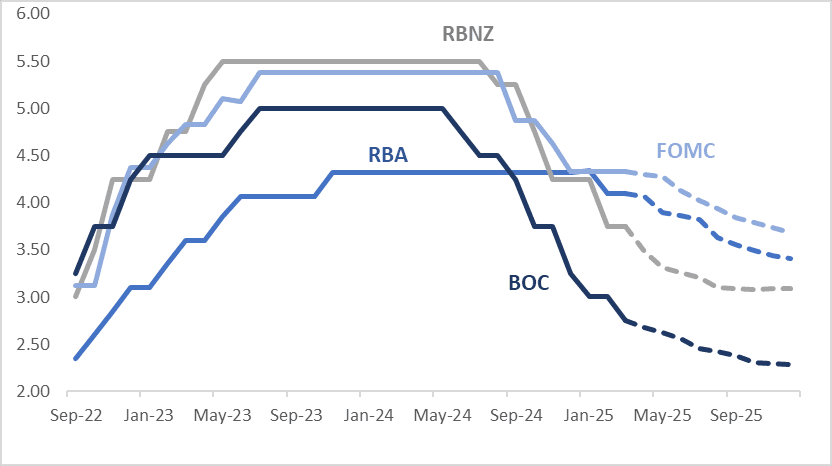

STIR: $-Bloc Markets Muted Over the Past Week Despite Key Data/Events

Mar-21 2025 02:28

In the $-bloc, rate expectations through December 2025 remained largely stable over the past week. U.S. pricing firmed by 6bps, while Canada, Australia, and New Zealand experienced minimal net movement.

- On Tuesday, Canada's headline inflation quickened in February as a sales tax holiday ended but so did core measures excluding that policy change, suggesting the central bank faces a bigger trade-off in any further interest-rate cuts to help the economy adjust to the US trade war.

- On Wednesday, the Federal Reserve held rates steady at 4.25-4.5%. The bulls were relieved by Fed Chair Powell's relatively dovish stance and the dots holding to two rate cuts this year, while bears noted the new 2025 SEP estimates reflecting slowing growth and rising inflation. Chairman Powell said the Fed is well-positioned to sit tight and wait for policy uncertainty to subside before making any decisions on interest rates.

- On Thursday, Australia’s February employment was weaker-than-expected falling 52.8k due to fewer older workers returning, while January was revised down to +30.5k. The number of unemployed also fell and so the unemployment rate was unchanged at 4.1%, while underemployment continued to fall.

- Looking ahead to December 2025, the projected official rates and cumulative easing across the $-bloc are as follows: US (FOMC): 3.68%, -65bps; Canada (BOC): 2.28%, -47bps; Australia (RBA): 3.42%, -68bps; and New Zealand (RBNZ): 3.09%, -66bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Bull-Steepener, BoJ Takata Reiterates More Tightening Coming

Feb-19 2025 02:12

At The Tokyo lunch break, JGB futures are stronger, +15 compared to settlement levels.

- BoJ board member Takata reiterated that the central bank is in a position to adjust policy rates further if the outlook is met. Takata stated that risks of big market moves have been lowered, giving the central bank more flexibility. This is a likely nod to last year's sharp risk off move in the wake of the end July hike by the central bank (although other factors were also in play).

- Japan's January trade figures were mixed. Exports rose 7.2% y/y, close to the 7.7% forecast and up from the prior 2.8% pace. Imports surged though to 16.7%y/y, from 1.7% in Dec and against a 9.3% forecast.

- Other Japan data released showed core machine orders for Dec weaker than forecast. We fell 1.2% m/m, against a 0.5% forecast and 3.4% prior. In y/y terms we printed 4.3% (against a 7.5% forecast and 10.3% prior).

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s heavy session.

- Cash JGBs have slightly bull-steepened, with yields flat to 1bp lower across benchmarks. The benchmark 10-year yield is 0.2bp lower at 1.428% after hitting a fresh cycle high of 1.446%.

- Swap rates are 1-5bps higher, with the 20-year underperforming. Swap spreads are wider.

CHINA: Could The Tide Be Turning for Bond Yields in China?

Feb-19 2025 02:09

- Since the lows in early January, bond yields in China have inched higher quietly. From a low of 1.01%, China’s 2YR Government bond yield has moved 39bps higher to 1.40% for yesterday’s close. For the 5-year, yesterday’s close of 1.53% represented a move of +21bps higher. The 10-year benchmark has risen from a low of 1.59% to yesterday’s close of 1.71%.

- When considering the moves in bond yields compared to the move to the CSI 300, it poses something interesting.

- Finishing 2024 at 3,934.91, the index closed yesterday at 3,912.78 – a decline of -0.56%. However, it is the move in recent trading sessions that calls for further investigation.

- Against a backdrop of a 2.7% gain in the CSI 300 during the trading sessions on Thursday and Friday last week, and Monday; the 10YR bond yield rose 7bps, and the 2YR is 13bps higher.

- This comes after a period where bond markets had been relatively calm, despite news that the PBOC had halted their bond purchases in mid-January.

- The move higher yields is also against a backdrop of comments from the PBOC Governor in Saudi Arabia on Sunday that more accommodative monetary policy can be expected.

- A further development in recent days has been the meeting between President Xi and Alibaba’s Jack Ma and other key entrepreneurs; in a sign that the relations between the President and the private sector could be improving.

- Whilst a short period move does not make a trend, the CSI 300’s rally and the inverse move from bonds is worth noting.

Figure1: CGB10YR and CGB 2YR yields (source: BBG)

CHINA: Home Prices Stagnate in JAN; as Lunar Holidays Impact.

Feb-19 2025 01:59

- New home prices in January fell by -0.07%, a modest improvement from the -0.08% in December.

- This represented the fifth consecutive month of improvement.

- Used home prices fell -0.34%, a modest increase from -0.31% in December.

- For used home prices, this halted a run of improving prices for four months.

- Prices for new homes fell in 42 cities, compared to 43 the month prior.

- Beijing new home prices -0.4% m/m; -5.7% y/y

- Shanghai new home prices +0.6% m/m; +5.6% y/y.

- Beijing used home prices +0.1% m/m; -3.8% y/y

- Shanghai used home prices +0.4% y/y; -2.3% y/y

- The January prices will provide little insight into the progress in the sector, as the month was impacted by the Lunar New Year holiday.