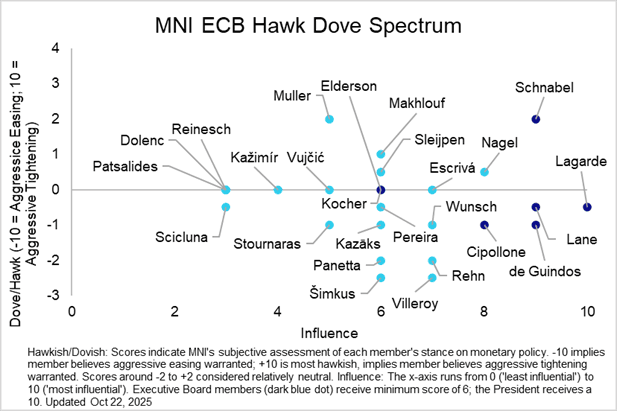

ECB: ECB Speak Wrap (Oct 6 - Oct 22)

The IMF/World Bank meetings in Washington DC brought a significant amount of commentary from ECB Governing Council members. Save for some nuances in views on both the dovish and hawkish end of the spectrum, the overwhelming message was that policy remains in a “good place”. The bar to another rate cut appears to be high, though policymakers haven’t fully closed the door to such a move, in line with the data-dependent and meeting-by-meeting approach.

An unchanged rate decision at next week’s October decision seems assured, with major guidance changes also unlikely. EUR STIR markets will probably pay more attention to next week’s swathe of regional data, including Q3 flash GDP and October flash inflation.

As usual, the full summary of ECBspeak by date, policymaker and topic are in this publication. In this iteration, we also launch our MNI’s ECB Hawk/Dove matrix.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SEK: Trading As A High Beta Euro Ahead Of Tomorrow's Riksbank Decision

- SEK outperforms the G10 basket this morning, seemingly trading as a high beta Euro with no obvious tailwinds from the equity/risk sentiment or rate differential channels. Focus of course remains on tomorrow’s Riksbank decision, which is a very close call between a hold and a 25bp cut. MNI preview here

- EURSEK overnight implied ATM vols are at the highest since June, pushing the breakeven on an ATM straddle expiring at tomorrow’s NY cut to 40 pips.

- The Government formally announced its 2026 budget today, which contains SEK80bln of unfunded policies to help stimulate household consumption and employment. While the confirmation of the expansionary budget may be lending light support to SEK today, we caution that most of the policies were already announced in the run-up to today’s announcement.

- The key focus ahead of tomorrow’s Riksbank decision will be on the fiscal multipliers embedded within the September MPR projections.

- JP Morgan believe the Riksbank decision “presents tactically dovish risks for SEK”, but “remain bullish and would fade a kneejerk sell-off as (1) beyond the near-term, SEK should benefit from FX market focus on fiscal differentiation, yield compression, and growth relief from cuts, and (2) while only 8bps are priced for next week, there is a cumulative full cut priced by 1Q’25 and if this is merely frontloading, it can blunt the reaction". As such, they continue to hold a short EUR/Scandi basket trade.

FED: St Louis's Musalem: Limited Room For Easing, Policy May Be Close To Neutral

St Louis Fed President Musalem (2025 FOMC voter, hawk) says he supported the 25bp cut in September as a "precautionary move" "because recent data indicate that the downside risks to employment have increased relative to the risk of inflation remaining persistently above target", however he calls for a cautious approach to easing because "I see a risk that above-target inflation could be more persistent than is desirable".

- Given this outlook we highly doubt he's at (let alone below) the median 2025 FOMC "dot" of 3.6%, and instead is probably one of the 7 members who favored no further cuts over the next two meetings (4.1% or above) though it's possible he was one of the 2 members who wrote down 1 more additional cut (3.9%).

- He says "I believe there is limited room for easing further without policy becoming overly accommodative, and we should tread cautiously for three reasons": 1) financial conditions already supportive of the economy, 2) looking through one-time tariff inflation impacts "is appropriate" but a posture of "looking through" "could risk price stability if taken too far, or if maintained for too long", 3) the ex-ante real policy rate is already close to neutral (4.1% Fed funds, 12-month forward inflation of 3.3% = 0.8%, below the 1% median long-run neutral rate FOMC median in real terms).

- On those real rate estimates, he cites potential conditions under which he would support further easing: "I do not view 1% as a floor below which the real policy rate must not go. But to go there, I believe the outlook or balance of risks must shift further from where they are today, especially if inflation looks likely to remain persistently above target. Should further signs of labor market weakness emerge, I would support additional reductions in the policy rate, provided the risk of above-target inflation persistence has not increased and longer-term inflation expectations remain anchored."

- He says that "The stance of monetary policy now lies between modestly restrictive and neutral, which I view as appropriate."

- He sums up, "While providing insurance against labor market weakness, I believe that monetary policy should continue to lean against persistence in above-target inflation, whether it materializes from the impact of tariffs, lower labor supply growth, or for other reasons."

- In Q&A, he says "I think there is limited room for further policy easing without getting into overly accommodative territory. So I think we should tread with in a cautious way, in a gradual way."

- "I am open to further adjustments in the in the policy rate. As I said, I think the the space for doing so before policy becomes accommodative, you know, is limited.... we're gonna get some more data between now and and the and the October meeting. I'm really focused on a path rather than, you know, the next meeting. I am taking a meeting by meeting approach, because I believe every piece of incremental information is important."

- Asked by MNI whether it's fair to say that he doesn't see the 25bp September cut as the start of an extensive easing cycle, Musalem says: "I can't pre-judge what the committee will do at each future meeting, so I won't be able to answer that question. But I did say, in terms of my own opinion or my own view, that I would be prepared to go below that 1% long term real neutral rate, provided I did see labor market weakness risks rising, and if inflation expectations remain anchored, and if there's no further persistence of the inflation path. So you know, I never think of the long run neutral rate as some sort of artificial boundary below which you can never go, but you have to go there under the right baseline outlook and shift in balance of risks."

US TSY FUTURES: Loosely Following Bunds Lower

- Treasury futures extending session lows, Dec'25 10Y currently +.5 at 112-24.5 - still off overnight lows that matched Friday morning lows (TYZ'5 112-22).

- Loosely following German 10Y Bund retreat in late Europe trade.

- Cross asset roundup: Bbg US$ index (BBDXY) inching off morning low of 1196.34 to 1198.01; US stocks mixed with Nasdaq climbing to new record high (22,692.98), SPX eminis near Friday's record high at 6729.00, while the DJIA trades weaker: -26.30 at 46,294.93 -20.60.

- Look ahead - no more data today, focus on a trio of Fed speakers at 1200ET: Cleveland Fed Hammack on banks & economy, Richmond Fed Barkin, Fed Gov Miran moderated Q&A from Economic Club/NY.