EM LATAM CREDIT: Ecuador: IMF USD600mn Disbursement – Positive

(ECUA; Caa3/B-/CCC+)

• The IMF staff released results of their third review of the 48 month USD5bn Extended Fund Facility (EFF) and authorized the disbursement of USD600mn for Ecuador, saying that program performance has been strong.

• Economy Minister Moya said USD600mn would be used to strengthen the country’s electrical system and to finance social services. The expression of confidence by the IMF in Ecuador’s reforms affirms our positive view. ECUA 35s were last quoted $75.60, up ½ point today, 2 ½ points since June 30th and up nearly 20 points YTD.

• Further affirming our view of commitment to reforms, Barrons reports that Ecuador just deployed 3,000 troops, to quell protests which have threatened to turn into an uprising. The govt. is committed to reallocating fuel subsidies with a more direct approach of compensating drivers and supporting social programs to discourage alleged fuel trafficking and supporting of criminal organizations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Corrective Cycle In Gilts Intact

- In the FI space, recent gains in Bund futures resulted in a break of resistance at 128.87, the Aug 28 high and short-term bull trigger. The climb undermines a recent bearish theme and highlights a stronger reversal. Price has moved through the 129.00 handle, signalling scope for an extension towards 129.50, the Aug 5 high. Key support and the bear trigger has been defined at 127.61, the Sep 3 low. First support is 128.58, the 20-day EMA.

- A rally in Gilt futures last week and a bullish start to this week’s session, highlights a stronger corrective cycle. The move higher is allowing an oversold trend condition to unwind. The contract has breached initial firm resistance at 90.84, the Aug 28 and 29 high. A continuation higher would open 92.06, the Aug 14 high. On the downside, initial support lies at 90.65, the Sep 5 low.

US TSYS: Early SOFR/Treasury Option Roundup: Rate Cut Pricing Cools Ahead PPI

Mixed SOFR & Treasury options reported overnight, the former leaning towards upside calls in the lead-up to this morning's PPI inflation data. Underlying futures weaker but off overnight lows in the last few minutes. Projected rate cuts retreating from late Tuesday (*) levels: Sep'25 at -27.2bp (-28.7bp), Oct'25 at -45.9bp (-49.6bp), Dec'25 at -67.5bp (-71.4bp), Jan'26 at -79.9bp (-85.1bp).

- SOFR Options:

- Block/screen over 35,000 SFRZ5 96.43 calls, 8.0 ref 96.33 to -33.5

- Block, 2,870 SFRM7 96.87 calls 54.5 vs. 97.095/0.58%

- Block, 5,000 SFRH6 96.50/96.87/97.00 broken put trees, 4.75/splits vs. 97.11

- -9,000 SFRH6 96.00/96.31/96.43 broken put trees, 3.0

- 9,000 SFRH6 96.00 puts, 1.75 last

- 3,500 SFRV5 96.37/96.62/97.00 broken call flys ref 96.335

- +3,274 SFRZ5 96.50/96.62/96.68/96.81 call condors, 1.0

- 5,000 SFRX5 96.43/96.68 call spds

- 5,000 SFRV5 96.31 puts ref 96.335

- 2,000 SFRZ5 96.50/96.62 call spds ref 96.33

- +5,000 SFRU5 95.93/96.00/96.06 call flys, 2.5

- over 7,000 SFRU5 96.00/96.12/96.25 call flys, 0.5-0.75 ref 95.9725

- Treasury Options:

