FOREX: EURCAD Extends Pullback from 16 Year Highs, Scotia Remain Bullish

Sep-19 15:21

- The weaker-than-expected ex-autos read within the July retail sales report for Canada has done little to affect the Canadian dollar on Friday, as investor’s short-term appetite wanes ahead of the week’s close. USDCAD holds close to unchanged today, and remains lower on the week despite the dollar’s latest recovery.

- A cluster of daily lows at 1.3725 represents the key short-term support for USDCAD, a level that was matched again following the Fed decision this week. The latest bounce to 1.38 places the pair in the middle of a well established range across August and September, with 1.3925 the key level on the topside, the Aug 22 high and bull trigger.

- It’s EURCAD that has been more in focus in recent weeks, rising to the highest level since 2009 amid broader Euro optimism, before pulling back over the past three sessions.

- Scotiabank have noted the cross is already trading well above the year-end targets of their official forecast (1.55 for Q4 2025 and 1.56 for Q4 2026). Scotia remain bullish but also aware of the possibility of a pullback from historically elevated levels. Scotia now look to the 1.65/1.70 range as their next upside target. They highlight the importance of the 200d MA support as the cross is also currently stretched relative to its historical range.

- As a reminder, retail sales growth was weak in July as expected, particularly in core terms. The slow but relatively steady rate of consumption in Q3 probably won't be a major mover for the Bank of Canada after this week's 25bp rate cut.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $65.000 BLN TOTAL

Aug-20 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $455 MLN FROM $65.000 BLN TOTAL

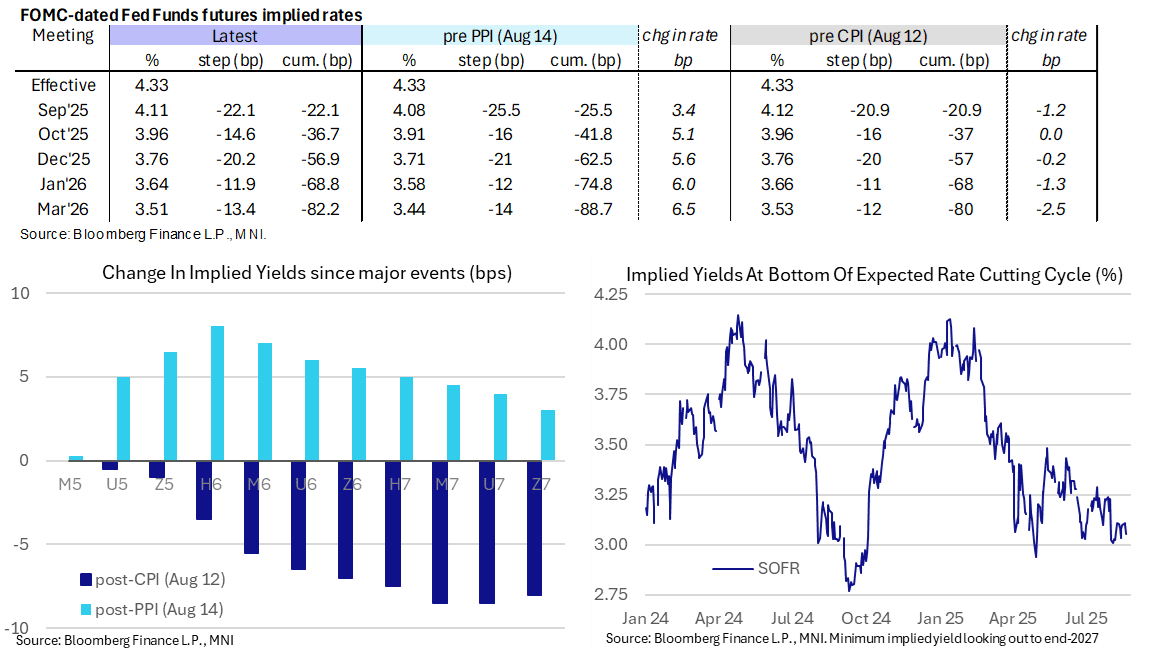

STIR: 2025 Rate Cut Prospects Build But Only Back To Pre-CPI Levels

Aug-20 15:13

- Rate cut prospects have increased on the two-prong nature of tech-led equity weakness and the WSJ reporting that Trump is considering firing Fed Governor Cook (a step up from his earlier Truth Social post urging her to resign).

- Fed Funds implied cumulative cuts from 4.33% effective: 22bp Sep, 36.5bp Oct, 57bp Dec, 69bp Jan and 82bp Dec.

- For context though, the 57bp of cuts to year-end is only back to levels seen shortly after Thursday’s strong PPI report and as such continues to have at least fully reversed the dovish impact from CPI earlier last week.

- Dovish implications are clearer to see further out the curve, with the SOFR implied terminal yield of 3.055% (SFRH7) now 4.5bp lower on the day (7.5bp lower than pre-CPI levels) after some narrow ranges in recent days.

- Terminal pricing does however keep to the 125bp +/-5bp of cuts from current levels range broadly seen since the Aug 1 payrolls report.

US TSY FUTURES: Extending Highs

Aug-20 15:10

- Mirroring late support in German Bund, Treasury futures continue to extend highs in late morning trade, weaker stocks (SPX eminis at 6377.5 -55.0) contributing to the move.

- Tsy Sep 10Y contract +7 at 111-31.5 session high, initial technical resistance at 112-15.5 (High Aug 5 and the bull trigger).

- Curves have reversed early flattening to steeper: 2s10s +.237 at 55.847, 5s30s +1.491 at 109.733.

- Focus on this afternoon's July FOMC minutes release at 1400ET.