EU CREDIT UPDATE: EUR Market Wrap

- 2y/10y bunds closed -2bp at 2.17%/2.78% - yields moved higher near the close along with USTs while bunds underperformed gilts following the hawkish BOE split. USTs closed -1bp at 3.97%/4.24%.

- Main/XO ended +3.7bp/+8bp at 58.7bp/308bp while €IG was -0.3bp at 0.9% (Corps -0.8bp at 0.84%, Fins +0.2bp at 0.98%, €HY -2bp at 3.01%). $IG was +0.4bp at 0.89% (Corps +0.7bp at 0.89%, Fins flat at 0.9%, $HY -0.3bp at 3.13%).

- SX5E/SPX futures closed -1.1%/-0.3% at 5447pts/5713pts. €IG movers included Amadeus IT Group (+2%), Enagas (+1%), Industria de Diseno Textil (+1%), Merlin Properties Socimi (+1%), Unicaja Banco (-5%), CaixaBank (-3%), Bankinter (-3%), ArcelorMittal (-3%).

- SX5E/SPX futures are -0.5%/-0.1% this morning. Oil is firmer, while gold is down after recent strong gains. China and Hong Kong equities continue track lower, moving off recent highs. Japan's National CPI print for Feb was a touch above expectations.

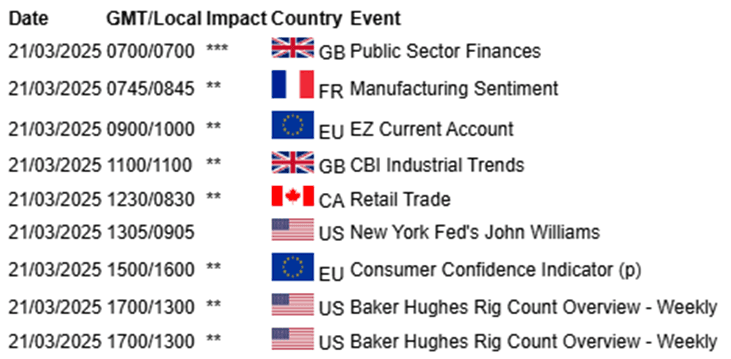

- Looking ahead, it is a quiet end to the week with French manufacturing sentiment out. Canadian retail sales also print. In the US we have Fed speak from Williams and Goolsbee (on CNBC).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DATA: Inflation Data Due at 7:00GMT

- The Bank of England forecast headline CPI at 2.82%Y/Y (with both the MNI median and Bloomberg consensus at 2.8%). Most analysts are within a 2.7-2.9%Y/Y range. This would be the highest print since March 2024.

- The closely watched services CPI is expected by the BOE to increase to 5.16%Y/Y (MNI Median and Bloomberg consensus are a little lower than this at 5.1%). This would be a notable increase from the low 4.37% print of December (but note that both the October and November prints were both above 5.0%).

- The reversal of the timing-induced very low December air fares print is the main expected contributor to the increase in both headline and services CPI, with VAT on private school fees and a 50% increase in bus fares (from £2 to £3) also contributing to both headline and services CPI.

- In addition with this being January data, new utilities prices will be included (these update quarterly and will contribute negatively) but fuel is the other component expected to add to headline CPI – so the overall impact of energy on headline CPI is likely to be muted.

- The other focus will be on the new weights – which remember come as A and B weights (with A weights in January and B weights for February through December) for the UK.

EUROZONE ISSUANCE: EGB Supply

Slovakia has announced a mandate for a syndication while Germany, Spain and France are all still due to hold auctions this week and Italy is due to launch its inaugural retail BTP Piu. Already this week, the ESM held a syndication whilst Slovakia and Finland held auctions. We look for estimated gross issuance for the week of E37.4bln (excluding the retail operation), down from E50.9bln last week.

For the full document including more details on issuance this week and next week click here.

- Slovakia is likely to hold a syndication today after it announced a mandate for a new 15-year SlovGB maturing 27 February 2040 to take place in the “near future”. We pencil in a transaction size of E2.5-3.5bln.

- The maturity is a little shorter than we had expected, we had looked for a new 12-year 2037 SlovGB to launch via syndication in February.

- This morning, Germany will return to the market to sell E4.5bln of the 10-year 2.50% Feb-35 Bund (ISIN: DE000BU2Z049).

- Tomorrow, Spain will hold a Bono/Obli auction. On offer will be a combined E4.5-5.5bln of the on-the-run 2.40% May-28 Bono (ISIN: ES0000012O59) and the 2.70% Jan-30 Bono (ISIN: ES0000012O00) alongside the 3.55% Oct-33 Obli (ISIN: ES0000012L78).

- Also tomorrow, France will hold a MT OAT auction selling a combined E11.5-13.5bln. The new 3-year 2.40% Sep-28 OAT (ISIN: FR001400XLW2), the 0% Nov-29 OAT (ISIN: FR0013451507) and the on-the-run 5-year 2.75% Feb-30 OAT (ISIN: FR001400PM68) will be on offer.

- Later tomorrow, France will return to hold a IL OAT auction to issue a combined E1.50-2.25bln. The 0.10% Jul-31 OATei (ISIN: FR0014001N38). The 0.10% Jul-36 OATei (ISIN: FR0013327491), the 0.95% Jul-43 OATei (ISIN: FR001400QCA1) and the 0.10% Mar-32 OATi (ISIN: FR0014003N51) will be on offer.

EUROZONE T-BILL ISSUANCE: W/C February 17, 2025

Greece, Portugal and the EU are all due to sell bills this week, whilst Germany, the Netherlands, France and the ESM have already issued bills. We expect issuance to be E18.9bln in first round operations, down from E22.2bln last week.

- Today, Greece will issue E500mln of the new 26-week Aug 22, 2025 GTB.

- Also today, Portugal will look to sell E0.75-1.00bln of the 11-month Jan 16, 2026 BT.

- Finally today, the EU will sell up to E1.5bln of the 3-month May 9, 2025 EU-bill, up to E1.5bln of the 6-month Aug 8, 2025 EU-bill and up to E1.0bln of the 12-month Feb 6, 2026 EU-bill.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar here.