EU CREDIT MACRO: EU Market Close

• 2y/10y bunds are closing +2bp at 2.04%/2.77%. Gilts +7bps and UST +4bps in 10yr.

• €IG closes +0.7bp on average. Evonik Perps down 80c following a profit-warning.

• Supply - EUR Corps: ALLRNV (PERPNC10 Sub), ARNDTN (5.25yr SUN), HEIANA (3yr SUN, Long 8 SUN, 12yr SUN), PNLNA (5yr SUN), SGSPAA (7yr SUN), VW (3yr SP FRN, 4yr SP, 7yr SP). EUR Fins: ASSGEN (PERPNC6 JR Sub), OMASST (4NC3 SP FRN). Books remain large at 4.9x at Guidance. Alliander and Generali in particular.

• SX5E/SPX futures are -0.5%/-0.4% at 5454pts/6666pts. €IG movers included H & M Hennes & Mauritz AB (+10%), Albemarle (+6%), IBM (+5%), Aumovio SE (+6%), EQT AB (-4%).

• Main/XO finish +0.7bp/+3bp at 56.7bp/268bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

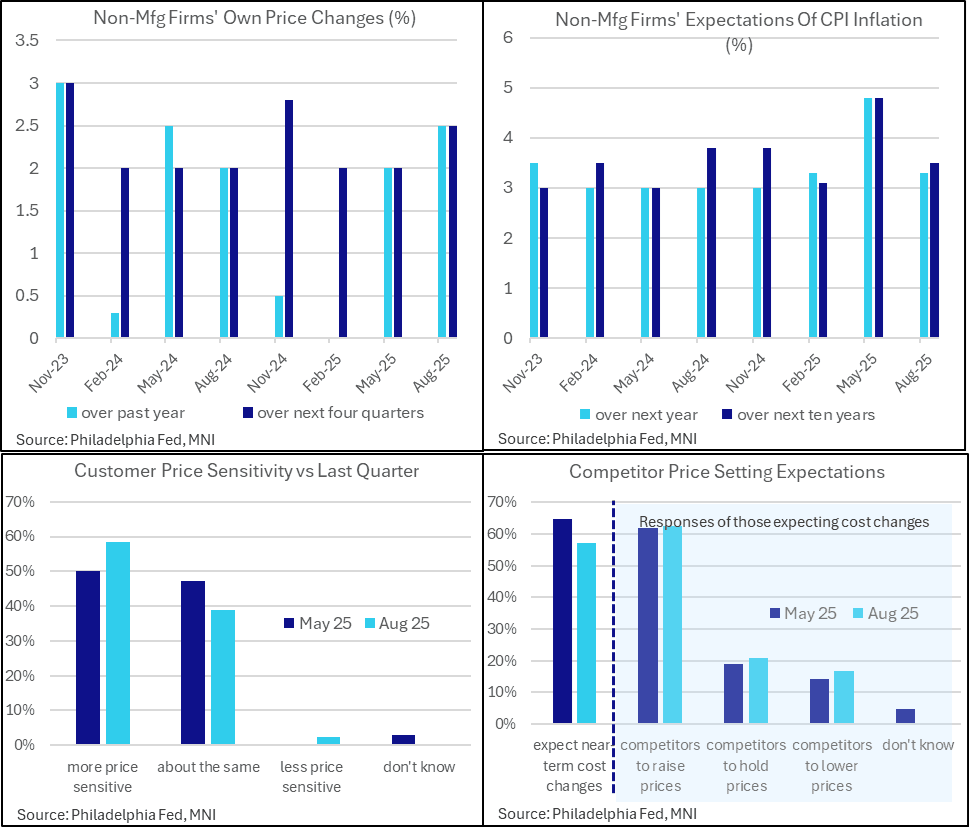

US DATA: Philly Non-Mfg Firms See Faster Price Increases Despite Sensitivity

- The Philly Fed non-manufacturing survey special questions on inflation expectations show a somewhat similar split in the activity indexes touched upon earlier with their historically large discrepancy between strong firms’ own activity and weak regional activity in August.

- The median firm reported increasing its own prices by 2.5% over the past year, up from 2.0% in the May question and having essentially paused annual price increases through end 2024/early 2025. It’s the strongest actual increase since the May 2024 survey.

