EMISSIONS: EU End-Of-Day Carbon Summary: EUAs/UKAs Track Weekly Losses

Oct-24 15:31

{EEUAs/UKAs Dec25 are edging down and tracking weekly declines amid lower trading interest and losses in TTF on the day. Meanwhile, the slower-than-expected rise in US inflation in September limited losses in EU equities, which could influence carbon, as investors maintain a positive outlook for a Federal rate cut next week.

- EUA DEC 25 down 0.04% at 78.41 EUR/t CO2e

- UKA DEC 25 down 0.89% at 54.67 GBP/t CO2e

- TTF Gas NOV 25 down 1.6% at 31.925 EUR/MWh

- NBP Gas NOV 25 down 1.7% at 80.32 GBp/therm

- Estoxx 50 up 0.1% at 5672.48

- The latest Germany ETS CAP3 auction cleared at €78.47/ton CO2e, up 0.62% compared with the previous Germany auction at €77.99/ton CO2e according to EEX.

- ICE EUA futures are unchanged and continue to trade closer to their trend highs. A bull cycle remains intact. Support to watch lies at the 50-day EMA, currently at €76.49. A clear break of this average would signal scope for a deeper corrective pullback. For bulls, sights are on €80.37, the Oct 10 high and a bull trigger. Clearance of this hurdle would confirm a resumption of the uptrend and open €82.12.

- TTF front month has pulled back from a high of nearly €32.9/MWh yesterday but still on track for a small net gain on the week after the EU adopted another package of sanctions on Russia including a ban on LNG imports from 2027.

- EU leaders agreed on Thursday for the bloc to move ahead with setting a 2040 climate target of cutting net emissions by 90% versus 1990 level, while requesting to add revision clause, according to the European Council.

- MEPs called on the EU maintain ambitious NDCs, phase out fossil fuel subsidies, and accelerate the energy transition, ahead of COP30 next month, according to Committee on the Environment Climate and Food Safety press release on 23 Oct.

- Germany’s Federal Environment Ministry and UBA welcomed EU CBAM simplifications but emphasised that free allocation of EUAs for should continue until the mechanism fully protects domestic industries, according to the joint letter.

- France and Spain have urged EU leaders to maintain the ban on new diesel and petrol cars by 2035, stressing that zero-emission vehicles are “indispensable” for achieving carbon neutrality by 2050, according to a letter seen by Euronews.

- UK residence-based greenhouse gas emissions were estimated at 476mn tCO2e in 2024, down 0.5% from 2023 and 43.3% below 1990 levels, according to the Office for National Statistics.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOE: Greene due to speak on monetary policy at 17:30BST / 12:30ET

Sep-24 15:25

- Greene is due to speak on Wednesday in a speech entitled ‘Supply shocks and monetary policy’ (17:30) at the University of Glasgow Business School. We don't expect this to be market moving unless Greene says that she no longer believes that rates are restrictive. The text will be released here.

- This would be in contrast to her comments in her appearance ahead of the Treasury Select Committee on 3 September, when she said that "I think there are indications that we're still restrictive, but I'm not convinced that we're meaningfully restrictive. We've been in a rate cutting cycle for, you know, a year now, so it can't go on forever with us also being restrictive."

- Greene was also concerned about inflation persistence while being less concerned about downside risks to the labour market. We would be surprised if she changes this tone today. And we would be very surprised if she supported a November cut following her hawkish dissent in August.

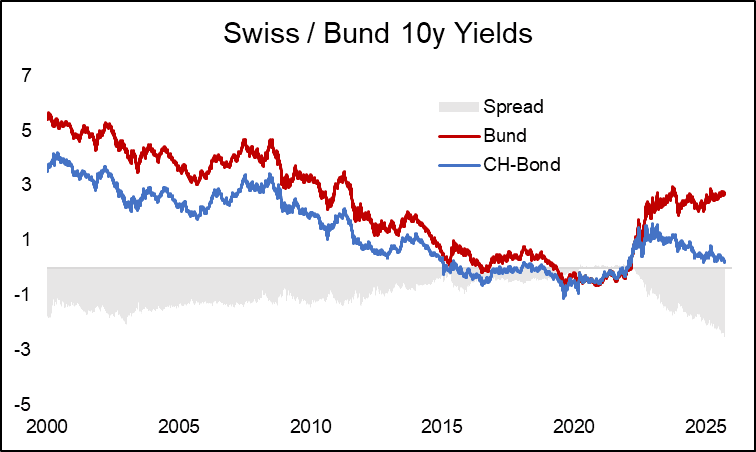

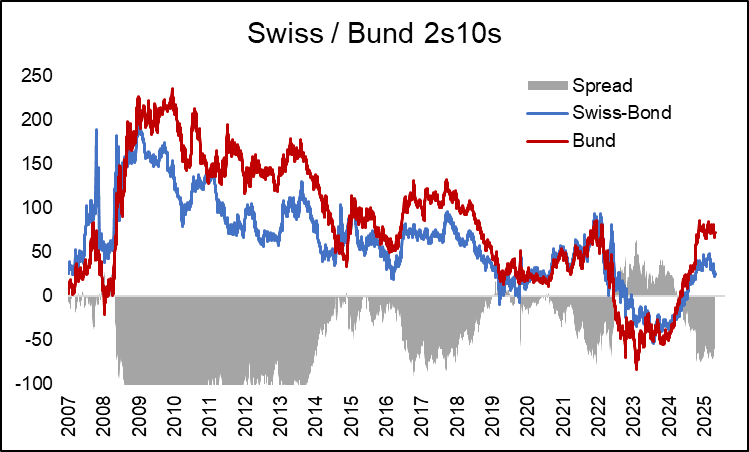

BONDS: Swiss-German Spread Extends Record Highs Ahead Of SNB; More Room In 2s10s

Sep-24 15:18

At 254bps, the Swiss - German 10-year government bond yield spread stands at its widest levels on record, extending its longer-term trend which started 2022.

- Form a broader perspective, the moves lower in Swiss 10-year yields over the past two years continue to be striking when viewed against global core FI markets, and highlight the unique position the Swiss economy finds itself - characterized by low inflation and the prudent federal fiscal position. German yields increased last year as expansionary fiscal policy reduced scarcity through expected higher issuance. But this has not been the case in Switzerland where scarcity still remains.

- The moves recently in Germany have been seen across the curve - and have generally been driven by the short-end. In Switzerland, the 2-year has remained well anchored as it already anticipates policy rates remaining at or close to zero for an extended period, but there has been a flattening of the 2s10s Swiss curve, partly driven by US-driven factors (that seem to have spilled over more outside of the Eurozone) and partly driven by the expectation that policy rates in Switzerland may remain lower for longer - and notably longer than 2-years.

- Given both the ECB and SNB (preview of tomorrow's decision here) appear to stand near or at end of their rates cycles, further room for adjustment of the Swiss - German 10y spread may be centred around the respective countries' curve shapes. This leaves focus on a potential re-pickup of global core FI steepening, the German fiscal situation, as well as any news on the Swiss trade situation.

FED: US TSY 17W AUCTION: NON-COMP BIDS $470 MLN FROM $65.000 BLN TOTAL

Sep-24 15:15

- US TSY 17W AUCTION: NON-COMP BIDS $470 MLN FROM $65.000 BLN TOTAL