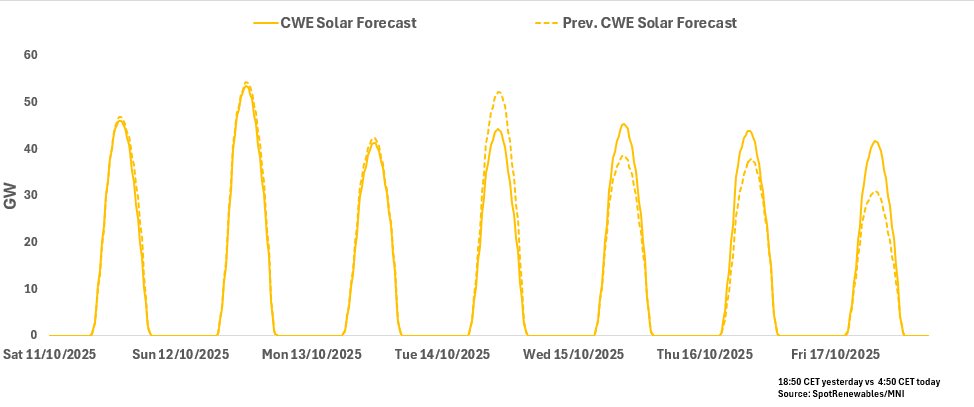

RENEWABLES: CWE Morning Solar Forecast

See the latest CWE solar forecast for peak-load hours starting this morning for the next seven days. CWE solar is anticipated to be low over 13-17 October at between 14-15% load factors.