- Own price expectations also firmed from 2.0% to 2.5%, above a typical median of 2% in surveys over the past almost two years but not an unprecedented level.

- Firms’ expectations of consumer inflation meanwhile cooled from a particularly strong May release, with those for the next year reverting to 3.3% from 4.8%. Ten-year ahead expectations also cooled to 3.5% after 4.8%, still above the 3.1% in February prior to reciprocal tariff announcements but within ranges.

- Elsewhere, these non-manufacturing firms reported greater price sensitivity over the quarter (59% reported higher sensitivity vs 50% in May) and fewer expect cost changes over the near-term (57% vs 65%). Of those that do expect cost increases, a similar almost two thirds expect those to be higher, with price changes over a median 3 months vs 2.5 months in the May survey.

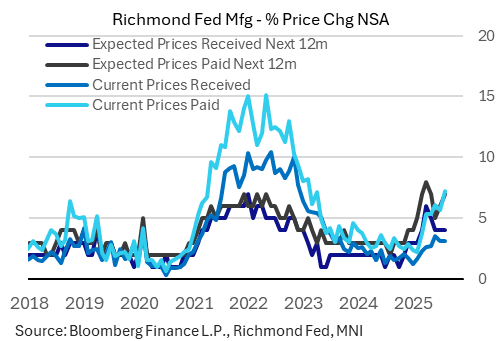

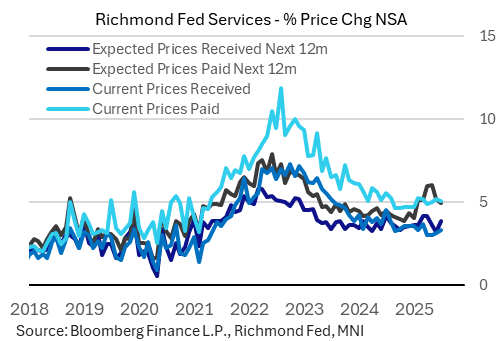

US DATA: Manufacturing Price Pressures More Acute Than For Services (2/2)

Looking across both the Richmond Fed's services and manufacturing surveys, there was a divergence in indicated price pressures, suggestive of tariffs feeding through to manufacturers more immediately.

- The Richmond Fed's manufacturing prices paid rose to a 28-month high 7.2% (reflecting changes over the prior 12 months), up from 5.7% prior; prices received were relatively steady at 3.1% (3.2% prior anda 2nd consecutive decline). 12-month expected prices paid rose for a 3rd consecutive month to 7.0% (6.0% prior, still below April's 8.0% high), with expected prices received at 4.0% for a 3rd month.

- For services firms, current prices paid ticked down 0.1pp to 5.1% (from 5.2%), with current received up to a 4-month high 3.3% (3.2% prior).

- Expected prices paid pulled back to a 6-monthlow 4.9% (5.2% prior), with expected received up to a 3-month high 3.9% (3.2% prior).

US STOCKS: Steady to Mixed on Narrow Ranges, Industrials, IT Outperforming

- Stocks are holding steady (SPX eminis) to mixed early Tuesday, off lows while holding to narrow ranges after Monday's modest decline. Currently, the DJIA trades down 15.51 points (-0.03%) at 45273.75, S&P E-Minis up 1 points (0.02%) at 6457.25, Nasdaq up 32.8 points (0.2%) at 21486.44.

- Industrials and Information Technology sector shares led gainers in the first half: GE Vernova +3.02%, Boeing +2.04%, General Electric +1.81% and Howmet Aerospace +1.78%.

- Leading tech stocks in the first half included: Palantir Technologies +2.30%, Advanced Micro Devices +2.26%, Monolithic Power Systems +2.21% and QUALCOMM +1.92%.

- On the flipside, Consumer Staples and Communication Services sector shares underperformed in the first half: Keurig Dr Pepper -2.99%, Brown-Forman -2.80%, Bunge Global -2.50% and Archer-Daniels-Midland -1.90%.

- Energy stocks weighed by a drop in crude prices (WTI -0.77 at 64.03): Devon Energy -1.29%, Diamondback Energy -1.23%, EQT -1.02% and Coterra Energy -0.98%.