GERMANY: Council of Economic Experts Calls For New Pension Savings Account

Members of the German Council of Economic Experts are calling on the federal government to introduce a new model of subsidized private pension provision in a FAZ op-ed. An introduction of the proposal would likely be accompanied by capital allocations rotating out of fixed income securities towards equities. Over E100bln is held in the Riester funds.

- "The core of the pension savings account should be a simply structured standard product, similar to the one created in Sweden", replacing the so-called "Riester pension" in place previously. "Existing Riester contracts should be transferred smoothly to the new system on a voluntary basis."

- The Swedish system referred to is the so-called "premium pension" system, where 2.5% of gross wages are diverted into an individual funded account. Savers can choose to invest this money in a menu of approved mutual funds (equities, bonds, mixed), and if they don’t make an active choice, the money is automatically invested in a state-run default fund (AP7 Såfa).

- While the realized capital allocation under the new system would be subject to uncertainty as per the user choice, a key criticism of the "Riester pension" was that allocations tended to be too conservative - on the margin, the council's proposals would likely be associated with a rotation from fixed income securities towards equities as a function of that.

- The German Council of Economic Experts is a mandated body providing economic policy advice to German policymakers. The German government is more generally working on pension reform, with the "active pension" (tax-free labour for <E2000/month for workers having reached pension age) being scheduled for parliament passing, and public pension reform proposals also being floated recently.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

