MEXICO: Core CPI Inflation Rises To 4.28% Y/y In September, As Expected

- "*MEXICO SEPT. CONSUMER PRICES RISE 0.23% M/M; EST. +0.26%" - BBG

- "*MEXICO SEPT. CONSUMER PRICES RISE 3.76% Y/Y; EST. +3.78%"

- "*MEXICO SEPT. CORE CPI RISES 0.33% M/M; EST. +0.33%"

- "*MEXICO SEPT. CORE CPI RISES 4.28% Y/Y; EST. +4.28%"

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Bear Threat In Oil Futures Still Present

- On the commodity front, Gold remains in a clear bull cycle and last week’s gains plus Monday’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a 2.382 projection of the Dec 30 ’24 - Apr 3 - 7 price swing. Initial firm support lies at $3458.7, the 20-day EMA.

- In the oil space, the trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from last Tuesday’s high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

EGB SYNDICATION: Mandate: Luxembourg New 10-year

"The GRAND DUCHY OF LUXEMBOURG, rated Aaa/AAA/AAA (all stable), has mandated BofA Securities, BCEE, Credit Agricole CIB, Deutsche Bank and Societe Generale as Joint Lead Managers for its upcoming new 10-year Euro-denominated senior fixed rate benchmark due 17 September 2035. The transaction is expected to be launched and priced in the near future, subject to market conditions. RegS only, Bearer form, CAC, FCA/ICMA stabilisation. The target market for the Bonds is professionals, retail and eligible counterparties (all channels for distribution), each as defined in MIFID II/UK MiFIR."

From Market source

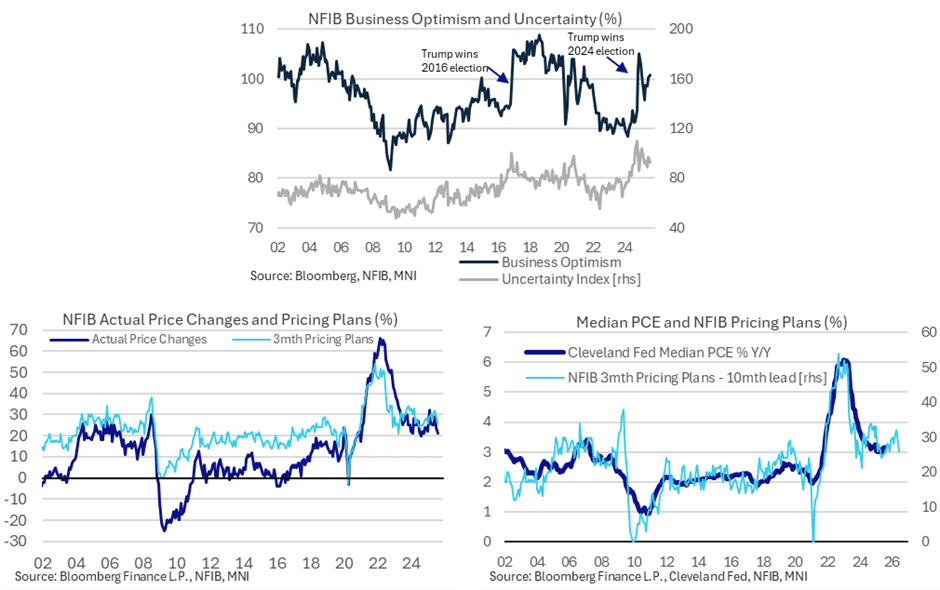

US DATA: Small Businesses Imply Largest Tariff Price Increases Have Passed

Small business optimism continued its improvement from lows seen after April tariff announcements in August. Both backward- and forward-looking price metrics pulled back further after some recent increases although a longer-term trend remains one at a level above that consistent with the 2% inflation target.

- The NFIB small business optimism index firmed slightly more than expected in August as it ticked up to 100.8 (cons 100.5) from 100.3 in July for technically its highest since January.

- It extends what has been a trend recovery from the 95.8 seen after reciprocal tariff announcements in April. For context, the index saw a recent high of 105.1 in December, fully reflecting US election results, an average of 93 in 2024 and a very long-term 52-year average of 98.

- Ahead of Thursday’s US CPI report for August, the net share who increased prices compared to three months ago fell for a second month to 21% (lowest since Oct 2024) vs 29% in Jun and a recent high of 32% in Feb.

- It’s below the 23% averaged in 2024 but remains above pre-pandemic averages of ~12%.

- Also on the softer side, the net share expecting to increase prices over the next three months fell for a second month to 26%, the joint lowest since Sep 2024, having recently peaked at 32% in June.

- It’s back below the 28% averaged in 2024 but remains above the 22% averaged pre-pandemic.

- The two price metrics therefore point to some cooling in price pressures after an initial firming in the early stages of the second Trump administration, although from a longer-term trend perspective they continue to point to some stabilization at level above those historically consistent with 2% inflation.