EURGBP TECHS: Corrective Pullback

- RES 4: 0.8769 High Jul 28 and the bull trigger

- RES 3: 0.8744 High Aug 7

- RES 2: 0.8728 76.4% retracement of the Jul 28 - Aug 14 bear leg

- RES 1: 0.8713 High Sep 2

- PRICE: 0.8653 @ 16:30 BST Sep 10

- SUP 1: 0.8636/8597 50-day EMA / Low Aug 14 and the bear trigger

- SUP 2: 0.8562 50.0% retracement May 29 - Jul 28 upleg

- SUP 3: 0.8540 Low Jun 30

- SUP 4: 0.8514 61.8% retracement May 29 - Jul 28 upleg

EURGBP traded lower Tuesday and has breached the 20-day EMA. Short-term weakness is considered corrective - for now - and support to watch lies at 0.8597, the Aug 14 low. Clearance of this level would reinstate a recent bearish threat. A resumption of gains would open 0.8744, the Aug 7 high. Key resistance and the bull trigger is at 0.8769, the Jul 28 high. Note that MA studies are in a bull-mode position highlighting a dominant uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Limited Trade To Open Week, With Sonia Upside Faded Pre-Labour Data

Monday's Europe bond/rate options flow included:

- SFIH6 96.70 calls 3.5K given at 5

US OUTLOOK/OPINION: Analyst Expectations For Sequential Drivers In July CPI

Core CPI sequential drivers in July are expected to come from used cars increasing modestly after a weak run plus travel-related services with lodging away from home pausing after declining and airfares increasing after broadly pausing.

- Lodging away from home (+ve): Seen broadly unchanged on the month after a heavy -2.9% M/M in June that subtracted -0.05pps from core CPI.

- Used cars (+ve): There’s a reasonable range of estimates for used car prices in July, from -0.5% to +0.7% but they all are stronger than the -0.7 M/M seen in June. The average estimate is 0.24% M/M after four months averaging -0.6% M/M.

- Airfares* (+ve): Seen rising 1.5% M/M after -0.1% in June following a period of prolonged, large declines with an average -3.7% M/M through Feb-May. The range of views of -0.4% to 2.5% is one of the narrower in recent months.

- Apparel (neutral to small +ve): Median of 0.5%/average 0.44% having accelerated to 0.43% M/M in June from a surprisingly soft -0.4% M/M in May.

- Vehicle insurance* (neutral to small +ve): Once again only three estimates this month with a decent range of -0.1% to 0.6% M/M. The average of 0.2% M/M would be a slight acceleration from the 0.1% in June but it’s a category that can swing from month to month with a sizeable 3.5% weight in core CPI.

- Rents (neutral): Owners’ equivalent rent (OER) seen dipping to an average 0.28% (range 0.25-0.30) after 0.30% in June, but with primary rents firming to an average 0.26% (range 0.22-0.34) after 0.23%.

- Non-core: Food (small -ve): Food price inflation is seen easing to 0.25% M/M in July after 0.33% M/M. Food away from home has continued a robust run recently, with 0.40% M/M in June and a 1H25 average of 0.36% (feeding into core PCE but not CPI). Food at home meanwhile has seen two months averaging 0.27%.

- Energy (-ve): Energy prices are seen falling circa -0.6% M/M after a 0.95% increase in May, driven by a more than 2% M/M decline in seasonally adjusted gasoline prices.

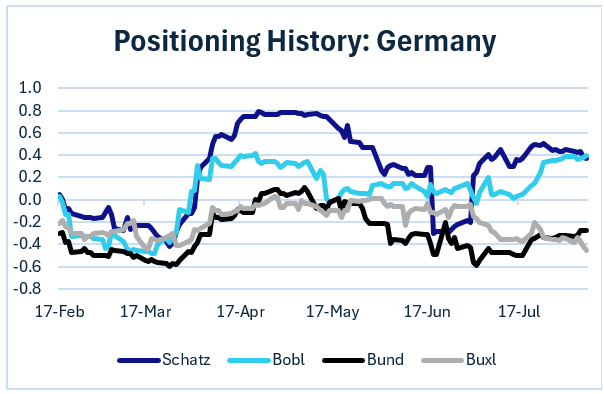

BONDS: Europe Pi: German Positioning Mixed (1/2)

From our latest Europe Pi futures positioning update (PDF):

- German contracts' structural positioning has been relatively steady since late July, with some subtle shifts. Schatz remains in "long", though has failed to pierce "very long" territory. Bobl has shifted into long territory alongside.

- Bund and Buxl remail short as with the last update.

- Shorts were set across 3 of 4 contracts last week, with the exception being Buxl (longs reduced).