STIR: Fed Terminal Yield Set For Lowest Close Since October With NFP Looming

Sep-04 17:31

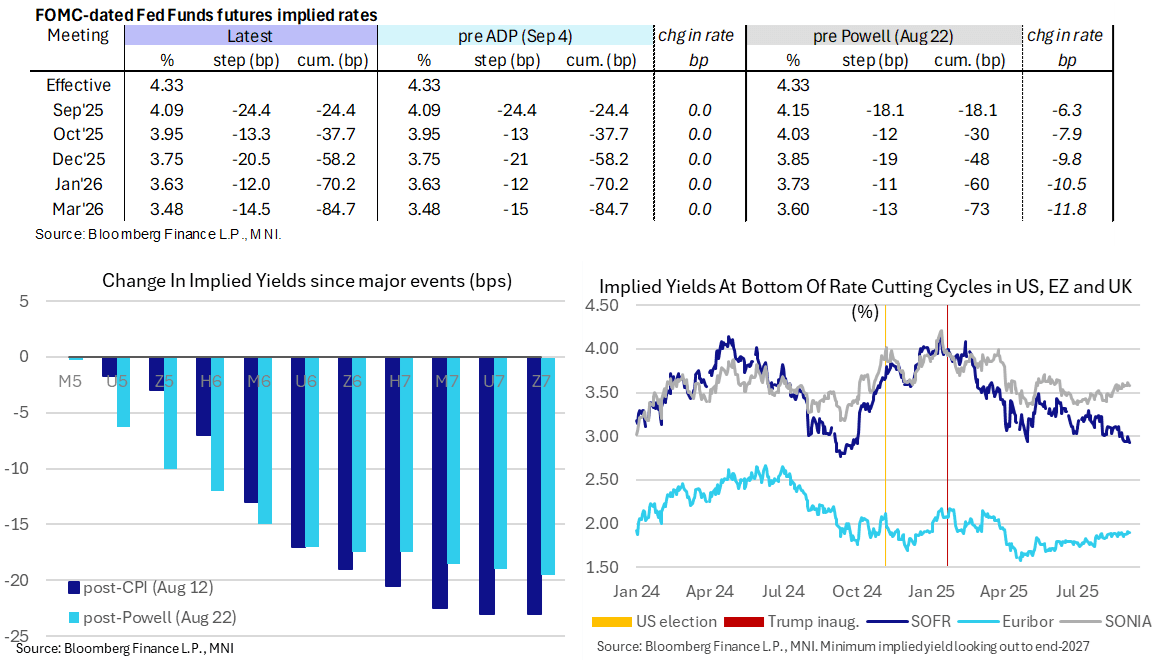

- Fed Funds implied rates for near-term meetings out to March are unchanged from levels prior to today’s main data releases, while SOFR futures hold a drift higher further out the curve.

- It’s sees near-term implied rates up to 2bp lower on the day having drifted lower pre-data.

- Cumulative cuts from 4.33% effective rate: 24.5bp Sep, 37.5bp Oct, 58bp Dec, 70bp Jan and 85bp Mar.

- SOFR futures are currently up to 4 ticks higher on the day out in 2027 contracts, close to session highs from late 2026 onwards.

- The SOFR implied terminal yield of 2.925% (SFRH7) Is 3.5bp lower on the day, set for a fresh lowest close since Oct 2024 with ~140bp of cuts priced from current levels.

- ADP employment, initial claims, ULCs and final service/composite PMIs were more dovish than expected to varying degrees whilst continuing claims and ISM services on the most part were stronger (lower in the case of claims).

- Tomorrow of course sees the August payrolls report – MNI Preview: https://mni.marketnews.com/3I3oEii

- Today’s lack of dovish reaction to an ADP miss (albeit not a large one) suggests there was already sizeable pessimism priced in but we still suspect risks are skewed towards a larger reaction in the event of a soft payrolls report, especially one where the unemployment rate pushes higher.

- Still to come today at 1900ET – Chicago Fed’s Goolsbee (’25 voter, dove) in moderated Q&A (text tbd, Q&A). Whilst historically one of the more dovish members on the FOMC, said on Aug 21 that he thought the rise in July services inflation was a “dangerous” data point that he hopes is just a blip. He thinks the current tariffs don’t look “one and done” whilst economic data more broadly are sending mixed messages.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Maintains A Softer Tone

Aug-05 17:30

- RES 4: 1.3681 High Jul 4

- RES 3: 1.3620 High Jul 10

- RES 2: 1.3448/1.3589 50-day EMA / High Jul 24

- RES 1: 1.3365 Low Jul 16

- PRICE: 1.3304 @ 16:47 BST Aug 5

- SUP 1: 1.3144 38.2% retracement of the Jan 13 - Jul 1 bull cycle

- SUP 2: 1.3041 Low Apr 14

- SUP 3: 1.3000 Round number support

- SUP 4: 1.2945 50.0% retracement of the Jan 13 - Jul 1 bull cycle

A bearish theme in GBPUSD remains intact for now - despite Friday’s rally. Last week’s sell-off resulted in a breach of the bear trigger at 1.3365, the Jul 16 low. The break confirms a resumption of the downleg that started Jul 1 and highlights a clear breach of the trendline drawn from the Jan 13 low. Sights are on 1.3144, a Fibonacci retracement, and 1.3041, the Apr 14 low. Firm resistance is 1.3448, the 50-day EMA. A break of this average is required to signal a reversal.

SOFR OPTIONS: Large Dec'25 SOFR Put Condor Spread & Midcurve Call Spread

Aug-05 17:24

- +20,000 SFRZ5 96.25/96.37/96.50/96.62 put condors vs. 95.75/95.87/96.00/96.12 put condor, .25 net

- -8,000 0QZ5 97.25/97.50 call spds, 5.62 ref 96.95

US TSYS/SUPPLY: Review 3Y Note Auction: Another Small Tail

Aug-05 17:03

- Treasury futures remain weaker, little react after $58B 3Y note auction (91282CNU1) tails yet again: drawing 3.669% high yield vs. 3.662% WI; 2.53x bid-to-cover vs. 2.51x prior.

- Peripheral stats see indirect take-up slips to 53.99% vs. 54.11% prior; direct bidder take-up 28.13% from 29.38% prior; primary dealer take-up rises to 17.88% vs. 16.51% prior.

- The next 3Y auction is tentatively scheduled for September 9.