US DATA: Far Smaller Trade Deficit As Tariff Front-Running Corrects Abruptly

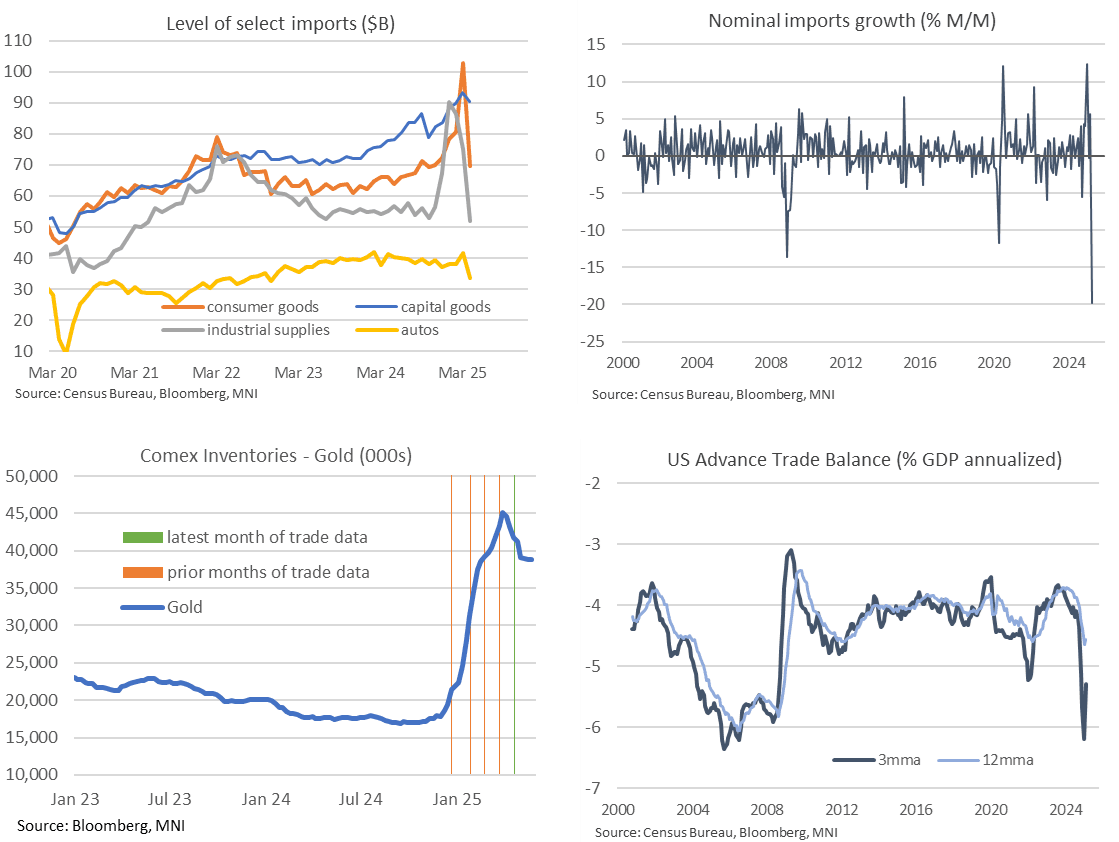

Advance April trade data saw a far smaller than expected goods trade deficit with clear signs of an abrupt cooling in imports after some particularly elevated readings ahead of reciprocal tariffs starting in April. We suspect gold and pharmaceutical products were particularly to blame but will have a better idea next week. Of note though, capital goods imports are one area that hasn't seen a meaningful correction lower.

- The goods trade deficit was far smaller than expected in the advance April release, printing just $87.6bn (cons $143bn, range $110-177bn across 34 estimates) after $162.3bn in March.

- The imports side of the ledger continues to dominate amidst major tariff distortions. Total imports fell -19.8% M/M for the biggest drop on record after a run with 5.7% M/M in Mar, -0.3% M/M in Feb and an almost record high 12.4% M/M in Jan.

- There were pull backs in imports across all the main categories but by far the most impactful were industrial supplies (probably gold) and consumer goods (probably pharma) along with a non-trivial hit to auto imports.