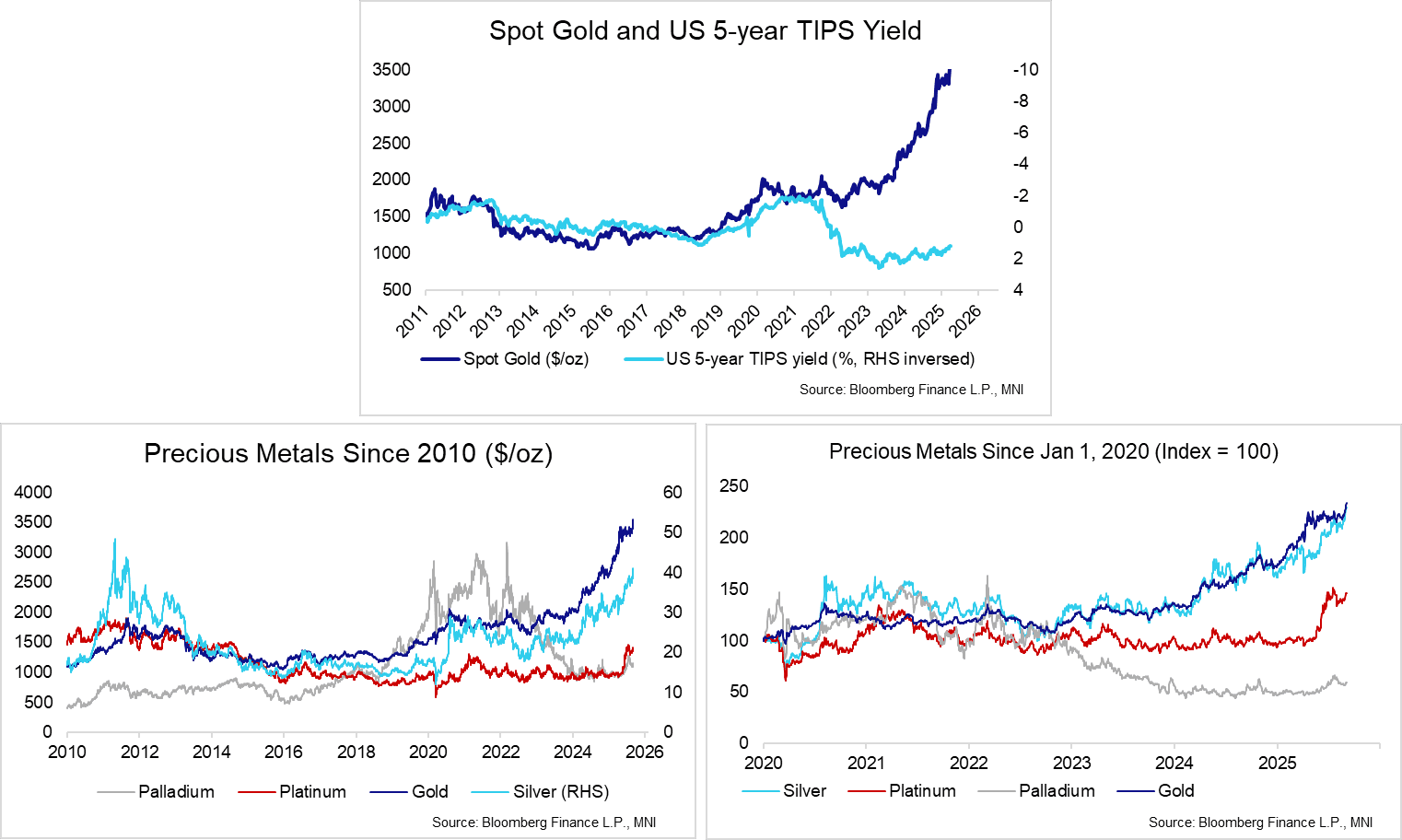

GOLD: Pushes To Fresh All Time High

Spot gold pushes to a fresh all-time high of $3,556/oz, with bullion now up ~7.5% from the August 20 low. Spot is on track for its longest streak of daily higher highs since 2022, which was only previously surpassed in 2017. Clearly, gold remains in a technical bull cycle, which has been strengthened by the breach of key prior resistance at $3500.1, the Apr 22 high. The next objective is the $3600.00 handle.

- Gold’s breakout over the past few weeks has been spurred by fresh concerns around Fed independence amid the ongoing Governor Cook saga. Meanwhile, fears around fiscal pressures (and the associated threat of future government debt monetisation) continue to provide a background tailwind. There hasn’t been an obvious specific driver of today’s 0.65% rally.

- World Gold Council data on August’s ETF flows and central bank purchases should be released later this month.

- Silver’s recent price action has also been impressive, with spot pushing through $40/oz yesterday before consolidating around $41 today. The next objective is $41.064, the 1.764 projection of the Apr 7 - 25 - May 15 swing.

BONDS: German Curve unwinds all the steepening bias

- Continued unwind in the German, in the back of the Buxl leading the Gains in Germany.

- After reaching its steepest level since March 2019 the 5s/30s is back below Opening levels.

- US Cash Tsys is also richer, while the belly underperforms, and curves are leaning flatter.

- Saw the Initial small resistance moving down to 129.18 in Bund, and this level has so far held, printed a 129.16 high.

BOE: Lombardelli: Neutral could be close to (or at) 4%

Lombardelli's comments are significant. She is saying that neutral could be close to (or at 4%). And she is deviating from the wider Bank guidance that rates are still "meaningfully restrictive." Highlights on her views below:

- In August "I judged it appropriate to pause the reduction of monetary restriction, due to my concerns about the current and expected above-target rates of underlying inflation and my judgements about the balance of supply and demand in the economy. I preferred to maintain the level of monetary restriction for longer rather than continue to reduce it at the previous pace."

- "At the time of the August decision headline inflation was 3.6% and it is expected to remain roughly between 3.5 and 4.0% for the remainder of this year. This is driven in part by inflation in food and energy - the most salient prices - and comes after a long period of relatively high inflation. This increases the risk of an inflation persistence scenario such as the one we considered in May."

- "It is less clear if the disinflation process is continuing in services prices"

- "While previous policy restrictiveness continues to weigh on the economy, I am less confident that the current policy stance as embodied in the market curve continues to be meaningfully restrictive. At the time of the August MPC vote, we had reduced rates by 100 basis points and I judged that there might not be that much further to go before the current policy stance is effectively neutral. Looking at history, it’s plausible that neutral may be closer to the upper end of the 2-4% range from Bank analysis. If so, this would mean we don’t have many more rate cuts to go as we potentially approach the end of the cutting cycle. I am not predicting that we are already at neutral, but nor am I confident that if we reduce restrictiveness much further we will still be sufficiently restrictive to return inflation to target sustainably."