GOLD: Cross-Market Pressure Pulls Spot Away From Fresh All-Time Highs

Oct-02 14:52

Gold extends the pull away from fresh all-time highs of $3,896.9/oz, which leaves round number resistance at $3,900/oz intact. Spot last $3.830/oz.

- Move seems to be a function of the stronger USD and an uptick in front end Tsy yields (detailed earlier).

- Profit taking could be exacerbating the move, bulls remain in technical control, first support at the Sep 30 low ($3,793.2/oz).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Expiries for Sep03 NY cut 1000ET (Source DTCC)

Sep-02 14:49

- EUR/USD: $1.1455(E2.2bln), $1.1525(E919mln), $1.1575-95(E1.5bln), $1.1600(E825mln), $1.1645-50(E792mln), $1.1675-80(E1.1bln), $1.1700(E1.1bln)

- USD/JPY: Y145.00($865mln), Y145.50($976mln), Y146.50($1.4bln), Y147.15-30($1.6bln), Y148.00($595mln), Y149.00($508mln)

- GBP/USD: $1.3500(Gbp507mln)

- AUD/USD: $0.6475(A$570mln)

US TSY FUTURES: BLOCK: Dec'25 5Y Sale

Sep-02 14:35

- -5,000 FVZ5 109-10.5, sell through 109-10.75 post time bid at 1028:33ET, DV01 $215,000.

- The 5Y contract trades 109-11.25 last (-3.75)

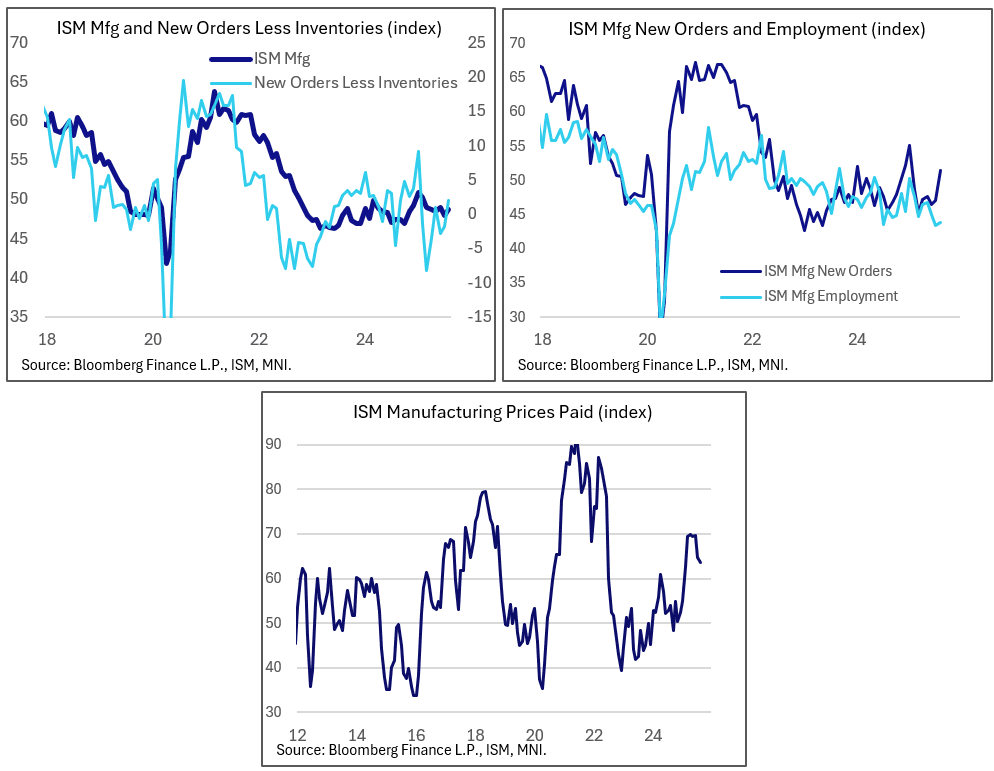

US DATA: ISM Manufacturing Improves On New Orders, But Tariffs Still Taking Toll

Sep-02 14:30

August's ISM Manufacturing report was weaker than expected on the headline figure, with some sub-components telling a slightly more mixed story, and price pressures unexpectedly diminished. Overall the ISM survey continues to portray a manufacturing sector that is failing to convincingly regain traction after the summer's tariff-related policy uncertainty. Indeed, tariffs were mentioned extensively in the sector-by-sector anecdotes in the report, and not in a positive light.

- The headline index ticked up a little less than expected, to 48.7 (49.0 expected, 48.0 prior) for a 6th consecutive sub-50 reading, notably with the improvement in the Employment sub-component disappointing at 43.8 (45.0 expected, 43.4 prior - per ISM, "panelists indicated that managing head counts is still the norm at their companies, as opposed to hiring").

- Additionally, Production took a big step back after 3 consecutive months of solid improvement, dropping to a 3-month low 47.8 (51.4 prior), consistent with negative Industrial Production and dragging on the headline figure.

- Conversely, the brightest note by far was unexpected strength in New Orders, which exceeded 50 for the first time since January (48.0 expected, 47.1 prior), as flagged by a solid performance in regional Fed surveys in this category. That was the biggest upside contributor to the overall ISM headline rise, though the commentary is decidedly less positive than the figure suggests: “Of the six largest manufacturing sectors, two (Food, Beverage & Tobacco Products; and Computer & Electronic Products) reported increased new orders. Despite the index’s move into expansion territory, for every positive comment about new orders, there were 2.5 comments expressing concern about near-term demand, primarily driven by tariff costs and uncertainty."

- Even so, this came as export orders ticked up 1.5 points to 47.6 for a 5-month high, though Imports fell 1.6 points to a 3-month low 46.0, suggesting weak trade dynamics overall.

- Inventories ticked up 0.5 points to reach a 4-month high 49.2, albeit still in contractionary territory. The differential between New Orders and Inventories reached 2 points, the highest since January - potentially indicative of improving future activity.

- Supplier Delivery times slowed (as indicated by the 51.3 reading, up 2 points from July which was the only month this year that indicated quickening delivery times).

- Another key surprise was in Prices Paid which dipped for a 2nd consecutive month, by 1.1 points to 63.7 (65.0 expected, 64.8 prior) - marking a 6-month low albeit still indicative of positive price pressures.

- As the above suggests, this was a very mixed report. The ISM categorizes these subcategories in terms of Demand (2 of 4 indicators improved - New Orders/New Export orders, vs Customers' Inventories and Backlog of Orders contracting at faster rates); Output (Production contracted, but Employment edged up), and Inputs (Supplier Deliveries, Inventories, Prices, Imports) which on net moved further into contraction.