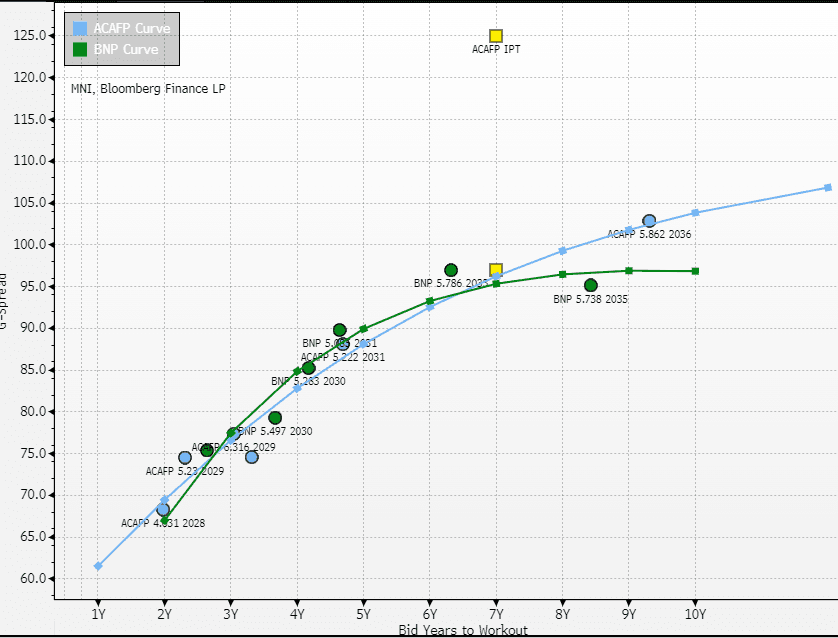

US CREDIT SUPPLY: Credit Agricole $Benchmark 8NC7 SNP +125 Area FV

(A1/A+/A+)

• FV 97a

• IPT 125a

• ACAFP SNP curve trades 1-2 bps inside closest comp BNP (Baa1/A-/A+) at 2031 maturities. BNP 5.786 1/33s trade at g97, and we adjust for duration to get to FV of 97a.

• Ratings: A3/A-/A+ (expected)

• Issuer: Credit Agricole SA (ACAFP)

• Format: 144A/Reg S, senior non-preferred

• Bookrunners: Credit Agricole Securities (USA) Inc.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GBPUSD TECHS: Bull Cycle Intact

- RES 4: 1.3753 High High Jul 2

- RES 3: 1.3681 High Jul 4

- RES 2: 1.3636 76.4% retracement of the Jul 1 - Aug1 downleg

- RES 1: 1.3595 High Aug 14

- PRICE: 1.3498 @ 15:56 BST Aug 19

- SUP 1: 1.3487 Intraday low

- SUP 2: 1.3448 50-day EMA

- SUP 3: 1.3400 Low Aug 11

- SUP 4: 1.3346 Low Aug 7

GBPUSD has pulled back from its latest highs but a bull cycle remains intact. Recent gains resulted in a breach of resistance at 1.3589, the Jul 24 high. Sights are on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1. A break of this retracement would strengthen the short-term bull theme. Initial firm support to watch lies at 1.3448, the 50-day EMA. A clear break would signal a possible reversal.

CANADA: July Inflation Data Keeps Analysts Eyeing A September BOC Cut

We didn't see any Bank of Canada rate view changes from Canadian institutions in the aftermath of the July CPI data, which was widely-acknowledged to have been softer than anticipated. A majority of analysts still see a September rate cut, though most/all suggest that it's dependent on the latest data trends (including a softer July jobs report) continuing between now and the the Sept 17 decision. Starting with institutions

- BMO (still expects September rate cut): "Overall, these results were nearly bang on our call, but still not good enough to prompt the BoC off the sidelines just yet. However, there still is one more full month of data, including one more CPI, before the Bank next decides on rates—so the door isn't slammed shut... [if the] more recent pace in core is maintained, and the economy remains soft, we believe that will eventually set the stage for BoC cuts."

- CIBC (still expects September rate cut): "Today's data supports our belief that the acceleration in inflation seen earlier in the year was linked largely to one-off factors, including an earlier than expected pass through from tariffs, and the slack that is evident in the Canadian economy is now starting to put renewed downward pressure on inflation. If the August data (released a day before the next Bank of Canada meeting) shows a similar trend, we expect that policymakers will be comfortable cutting interest rates by 25bp at the September meeting."