- It’s easiest comparing the outright levels after some unprecedented swings, where industrial supplies and auto imports have pulled back below 2024 averages. However, consumer goods and especially capital goods are still higher, with the latter interesting amidst investment pledges:

- Industrial supplies: $51.8bn in Apr, $75bn Mar, $86bn Feb, $90bn Jan and $67bn in Dec. They averaged $56bn in 2024.

- Consumer goods: $69.6bn in Apr, $103bn Mar, $81bn Feb, $78bn Jan and $72bn in Dec. They averaged $67bn in 2024.

- Autos: $33.6bn in Apr, $41.5bn Mar, $38bn Feb, $38bn Jan and $37bn in Dec. They averaged $40bn in 2024.

- Capital goods: $90.5bn in Apr, $93bn Mar, $90bn Feb, $88bn Jan and $84bn in Dec. They averaged $80bn in 2024.

- Final details, released Jun 5, will be needed but a small reduction in Comex gold inventories had suggested a further correction to more normal levels after gold imports surged in January and then moderated but were still extremely elevated in Feb and Mar.

- Consumer goods had recently seen a more abrupt contribution from a spike in pharmaceutical imports as they jumped from an already elevated $29.5bn in Fed to $50.4bn in Mar (they averaged $21bn in 2024). This was driven by Irish shipments in particular and we suspect this category saw a sharp unwind in April.

- There is still a huge amount of dust to settle but for what it’s worth, the goods trade deficit stands at 5.3% GDP on a three-month basis (from 5.1% in Jan and 4.1% in Oct) whilst the twelve-month rate stands at 4.6% GDP.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US DATA: Recapping Latest PCE Inflation Trends

Core PCE:

- 2.65% Y/Y drops from 2.96% in Feb for lowest since Jun 2024. However:

- 3.5% annualized over three months vs 2.4% in Dec

- 3.0% annualized over six months

Supercore PCE:

- 3.25% Y/Y from 3.65% in Feb for lowest since Jan. Recent trends also running hotter:

- 3.9% annualized over three months vs 3.7% in Dec

- 3.8% annualized over six months

PIPELINE: Corporate Bond Update: $1.25B NIB & $1B CoE Priced

- Date $MM Issuer (Priced *, Launch #)

- 04/30 $1.25B *Nordic Investment Bank 5Y SOFR+43

- 04/30 $1B *CoE Dev Bank 3Y SOFR+36

- 04/30 $Benchmark IADB 5Y SOFR+44

- 04/30 $Benchmark BNP Paribas 4NC3 fix/SOFR, 6NC5

- 04/30 $Benchmark Bahrain 12Y 7.5%, 8Y Sukuk 6.25%

EUROPEAN INFLATION: Slight Upside Risks For April EZ Core HICP - Analysts

Sellside analysts tend to see slight upside risks vs their initial estimates on EZ April Flash HICP (consensus stood at 2.1% headline and 2.5% core ahead of the national-level data released since yesterday, our full preview here) - overall, analysts are looking for for core somewhere between 2.5% to 2.6% now:

- Barclays: "We track EA headline and core HICP at 2.0% y/y and 2.5% y/y, respectively. This is in line with our forecast for headline inflation but 0.1pp higher than our forecast for core due to relatively firm data from Italy and Spain."

- Berenberg: "Eurozone inflation may not (yet) fall all the way to the 1.9% yoy rate we are forecasting for April. The expensive Easter holiday season seems to have contributed to stubborn services inflation in April. As this effect unwinds in May, inflation will likely decline further next month."

- Commerzbank: "We maintain our eurozone forecast that inflation in April is likely to have slightly fallen from 2.2% to 2.1%. However, we see upside risks to our forecast that the core rate has likely remained at 2.4%."

- Goldman Sachs: "We upgrade our Euro area headline inflation forecast for April to 2.12%yoy, from 2.11%yoy previously [2.09% initial]. We also revise up our Euro area core inflation forecast by 8bp to 2.63%yoy [2.54% initial], mostly driven by stronger-than-expected French and Italian core pressures. This would imply seasonally adjusted sequential core inflation of 0.25%mom in April on our estimates."

- JP Morgan: "Euro area headline inflation likely declined a tenth to 2.1%oya, with risks tilted towards a 2.0%oya reading. Core data, meanwhile, suggest that the Euro area core inflation likely increased more than we expected. We thus raise our Euro area core forecast from 2.5%oya to 2.6%."