CWE Solar for 11-17 October

- 11 October: 25.20GW

- 12 October: 29.29GW

- 13 October: 22.54GW

- 14 October: 23.84GW

- 15 October: 24.92GW

- 16 October: 24.09GW

17 October: 22.47GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

WTI TECHS: (V5) Trend Needle Points South

- RES 4: $77.85 - 2.794 proj of the Apr 9 - 23 - May 5 price swing

- RES 3: $75.65 - 2.500 proj of the Apr 9 - 23 - May 5 price swing

- RES 2: $74.25 - High Jun 23 and a bull trigger

- RES 1: $66.03/69.36 - High Sep2 / High Jul 30 and key resistance

- PRICE: $63.21 @ 07:19 BST Sep 10

- SUP 1: $61.29 - Low Aug 13 and the bear trigger

- SUP 2: $57.71 - Low May 30

- SUP 3: $54.80 - Low May 5

- SUP 4: $54.03 - Low Apr 9 and a key support

The trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

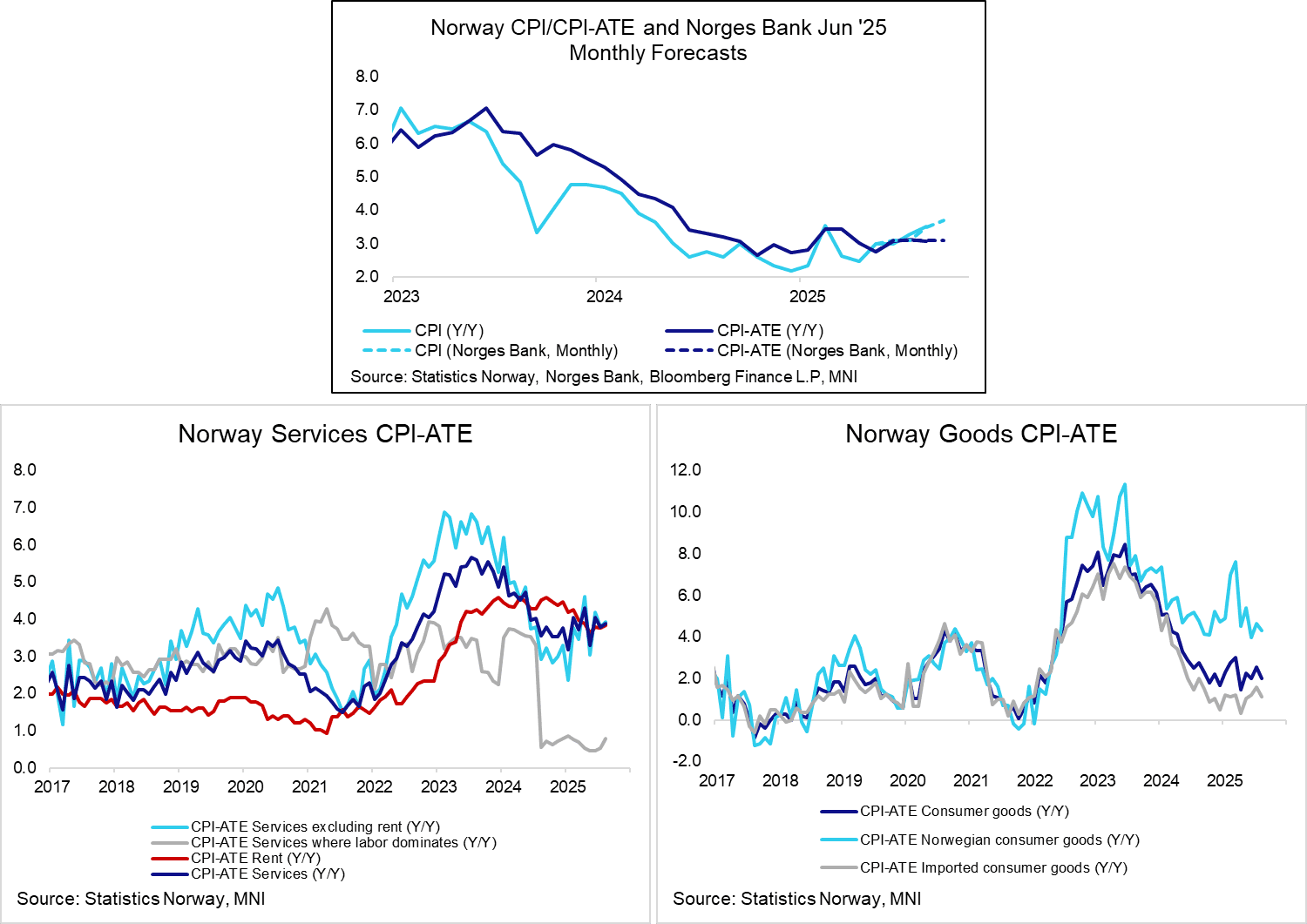

NORWAY: Stronger-than-expected Underlying Inflation, But Not Alarmingly So

CPI-ATE inflation was 3.07% Y/Y in August, after 3.12% in July and 3.07% in June. Overall, we judge it to be a little stronger than expected by analysts and Norges Bank, but not alarmingly so. A portion of CPI-ATE strength came from the volatile airfares category.

- Despite Norges Bank noting at the August decision that “Child daycare prices were reduced from 1 August 2025 and will thus be lower than assumed in the June Report”, Statistics Norway suggests the policy did not have much impact on annual CPI-ATE inflation in August. From the press release: “Despite a large reduction in the maximum price for kindergartens from July to August, this does not significantly reduce the twelve-month growth in the CPI. This is because the maximum price was reduced by about the same amount this year as last year”.

- Excluding these prices from CPI-ATE, Stats Norway notes that inflation would have been 3.9% Y/Y. This underscores why Norges Bank remains cautious in its approach to easing monetary policy – underlying inflation is still quite strong.

- Overall, services excluding rent accelerated to 3.93% Y/Y (vs 3.80% prior). An uptick in airfares (8.34% Y/Y vs -0.18% prior) was an important contributor here. Other services components generally eased a little.

- Rents, which some analysts had expected to decelerate in August, ticked up to 3.83% Y/Y (vs 3.77% prior).

- Elsewhere, food inflation fell to 4.70% Y/Y (vs 5.57% prior), a dynamic that was in line with analyst expectations. This was offset a little by accelerations in non-alcoholic and alcoholic beverage inflation.

- Domestic goods inflation eased to 4.33% Y/Y (vs 4.65% prior), while imported goods fell to 1.11% Y/Y (vs 1.58% prior).

- Headline CPI was 3.53% Y/Y, in line with expectations (vs 3.27% prior). As expected, electricity inflation accelerated in August on a base effect (29.41% Y/Y vs 12.98% prior).

GOLD TECHS: Bulls Remain In The Driver’s Seat

- RES 4: $3716.5 - 2.500 proj of the Dec 30 ’24 - Apr 3 - 7 price swing

- RES 3: $3700.0 - Round number resistance

- RES 2: $3674.8 - 2.382 proj of the Dec 30 ’24 - Apr 3 - 7 price swing

- RES 1: $3674.3 - High Sep 9

- PRICE: $3645.0 @ 07:26 BST Sep 10

- SUP 1: $3579.7 - Low Sep 9

- SUP 2: $3474.7 - 20-day EMA

- SUP 3: $3402.9 - 50-day EMA

- SUP 4: $3311.6 - Low Aug 20

Gold remains in a clear bull cycle and last week’s gains plus this week’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3474.7, the 20-day EMA.