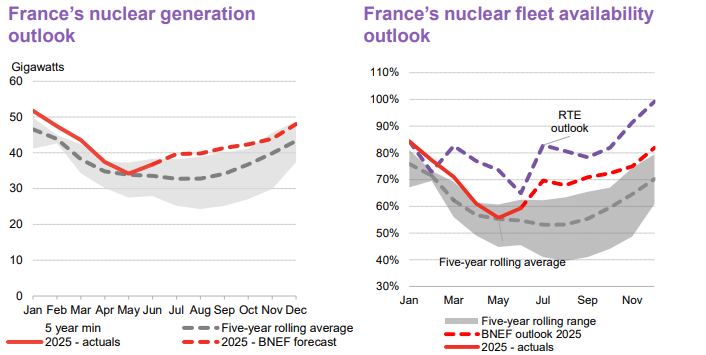

POWER: French Nuclear Generation to Rise to 39.7GW in July

French nuclear generation is forecast to average 39.7GW in July, up by 3GW from June with plants returning from seasonal maintenance according to BNEF.

- Nuclear generation is further forecast to average 39.5GW during summer, which would be higher year on year.

- However, hot weather-related curtailments could weigh on the forecast.

- EdF may face nuclear output restrictions at its 2.6GW Golfech nuclear complex starting on 29 June, at the 3.64GW Blayais complex from 29 June, at the 2.67MW St Alban plant from 1 July and at the 3.58GW Bugey complex from 27 June due to high river water temperatures, remit data showed.

- In winter 2025/26, nuclear generation is forecast to average 47.6GW.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/OVERNIGHT REPO: SOFR Ticks Up, Month-End Pressures To Spill Over Monday

Secured rates picked up again Friday, with SOFR up 2bp to 4.35%. That's the highest since the start of the month, with the rise at both ends of May reflecting month-end dynamics. Upside pressure is expected to persist Monday before subsiding over the rest of the week.

- Fed funds were unchanged as usual.

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 4.35%, 0.02%, $2641B

* Broad General Collateral Rate (BGCR): 4.34%, 0.02%, $1049B

* Tri-Party General Collateral Rate (TGCR): 4.34%, 0.02%, $1013Bd

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 4.33%, no change, volume: $105B

* Daily Overnight Bank Funding Rate: 4.33%, no change, volume: $228B

CANADA DATA: PMI Suggests Stagflationary Manufacturing Dynamics In May

The S&P Global Canada Manufacturing PMI saw a slight uptick to 46.1 in May from 45.3 prior. Despite the apparent stabilization in the headline reading, highlights from the report (link) suggest a stagflationary May for Canadian manufacturers:

- "Output and new orders both fell again, largely due to tariffs, whilst employment was reduced at the fastest rate in nearly five years. Confidence in the outlook remained subdued, and inflation rates picked up since April. Delays related to the delivery of inputs intensified and further inventory reductions were recorded."

- "Panellists widely blamed tariffs, noting an ongoing malaise in product markets with clients generally reluctant to commit to new contracts given the uncertainty of trade policies. International demand remained especially hard hit, with new export business again declining to a steeper degree than overall sales. Trade with the neighbouring United States was again reported to be weak."

- Meanwhile inflationary pressures remained acute:

- "Price data meanwhile showed an acceleration of input cost inflation. There was again evidence that tariffs had led to a general uplift in input costs, with vendors reportedly raising their charges....Overall, input price inflation was broadly in line with March’s 31-month peak. In response to rising input costs and tariff challenges, many firms saw little choice but to raise their own charges. Latest data showed a marked overall increase in output charges, despite the rate of inflation dropping to a three-month low. "

SWITZERLAND DATA: Focus On CHF Feedthrough, Housing & Travel Reversal [2/2]

- In April, Swiss CPI surprised notably to the downside as CHF valuations reached their highest levels since early 2024 in real trade-weighted terms, and volatile travel-related categories also had a negative impact in April. Against the backdrop of the Swiss Franc having pared some of that previous strength, a reversal here would appear possible - however, the beta and lag of Swiss CPI to CHF valuations differ across categories and can both be difficult to track down.

- Additionally, rents will see their quarterly update in May, and the Y/Y pace in the category has ticked down the last two quarters following lower mortgage reference rates.