COMMODITIES: Gold and Oil Gain Overnight

- As the President's tax bill passes through senate, the ever present fiscal concerns return to investors and fellow republicans thoughts. House Republicans are pushing back on the bill citing concerns over spending reductions and medicaid cuts and if at least three republicans do not support, the bill's passage through the House may not be assured.

- Fed Chairman Powell "Really Can't Say" If July Too Soon To Seriously Consider Cut. Fed Chair Powell speaking on an ECB forum panel asked if July is too soon to seriously consider a rate cut and he certainly doesn't categorially rule it out, even if it's couched in typical central bank-speak: "Yeah, I really can't say - it's going to depend on the data. And we are going meeting by meeting. I mentioned, you know, how I'm thinking about that, but I wouldn't take any meeting off the table or put it directly on the table, it's going to depend on how the data evolve."

- Powell's comments comes as the May JOLTS report saw stronger job openings than expected and other data points to stabilization of the labour market.

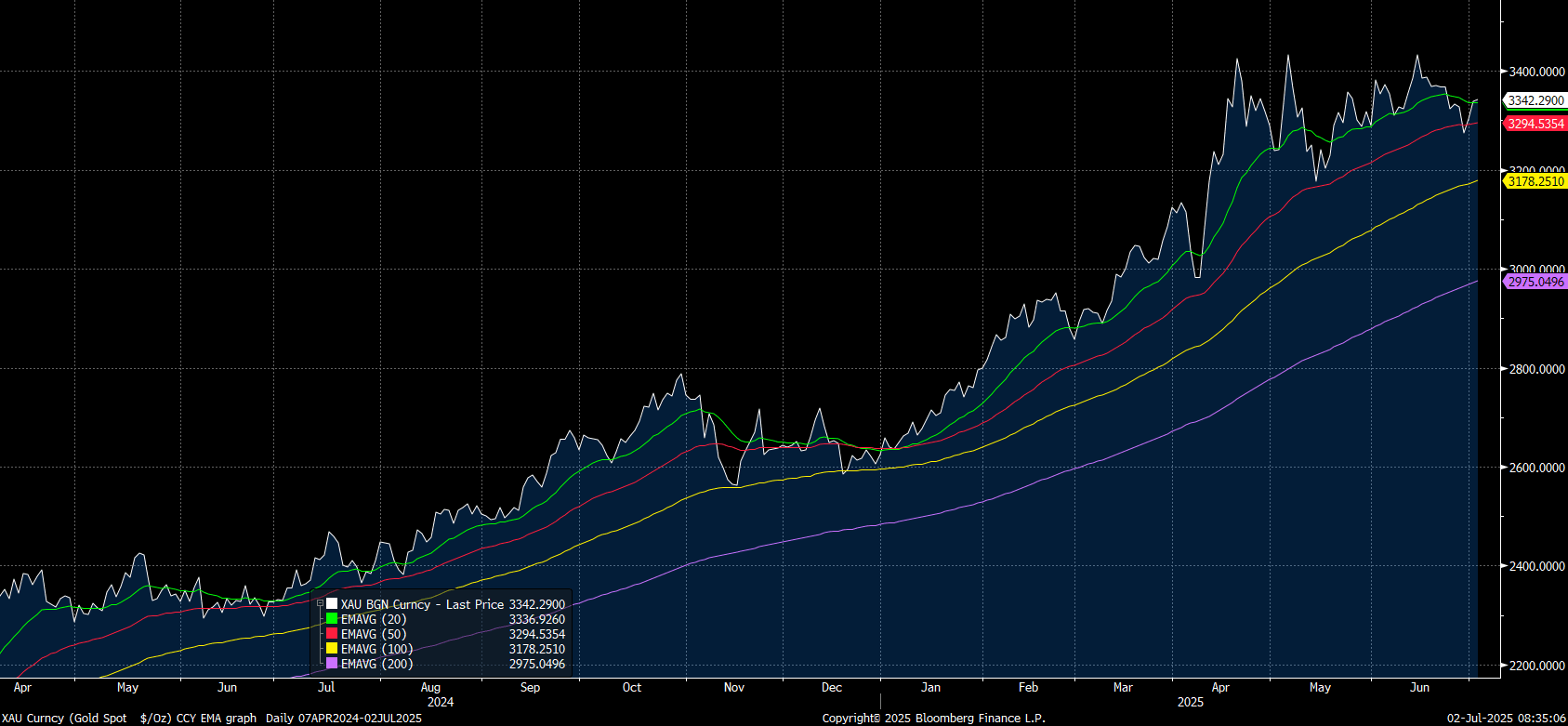

- The fiscal concerns were enough to give GOLD a boost and it finished the US session up +1.08% to a high of US$3,332.33, a bounce of over 3% from Friday's lows, before settling into the close at $3,338.84.

