EQUITY OPTIONS: EU Bank Outright Put Buyer

Sep-25 13:44

SX7E (17th Oct) 220p, bought for 2.10 in 12k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

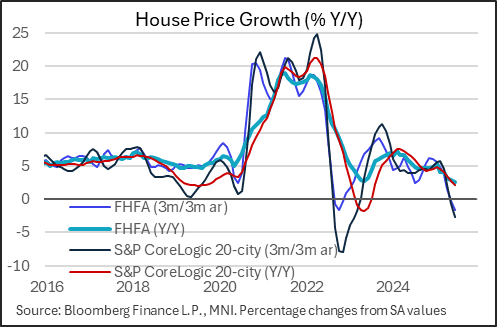

US DATA: House Price Momentum Continues To Wane

Aug-26 13:43

House prices were mixed versus expectations in June, but the overall trend is toward further softening.

- The FHFA's house price index fell 0.2% M/M (-0.1% expected, -0.1% prior), with the S&P CoreLogic 20-City index falling 0.25% M/M (-0.20% expected, -0.32% prior).

- Momentum In all of the major house price aggregates is turning decidedly lower, amid rising inventories/low sales and continued high mortgage rates negatively impacting affordability.

- The FHFA's index is now falling at a 1.7% 3M/3M annualized rate, the weakest since 2011, with the S&P's 20-City at -2.7%, weakest since early 2023. This should be taken into broader context: both indices are up around 50% vs the start of 2020 and remain positive on a Y/Y basis (2.6% and 2.1% respectively) but have slowed considerably on that basis in the last several months.

- With pending home sales remaining weak and homebuilder sentiment as negative as it's ever been, we continue to expect downside pressure on prices.

SONIA OPTIONS: Call Fly seller

Aug-26 13:29

SFIV5 96.10/96.20/96.30c fly, sold at 2.75 in 3k.

SONIA OPTIONS: Outright Call buyer

Aug-26 13:24

SFIU6 96.90c bought for 9 up to 9.25 in 4k (ref 96.39).