- +2,000 FVZ5 110/111 call spds vs. 108.75 put, 2.0 net ref 109-25

- 2,000 USX5 133 calls vs. 3,000 USX5 104 puts ref 116-27

- -1,000 TYZ5 113 straddles, 209 ref 113-10

- +5,000 TUV5 104/104.75 call over risk reversals, 2

- -4,000 TYZ5 130.5 calls w/ -2,000 TYZ5 104.5 puts ref 113-10.5

- 1,140 TYV5 112/112.5 3x2 put spds ref 113-09.5

- 2,200 TYV5 112.25 puts ref 113-08.5

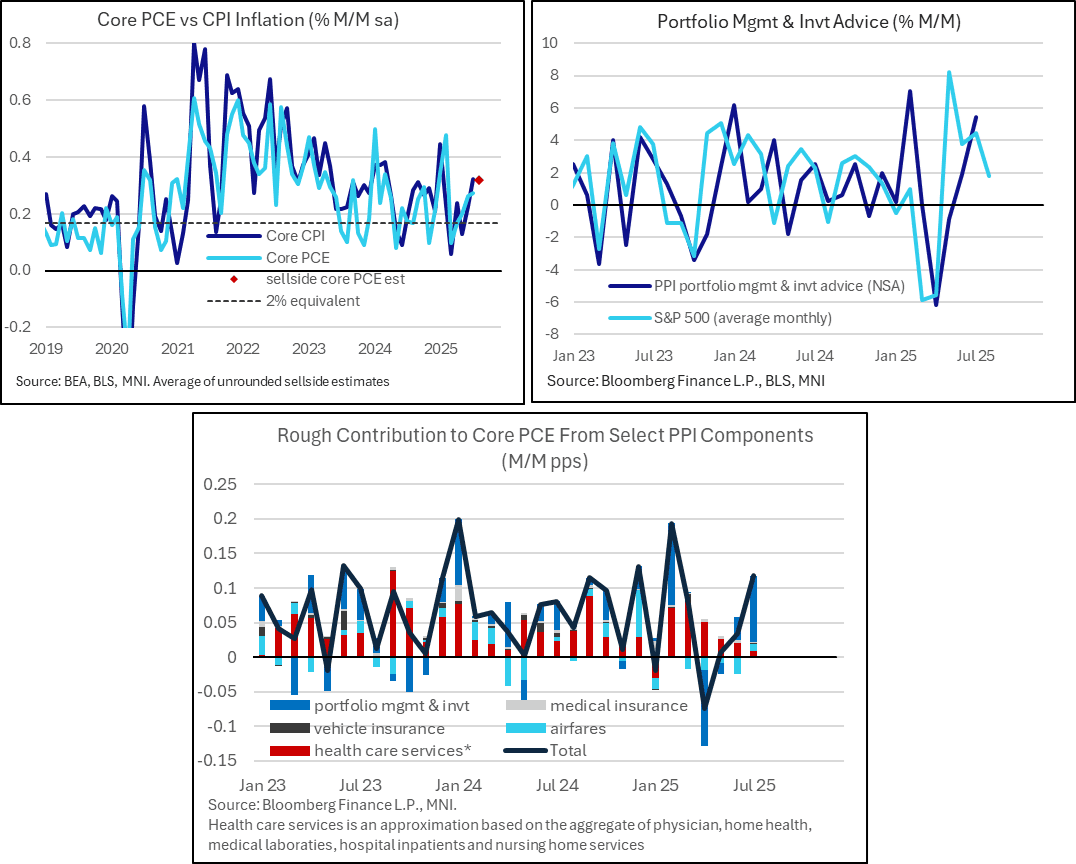

US OUTLOOK/OPINION: PCE Components To Watch Out For In PPI (3/3)

- As for some of the PPI-specific components that feed into PCE calculations, expect the usual focus on airfares, portfolio management, vehicle insurance and a raft of health services.

- The below categories are on a non-seasonally adjusted basis:

- Portfolio management and investment advice: it increased a strong 5.4% M/M in July as it reflected equity market strength with a slightly longer than usual. We wouldn’t be surprised to see another sizeable increase. Nomura look for a “decent” 2.2% increase.

- Domestic airfares: Seasonal norms suggest that this should decline further after the -2.15% M/M in July. Nomura: “Although PPI's domestic airline fares likely declined by 3.1% m-o-m, the expected decline was mostly due to a seasonal movement, which is likely to be largely offset by the BEA's seasonal adjustment when it is incorporated into core PCE inflation calculation”

- Health care services (for a crude proxy of categories that feed into PCE): Nomura estimate a “trend-like” pace of 0.1-0.2% M/M.

- As for where core PCE estimates currently stand, in the limited number of estimates we’ve seen, the readthrough for the month’s core PCE is seen as relatively minor in terms of directional divergence. Median core PCE estimates are for 0.31% M/M vs 0.27% prior and 0.32% for core CPI, with no analysts seeing core PCE printing above core CPI.

- As it stands, the M/M core PCE estimate would be the highest since February.