- The rally sees gold back above the 20-day EMA of $3,336.98, having briefly traded below the 50-day EMA on Friday.

Source: Bloomberg Finance LP / MNI

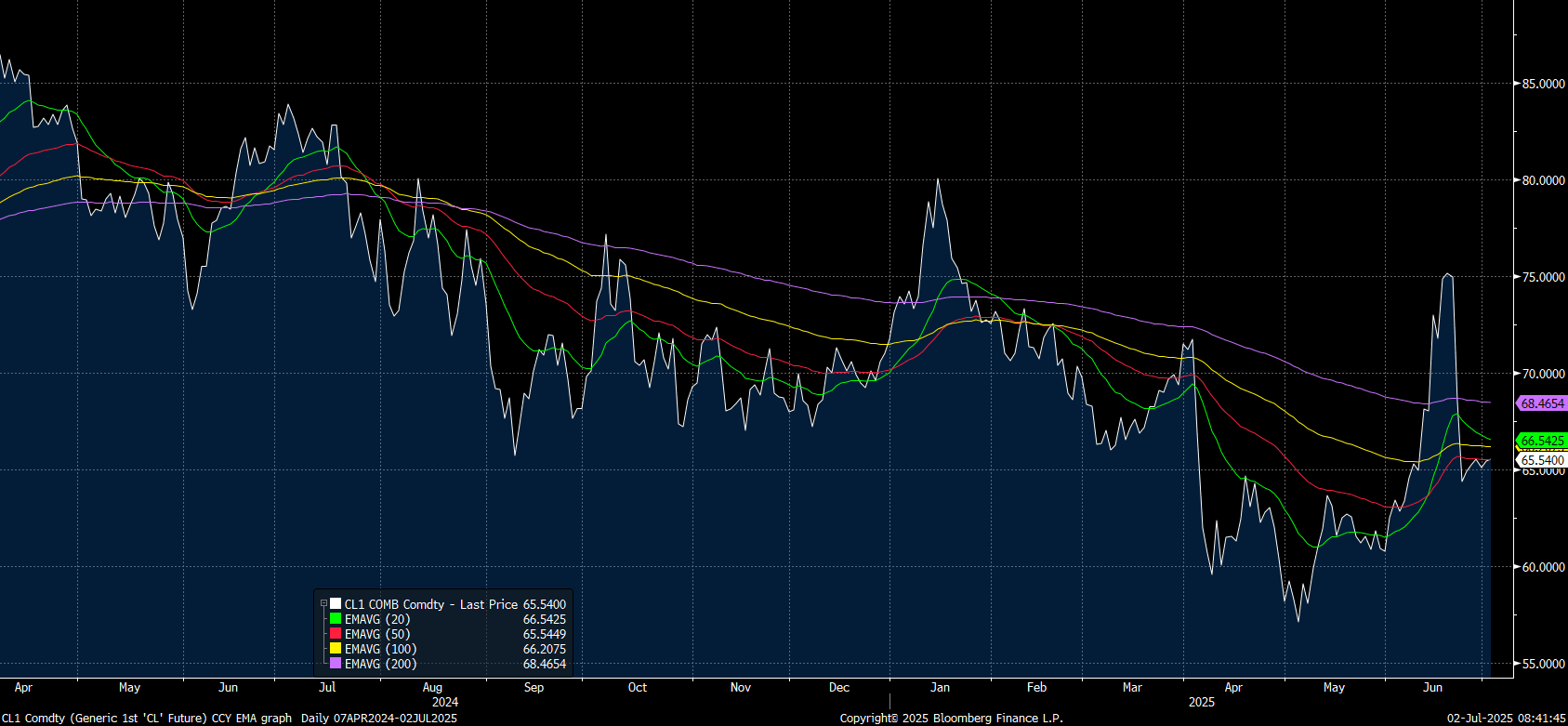

- Oil had a stronger night despite the expectations of a further increase in OPEC+ output in August as the market weighs the potential for stronger than expected demand given the heat experienced across most of Europe and the US.

