EU CONSUMER STAPLES: Consumer & Transport: Week in Review

IG held firm even as HY widened 10–30bps, opening interesting RV across the IG/HY divide. Potential rising stars like Levi’s start to screen value, while pressure builds on earnings for at-risk HY names such as Electrolux and Coty. Next week’s earnings calendar is light but includes key names LVMH, Pernod and Nestlé.

- Südzucker reported 2Q results a month after cutting FY guidance and still guided toward the lower half of the range. Cash flows were supported by WC measures, but we still see leverage rising ~2x this year on continued earnings falls.

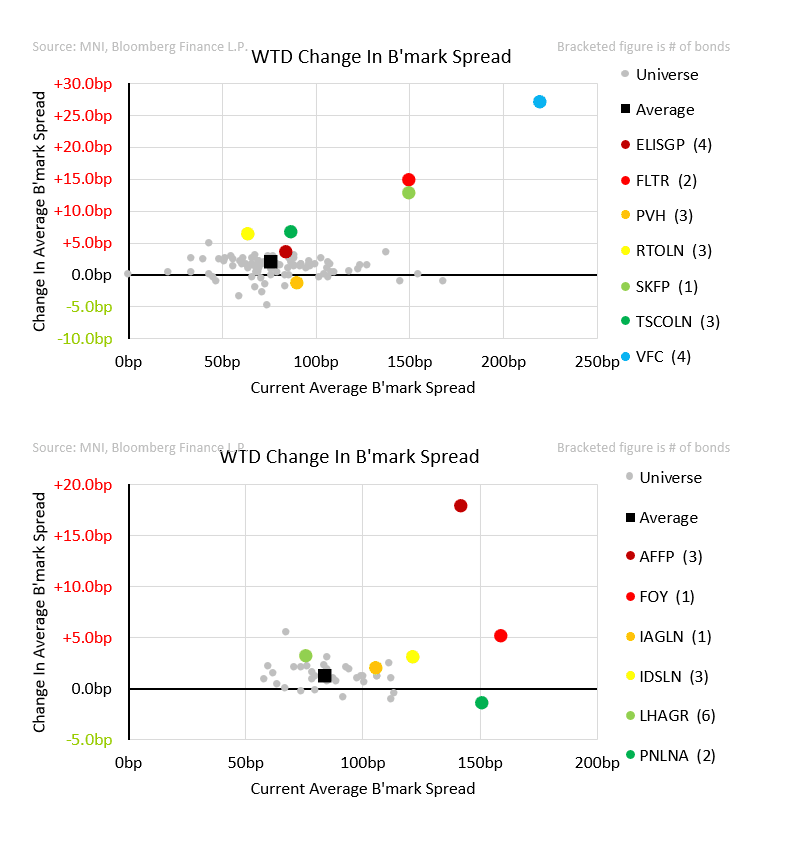

- Flutter fell another 4% as excitement around growth in prediction-markets continued; NYSE owner ICE took a $2bn stake in Polymarket, valuing it at $8bn, while Kalshi raised $300m at a $5bn valuation—more than double the valuation from earlier this year.

- Pandora is facing a historic rise in silver. High hedging levels will delay the impact, but we estimated a 250bps headwind on the 24% medium-term EBIT margin target if Silver held at $50/oz. We still view the credit as a firm name but see catalyst skewed negative now.

- Pepsi posted LSD organic growth, driven by international beverages and LATAM food. NA volumes—especially in foods—remained weak. Activist Elliott was expected to push for NA brand divestitures.

- Barry Callebaut estimates were revised by us with leverage lowered ~0.8x on better realised cocoa prices. Softer cocoa (on higher farmer prices and favourable weather) could help Barry preserve IG ratings.

- B&M reported LFL falls with margin targets reset 200-300bps lower as the new CEO targets more aggressive pricing. We await the Nov update to firm up a view.

- Levi raised FY guidance again on continued high-single digit organic growth. Strength in non-core Women’s and bottoms should be taken positively by agencies. We see rating upside and see levels as interesting.

- Groupe SEB cut guidance again as 3Q sales turned negative.

- Mars acquisition of Kellanova is set to receive EU regulatory approval according to Reuters leaks. If so it would unlock a 3-notch upgrade for K bonds and remove the 101 SMR risk on newly issued USD bonds.

- Pernod Ricard held onto Baa1 ratings at Moody’s. The agency points to €7b in aged inventories as support for credit. We note growth has lagged peers and still see near term catalyst skewed negative.

- Woolworths was reaffirmed at Baa2 Stable at Moody’s as the agency, like S&P, notes ample rating headroom. We see levels as interesting but near term catalyst skewed slightly negative.

- VFC was affirmed at BB flat by S&P in a more optimistic take than Moody’s. Company schedules earnings for 28 Oct.

- Primary (NIC in brackets): Autostrada Torino-Milano 6.3y (+2), Tesco 8y (+3)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US EIA: CRUDE OIL STOCKS EX SPR +3.94M TO 424.6M SEP 05 WK

- US EIA: CRUDE OIL STOCKS EX SPR +3.94M TO 424.6M SEP 05 WK

- US EIA: DISTILLATE STOCKS +4.72M TO 120.6M IN SEP 05 WK

- US EIA: GASOLINE STOCKS +1.46M TO 220.0M IN SEP 05 WK

- US EIA: CUSHING STOCKS -0.36M TO 23.9M BARRELS IN SEP 05 WK

- US EIA: SPR +0.51M TO 405.2M BARRELS IN SEP 05 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +0.6% TO 94.9% IN SEP 05 WK

SCANDIS: Fresh Strength For NOK and SEK Since the US Equity Open

Fresh strength seen for Scandi FX since the US cash open, seemingly a function of the broader dollar pullback post-US PPI rather than in response to any fresh domestic catalyst. NOK and SEK outperform the G10 basket on an intraday basis.

- USDNOK (-0.9%) is narrowing the gap to the June 17 low at 9.8615, clearance of which would expose the December 2022 low at 9.6982.

- A reminder that this morning’s August inflation report was stronger-than-expected, driving a 7bp intraday rise in 2-year NOK swap rates and placing heightened focus on tomorrow’s Q3 Regional Network Survey. A Norges Bank hold next week is still possible if that survey is hawkish.

- USDSEK meanwhile has registered a fresh multi-year low, with support seen at 9.2307 (March 2022 low).

- Tomorrow’s Swedish calendar includes the final August inflation report, details of which will be important to judge the likelihood of a September rate cut. With Riksbank Deputy Governor Jansson not coming across as overtly dovish following the lower-than-expected flash release last week, the Executive Board could decide to keep rates steady in September, and save some dry powder for later this year if required.

- Riksbank Governor Thedéen also speaks tomorrow at 1200BST. The topic of the speech is banking sector liquidity.

GLOBAL: MNI Tech Trend Monitor - Highlighting Key Longer-Term Trends

MNI Tech Trend Monitor: https://emedia.marketnews.com/marketnewsintl/MNITechTrendMonitor.pdf

We introduce the MNI Tech Trend Monitor - This document highlights a selection of key longer-term trends that we have identified in markets that could be reaching inflection points, trend reversals/extensions or technically significant levels.

Covering:

- UK Gilt 10y Yield

- UK Gilt 30y Yield

- ICE USD Index

- Europe Banking Stock Index (SX7E)