July, export and import prices both rose in m/m terms. Export prices were up 1.6%, while import prices were up 2.4%m/m. For import prices this was the first m/m rise since January of this year. In y/y terms, both export and import prices were still in negative territory, but up from the June levels. Export prices were -5.4%y/y, while imports were -10.4%.

- The chart below plots y/y changes in USD/JPY versus import prices y/y. To end July USD/JPY was up a touch in y/y terms. If current spot levels prevail, (currently around 147.80), USD/JPY will remain positive in y/y terms to end September (note USD/JPY was 152.03 end Oct last year).

- This implies some upside to import price y/y momentum in the near term, albeit fairly modestly. If USD/JPY holds around current level to end September, we would be up +2.9% in y/y terms.

Fig 1: Japan Import Prices & USD/JPY, Y/Y

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Dec-35 Supply Faces Lower Yield But Same Curve

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 9 July 2025 for A$1200mn. Bidding is likely to be shaped by several key factors:

- The current outright yield is 5-10bps lower than the previous auction and approximately 50bps lower than the peak in late 2024.

- The 3/10 yield curve is around the same level as the previous auction but sits around 20bps below its recent high.

- On the negative side, the auction comes amid weaker sentiment toward longer-dated global bonds.

- However, the line is included in the XM basket.

- While some factors may limit the overall strength of bidding, there is an expectation of continued firm pricing at today's auction.

- Results are due at 0200 BST / 1100 AEST.

AUSSIE BONDS: AUCTION PREVIEW: ACGB Dec-35 Supply Due

The Australian Office of Financial Management (AOFM) will today sell A$1200mn of the 4.25% 21 December 2035 bond. The line was last sold on 9 July 2025 for A$1200mn. The line was opened via syndication on 24 July 2024 for A$11.5bn.

- The last sale drew an average yield of 4.3442%, at a high yield of 4.3475% and was covered 2.6500x. There were 29 bidders, 16 of which were successful and 12 were allocated in full. The amount allotted at the highest yield as a percentage of the amount bid at that yield was 3.5%.

- This week's ACGB supply is at the top of the recent average weekly issuance of $1500-2200mn, with A$1000mn of the 2.75% 21 November 2029 bond due on Friday.

- During the first half of 2025-26, the AOFM plans to: issue a new October 2036 Treasury Bond (by syndication and subject to market conditions); conduct 2 Treasury Bond tenders most weeks; hold 1-2 Treasury Indexed Bond tenders each month.

- Issuance of Treasury Bonds (including Green Treasury Bonds) in 2025-26 is expected to be around $150 billion. Issuance of Treasury Indexed Bonds in 2025-26 is expected to be between $2 billion and $3 billion.

- Results are due at 0200 BST / 1100 AEST.