EMISSIONS: EU Mid-Day Carbon Summary: EUAs/UKAs Fall On TTF Losses

Aug-15 11:19

EUAs/UKA Dec25 are on track for 3.41% and 2.66% weekly losses respectively, weighed by 3% losses in TTF amid higher LNG imports, while focus remains on the outcome of today’s Trump/Putin meet. Meanwhile, the gains in EU equities on optimism over Federal Reserve rate cut in September are limiting carbon downsides. EUA/UKA Dec25 are edging down to the lowest levels since late July and a one-week low respectively. EUAs have fallen below both the 10- and 50-day averages since Tuesday, while UKAs slipped below the 10-day average, signalling short-term downward pressure.

- EUA DEC 25 down 0.18% at 70.83 EUR/t CO2e

- UKA DEC 25 down 0.76% at 50.76 GBP/t CO2e

- TTF Gas SEP 25 down 1% at 31.815 EUR/MWh

- NBP Gas SEP 25 down 0.8% at 78.21 GBp/therm

- Estoxx 50 up 0.3% at 5451.32

- FTSE 100 SEP 25 up 0.2% at 9216.5

- The latest Germany ETS CAP3 auction cleared at €70.13/ton CO2e, down 2.79% compared with the previous Germany auction at €72.14/ton CO2e according to EEX.

- European gas prices have dropped to around the May lows on higher LNG imports and cooler weather. Focus also remains on the outcome of today’s Trump/Putin meet.

- Companies representing over 40% of global market capitalisation now have emissions reduction targets validated by the SBTi (Science Based Targets initiative), typically set for 2030. The number with verified near-term targets rose 97% in Q2 2025 compared with Q4 2023, according to the SBTi tracker.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ECB: Portugal Set To Replace Centeno - Bloomberg Sources

Jul-16 11:18

*PORTUGAL IS SET TO REPLACE CENTENO AS CENTRAL BANK GOVERNOR" Bloomberg

From the story:

- "Portuguese Prime Minister Luis Montenegro plans to replace central bank Governor Mario Centeno after his first term ends July 19, according to a person familiar with the premier’s thinking".

- "The government could announce his successor in the coming days, said the person, who asked not to be named because the information is confidential. Deliberations are ongoing and Montenegro may still change his mind or delay the decision, the person said. "

OUTLOOK: Price Signal Summary - Bear Cycle In Bunds Intact

Jul-16 11:17

- In the FI space, Bund futures have recovered from their latest lows, however, a bear cycle remains intact. Recent weakness resulted in a break of 129.30, the May 22 low. The breach strengthens the current bearish theme and exposes the next key support at 128.97, the May 14 low and a bear trigger. On the upside, resistance around the the 50-day EMA, at 130.28, marks the key short-term hurdle. A clear breach of it is required to highlight a possible reversal.

- A bear cycle in Gilt futures remains in play and Tuesday’s volatile bearish session reinforces this theme. The contract has recently breached support at 91.63, the Jul 2 low. Price has also traded through 91.50, the 61.8% retracement of the May 22 - Jul 1 bull leg. The move down exposes 90.97, the 76.4% retracement point. Clearance of this level would strengthen a bearish theme. Initial firm resistance is at 92.29, the 20-day EMA.

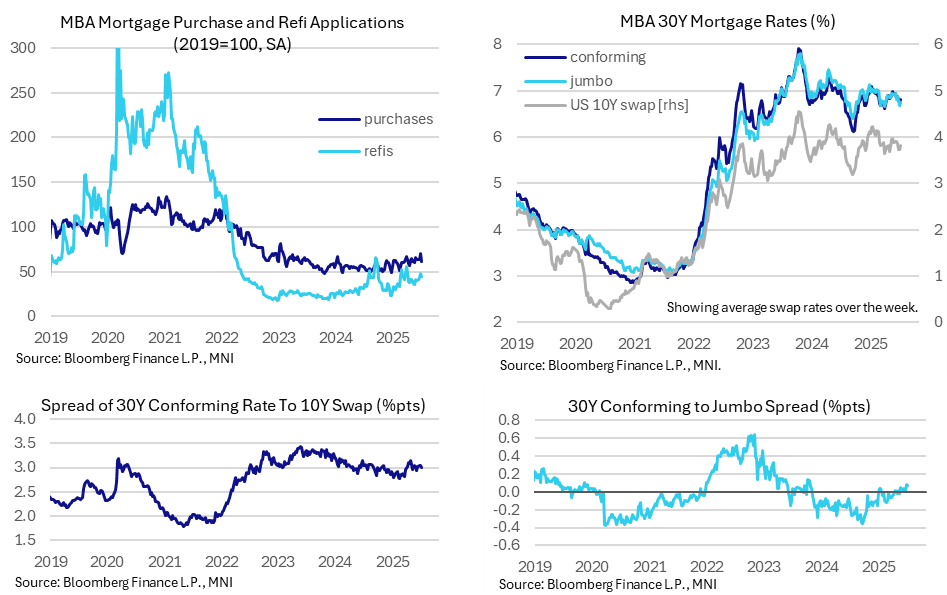

US DATA: Mortgage Activity Retreats On Mild Uptick In Rates

Jul-16 11:16

- MBA composite mortgage applications fell -10% last week (sa) to reverse the 9.4% increase the week prior.

- New purchase applications returned to being the larger drag when it comes to recent week on week changes, slipping -11.8% vs -7.4% for refis.

- Applications remain depressed but at familiar levels, with composite applications at 54% of 2019 averages, comprising of new purchases at 62% and refis at 44%.

- The drop in mortgage activity came on a relatively small increase in the 30Y conforming rate, +5bp to 6.82%, after the 6.77% the week prior had been the lowest since early April.

- With the average 10Y swap rate over last week rising 9bp, there was a mild narrowing in the mortgage to US swap rate spread, although it’s roughly holding around the 300bp mark since mid-May. For context, it widened to 315bp in late April/early May in fallout from US reciprocal tariff concerns although remains wider than the 280-290bps seen prior to April.

- Going against this marginal tightening point, at least compared to pre-reciprocal tariff levels, is the continued trading of 30Y jumbos inside regular rates, by 7bps after a shift to 8bp the prior week for its most since Oct 2023.

- Rates could further weigh on mortgage activity in next week's release, with the 10Y swap currently 8bp higher than last week's average.