- WTI finished in the US up at the end of the US session by +0.52% and is opening stronger in the Asia trading day. At US$65.54, WTI is attempting to break the 50-day EMA of $65.54 with the 100-day EMA above at $66.20

Source: Bloomberg Finance LP / MNI

- Brent closed out the US session down -0.74% at US$67.25 bbl to remain below all major moving averages.

- The IEA forecasts that global oil demand will rise by up to 2.5m barrels a day from 2024-2030 despite EV's forecasting to displace up to 5m barrels per day over the next decade.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: USD/JPY - Starts The Week Around 144.00

The Friday night range was 143.48 - 144.44, Asia is currently trading around 143.85. No real direction for USD/JPY on Friday as US stocks and bonds contended with month-end rebalancing and a rise in US-China tensions.

- Bloomberg - “Scott Bessent said he’s confident the latest trade clash between Trump and Xi Jinping “will be ironed out” in a call “very soon.” He also told CBS’s Face the Nation the US “is never going to default” on its debt, while declining to say when the Treasury will run out of cash.”

- “Pete Hegseth pressed Asian partners to boost defense spending toward 5% of GDP, warning at the Shangri-La Dialogue that more urgency is needed to prepare for a potential Chinese invasion of Taiwan. Beijing protested the comments, blaming the US for instability and saying it must “never play with fire.”(BBG)

- “Japan’s top trade negotiator Ryosei Akazawa said the latest round of discussions with the Trump administration on tariffs have them on track toward a deal as early as next month, while refraining from citing specifics.”(BBG)

- The market seems very confident of a move lower in USD/JPY but with positioning quite large now we have seen the risks of pullbacks increase. Resistance around the 146.00 area held perfectly last week and the JPY bulls would be quite relieved as well as vindicated by the price action. The next pivotal trigger points look to be below 140.00 on the downside and above 146.50 on the topside.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($670m). Upcoming Close Strikes : 140.00($1.88b June 5), 142.00($884m June 5).

- CFTC data shows Asset managers maintained their already extensive JPY longs, and leveraged funds reduced their longs that had just started to be built up.

Data/Event : Capital Spending, Jibun Mfg PMI

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg

JGB TECHS: (M5) Rallies Off Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 141.48/142.95 - High May 2 / High Apr 7

- PRICE: 139.20 @ 14:58 GMT May 30

- SUP 1: 138.54 - Low May 22

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have rallied off recent lows, however a bearish theme remains intact following the reversal that started Apr 7. A continuation lower would signal scope for an extension towards 136.57, a Fibonacci projection. On the upside, a reversal higher would instead refocus attention on 142.95, the Apr 7 high. The first important resistance to watch is 141.48, the May 2 high. A break of this level would be viewed as an early bullish signal.

AUSTRALIA: Q1 GDP On Wednesday, RBA Minutes Tuesday

The highlight of the week will be Wednesday’s Q1 GDP release but before then key components will be released on Tuesday. GDP is expected to rise 0.4% q/q to be up 1.5% y/y after 0.6% & 1.3% in Q4. Investment and real household consumption were little changed on the quarter.

- On Tuesday, the Q1 balance of payments data are released and include the net export contribution to GDP, which is forecast to be flat. Bloomberg consensus has the current account deficit steady at $12.5bn.

- Q1 company profits are also on Tuesday and projected to rise 1.3% q/q after 5.9%. Inventories are part of this data set and consensus has a 0.2% q/q rise after 0.1% in Q4.

- The public demand contribution to GDP is also out on Tuesday. It contributed 0.2pp to Q4 growth.

- The RBA minutes from the May meeting print on Tuesday. It cut rates 25bp at this meeting but no change and 50bp were also considered. Assistant Governor (Economic) Hunter speaks on Australia’s global linkages on Tuesday at 1305 AEST.

- Final S&P Global PMIs for May print this week with manufacturing on Monday and composite & services on Wednesday. Services moderated in the flash May release while manufacturing was stable.

- The May Melbourne Institute inflation gauge is released on Monday. In April it rose 0.6% m/m to be up 3.3% y/y.

- ANZ job ads for May are also out on Monday. They rose 0.5% m/m in April. The labour market remains tight.

- April household expenditure is published on Thursday and consensus expects it to rise 0.2% m/m leaving the annual rate at 3.5% y/y.

- April merchandise trade data are also Thursday and the surplus is forecast to narrow slightly to $6bn from $6.9bn.