AUSSIE BONDS: Futures Higher, AU-US 10yr Spread Close To Multi Month Highs

Aussie bond futures continue to hold gain, but tight ranges have prevailed. Positive carry over from futures gains in the US and the EU look to be major driver today, while Q2 capex data locally was weaker than expected. 10yr futures (XM) were just off session highs, last 95.68, +3bps, while 3yr futures (YM) were at 96.585, +2bps.

- Cash ACGB yields are close to 3bps lower across the curve, with no standout outperformance. The 3yr yield was last around 3.39%, while the 10yr was near 4.29%. Both these benchmarks sit within recent ranges.

- The AU-US 10yr spread sits slightly lower around +7bps but is within the upper range seen in recent months. We have spent little time above +10bps going back to mid April of this year.

- On the data front, private sector capex remained soft in Q2 with volumes rising 0.2% q/q, driven by the non-mining sector, after falling 0.2% q/q to be up only 1.7% y/y although this was an improvement from Q1’s -0.6% y/y. There has been talk that investment needs to rise in order to see progress on productivity, which has been weak. Q2 GDP is released September 3 with inventories September 1, and net exports and public demand contributions September 2.

- Tomorrow we get July private credit figures.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - The USD Correction Could Have More To Go

The BBDXY has had a range of 1207.45 - 1208.74 in the Asia-Pac session, it is currently trading around 1208, +0.05%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. Yesterday's US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. There is lots of event risk coming up this week and we are heading into month-end so some caution is warranted, this could potentially see some more paring back of USD shorts. Today is corporate month-end and this could also add to some short-term USD demand putting further pressure on the shorts.

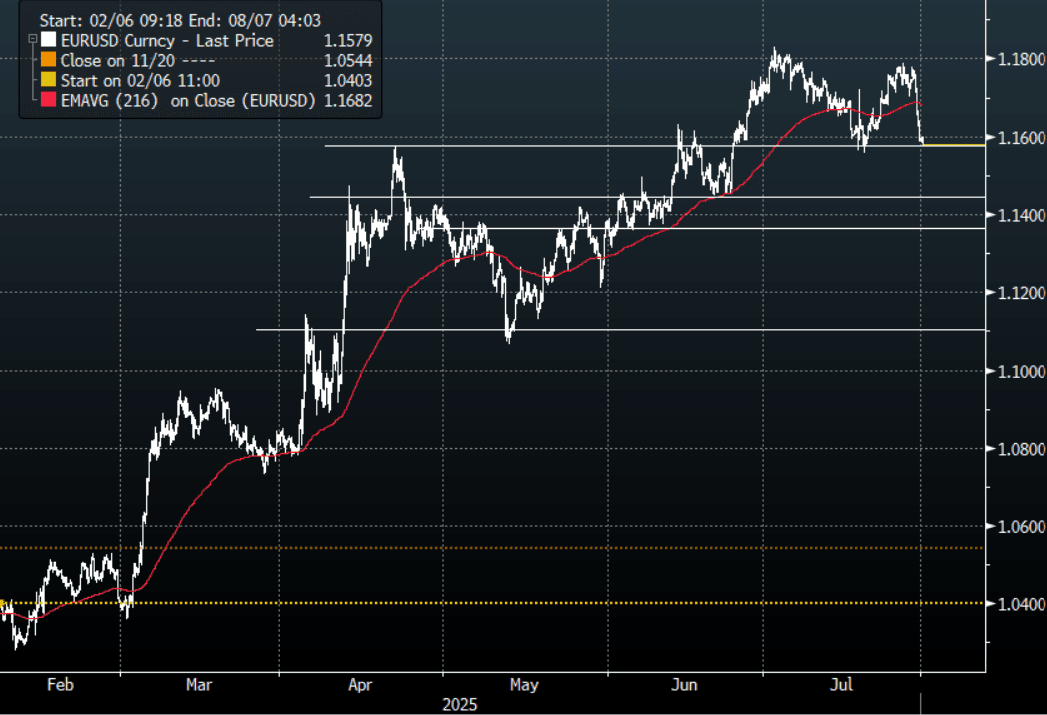

- EUR/USD - Asian range 1.1575 - 1.1599, Asia is currently trading 1.1580. The pair saw some heavy selling putting in a top towards 1.1800 for now. The price looked a little stretched in the short term, and with the USD making a recovery the EUR is set for a correction of sorts. First support around 1.1550 then the more important 1.1350/1.1450 area where I would expect demand first up.

- GBP/USD - Asian range 1.3337 - 1.3362, Asia is currently dealing around 1.3340. This pair looks like it is now breaking lower indicating a deeper correction. Support seen now back towards 1.3100/1.3200 and look for supply now on bounces back towards 1.3500.

- USD/CNH - Asian range 7.1775 - 7.1839, the USD/CNY fix printed 7.1511, Asia is currently dealing around 7.1800. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3311, US 10-Year 4.40%, BBDXY 1208, Crude oil $66.59

- Data/Events : Spain GDP & Retail Sales, EZ ECB 1&3 Year CPI Expectations, France Total Jobseekers

Fig 1: EUR/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

BUND TECHS: (U5) Candle Patterns Highlight A Potential Reversal

- RES 4: 131.33 High Jun 20

- RES 3: 130.85 61.8% retracement of the Jun 13 - Jul 14 bear leg

- RES 2: 130.17/76 50-day EMA / High Jul 22

- RES 1: 129.95 20-day EMA

- PRICE: 129.74 @ 05:30 BST Jul 29

- SUP 1: 128.84 Low Jul 25 and the bear trigger

- SUP 2: 128.40 Low Apr 9

- SUP 3: 128.19 Low Mar 27 (cont)

- SUP 4: 127.83 76.4% retracement of the Mar 11 - Apr 7 bull leg (cont)

Bund futures have recovered from last Friday’s 128.84 low. Friday’s activity resulted in a test of the base of a 3.5-month range at the 129.00 handle. This key support remains intact for now. A hammer candle formation on Jul 25 followed by a bullish engulfing candle yesterday signals a potential reversal of the recent downtrend.Initial resistance to watch is 129.95, the 20-day EMA. A break of the Jul 25 low is required to confirm a resumption of the bear trend.

BONDS: NZGBS: Closed At Bests But Only Modestly Richer

NZGBs closed at session bests, 2bps richer across benchmarks.

- The NZ-US 10-year yield differential finished 3bps tighter at +15bps.

- Swap rates closed 2bps lower.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- The local calendar will feature the release of ANZ business confidence for July tomorrow. It continues to point to a gradual recovery in the economy. Cost and price components remain elevated, and inflation expectations are at 2.7% off their low.

- ANZ July consumer confidence is out on Friday. It rose sharply in June to 98.8, the highest this year, but still off December's 100.2. Rate cuts, which take time to be reflected in mortgage payments, have helped improve households' financial situations and reduced the time to buy component.

- June building permits will also be printed on Friday. They rose 10.4% m/m in May, and indicators suggest that the construction sector is recovering.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond.