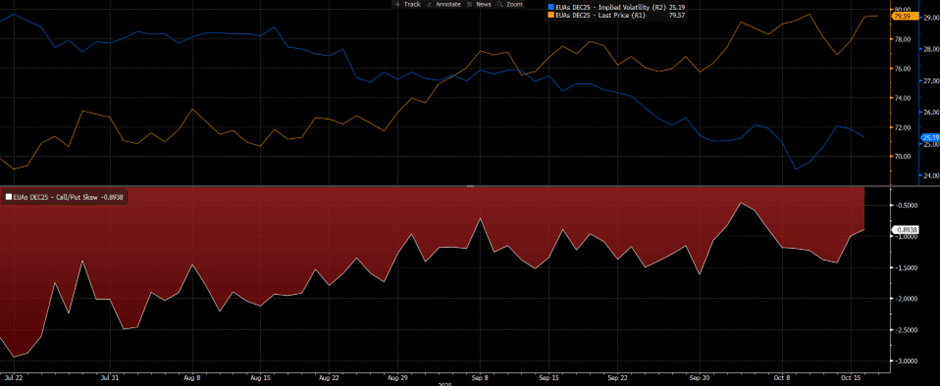

EMISSIONS: EUAs Implied Volatility Rebounds from All-Time Low

Oct-17 12:55

EUA Dec25 options implied volatility as of 16 Oct rebounded from the all-time low recorded earlier in the month, while put options open interest rose, signalling rising expectations for price swings and demand for downside protection.

- Implied volatility rose to 25.19% on 16 Oct from the record low of 24.18% on 9 Oct.

- The 25-delta call-put volatility skew stood at -0.89%, wider than the -0.46 in early October.

- The put/call open interest ratio increased to 0.76 on 16 Oct from 0.70 on 2 Oct, with put open interest climbing to 150,239 contracts from 139,459, while call open interest edging down to 197,106 from 199,207, reflecting higher growth in put positions.

- The largest open interest remains concentrated at the €70/t put strike with 21,049 contracts, and the €100/t call strike with 26,792 contracts.

- EUA Dec25 futures open interest rose slightly to 360k on 16 Oct from 359k on 2 Oct, while the price advanced 2.7% to €79.52/t on 17 Oct from €77.43/t on 2 Oct.

- EUA DEC 25 up 0.06% at 79.56 EUR/t CO2e

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

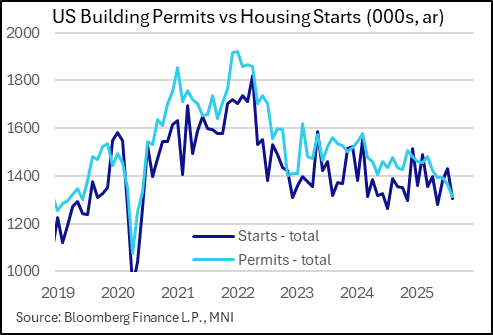

US DATA: Housing Activity Resumes Downtrend After Nascent Summer Pickup

Sep-17 12:54

Residential construction activity fared worse in August than expected, with building permits hitting fresh cycle lows after a brief uptick was seen in June and July.

- Permits came in at 1,312k (SA annualized), a drop of 50k from prior and well below the 1,370k consensus. This marks a new cycle low for this key leading indicator of construction activity, with the prior low set at the start of the pandemic in 2020 and before that, June 2019. Permits have only risen % M/M in 2 of the last 12 months, and are now down 11.1% Y/Y.

- Multi-unit permits fell 6.4% to 456k, the 2nd-lowest since 2020, with single-family permits down 2.2% to 856k, a 29-month low. Most of the weakness in volume terms is concentrated in the US South region, which experienced a boom in the early stages of the pandemic as Americans relocated. It's still the biggest region for permits by far (691k vs 621k for the Northeast, Midwest, and West combined in August), but has now fallen sharply in 4 of the last 5 months including 10% in the last 2 months alone.

- It was a similar story for housing starts, which basically lag permits. They fell 122k in August to 1,307k SA ann., vs 1,365k expected, with weakness in both single-family and multi-unit starts. That's not quite a fresh cycle low, with May having seen 1,282k, but likewise it appears that the Jun/Jul jump may have been fleeting.

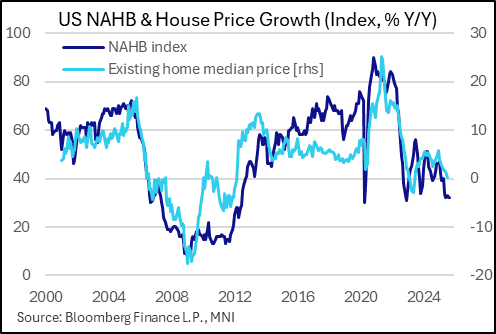

- Little improvement is expected. The NAHB Housing Market Index for September released Tuesday showed continued weakness in single-family homebuilder sentiment, with a headline score of 32 (33 expected, 32 prior), near the historic lows it's been for the last 4 months (ticked up to 33 in July), amid weak prospective buyer traffic and present sales offset by a small tick-up in expected future sales (still at depressed levels). And per the NAHB, "39% of builders reported cutting prices in September, up from 37% in August and the highest percentage in the post-Covid period".

- Estimates for residential investment have fallen since the start of the quarter, with the Atlanta Fed's GDPNow initially showing an expected 1.8% Q/Q SAAR growth in the category in Q3 after -4.7% in Q2 and -1.3% in Q1; however that's fallen to -4.6% in the latest update (albeit off the low of -8.2% seen after housing starts and home sales figures for July). We would expect the estimate to be pulled back again after this data.

- Apart from the GDP growth impact, it's likely house prices will continue to soften amid extraordinarily low affordability metrics and a softening labor market.

US TSYS: J.P.Morgan Cautious On Higher Yields If Fed Delivers 25bp Cut

Sep-17 12:53

Benchmark yields out to 10s are trading 2-5bp off multi-month lows, registered earlier in September, while 20s and 30s have hit fresh multi-month lows in the current session.

- J.P.Morgan believe that “duration positioning is relatively flat - our Treasury Client Survey as well as our core bond fund and CTA betas to Treasury yields are all very close to average levels observed over the last year, while our macro hedge fund beta indicates the levered community is positioned for higher yields”.

- They suggest “curve steepeners were crowded, and we think that those positions have been pared back significantly over the last two weeks now that money markets are pricing the Fed in neutral territory by late-2026”.

- Meanwhile, J.P.Morgan are of the view that “valuations are somewhat rich as 10-Year yields are trading about 16bp too low after controlling for their fundamental drivers, the richest they’ve been trading on this basis since the “Liberation Day” tariff announcement in early-April”.

- Taken together, they think that “risks are skewed somewhat to higher yields should the Fed deliver 25bp as expected, and we maintain tactical shorts in 10-year Treasuries as well as 5s/20s steepeners” ahead of the meeting.

EQUITIES: US and EU Roll pace (updated)

Sep-17 12:44

Equity Roll Update, expect for the December to be front Month in Europe Tomorrow, US has already moved to Dec earlier this Week:

- ESA: 75%.

- NQA: 60% (below pace).

- DOW: 74%.

- VGA: 75%.

- EU Banks: 76%.

- Stoxx600: 83%.

- Dax: 71%.

- FTSE: 73%.