- Desjardins (still expects September rate cut): "Reading between the lines of the BoC’s most recent interest rate announcement, it seemed clear that policymakers would be open to cutting rates to support the weakening economy and labour market if underlying inflation was to start moving in the right direction. With this in mind, the easing of underlying price pressures in the July inflation report may have been just what the doctor ordered. As such, it reinforces our view that the BoC is more likely than not to cut the policy rate at its upcoming meeting in September—an outcome that markets have not yet fully priced in."

- National (still expects September rate cut): "while the Bank of Canada will likely view it as mildly positive, it is unlikely to be a game-changer. As such, we believe that the BoC will only be confident enough to cut policy rates again this year if the unemployment rate continues to rise, which is our baseline scenario."

- TD (still expects September rate cut): "The BoC's preferred measures of core inflation are still running near 3% y/y, but the deceleration across 3m core inflation rates should give the Bank some new conviction that inflation pressures have been contained. This should keep an open path to a September rate cut, although this progress will need to be sustained through the August CPI report."

- RBC (still sees no further BOC cuts): "rates of price increases are smaller than what we expected - we had looked for persistent strength in services components to again show up, echoing resilience seen in consumer spending broadly to-date. Still, one reading doesn't make a trend...From the Bank of Canada’s perspective, the easing this month is welcome. However, they have also already cut interest rates significantly over the last year and will need to consider the potential impact of expected government spending increases as a more effective policy response to U.S. tariffs than further changes in interest rates. Labour markets in Canada have softened but as we look not much further for a bottom of conditions, we don't expect the BoC will cut again in this cycle."

- Scotiabank (still sees no further BOC cuts this year): "there are two main issues with data reliability. One concerns Statcan’s seasonal adjustments. The other concerns wild revisions....In any event, based on the data as it stands now, those are not light core inflation readings, and they’re definitely not undershooting the BoC’s 2% inflation target, but they are back in the confines of the BoC’s 1–3% target range for headline inflation while using core gauges as the more stable way of operationalizing achievement of this target range. That balances the risks to the rate outlook a little more than previously. The BoC couldn’t base further easing from what is already a roughly neutral policy rate on such numbers in my opinion. They would either need more evidence of downside risk to inflation tracking that may or may not arrive with further data, or high confidence in their ability to forecast price pressures which doesn’t seem to be in vogue at the BoC that continues to avoid a base case projection."

FOREX: CAD Weakens Post CPI, Softer Equities Weigh on AUD & NZD

- Despite some initial weakness on Tuesday, the USD index tilted back into positive territory late in the session, set to moderately extend the rally this week. Price action was assisted by a dip lower for the major equity benchmarks, as a cautious risk off mood prevails given the lack of progress regarding a Russia/Ukraine ceasefire and the notable weakness for tech stocks in the US.

- Canada inflation data came in slightly below expectations and while unlikely to prompt renewed easing from the BOC, the Canadian dollar has sold off today. USDCAD has risen 0.4% to 1.3860, closing in on the August 01 highs off 1.3879. A break of this level would cancel a bear threat and resume the recent bull cycle.

- Elsewhere, risk dynamics have negatively impacted the likes of AUD and NZD, while Norwegian Krone is at the bottom of the G10 leaderboard.

- For AUDUSD, the pair is comfortably off its most recent highs but continues to trade in a range. From a trend perspective, the condition remains bullish highlighted by MA studies that remain in a bull-mode position; however, spot has narrowed the gap substantially to key support at 0.6419, the Aug 1 low.

- Kiwi weakness is notable ahead of Wednesday’s RBNZ decision, recording the first print below 0.5900 in two weeks. With a 25bp cut widely forecast, attention will be on the revised RBNZ outlook and tone of the statement and press conference. The focus is likely to be on the projected OCR path and whether it is revised lower suggesting further easing towards stimulatory territory as excess capacity persists.

- GBPUSD has consolidated around the 1.35 mark on Tuesday amid gilts paring some of yesterday's weakness. A technical bull cycle remains intact, keeping sights on 1.3636, the 76.4% retracement of the bear leg between Jul 1 and Aug 1 ahead of tomorrow's UK CPI release.

- FOMC minutes are also due for release tomorrow before the Jackson Hole symposium kicks off Thursday.