ASIA: Coming Up in Asia Today

| 0130GMT | 0830HKT | 1030AEDT | Singapore Electronic Exports YoY June |

| 0130GMT | 0830HKT | 1030AEDT | Singapore Non-Oil Domestic Exports YoY JUNE |

| 0930GMT | 1630HKT | 1830AEDT | Hong Kong Unemployment Rate SA |

source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Coming Up in Asia Today

| 0130GMT | 0830HKT | 1030AEDT | Singapore Electronic Exports YoY MAY |

| 0130GMT | 0830HKT | 1030AEDT | Singapore Non-oil Domestic Exports YoY MAY |

| 0930GMT | 1630HKT | 1830AEDT | Hong Kong Unemployment Rate SA MAY |

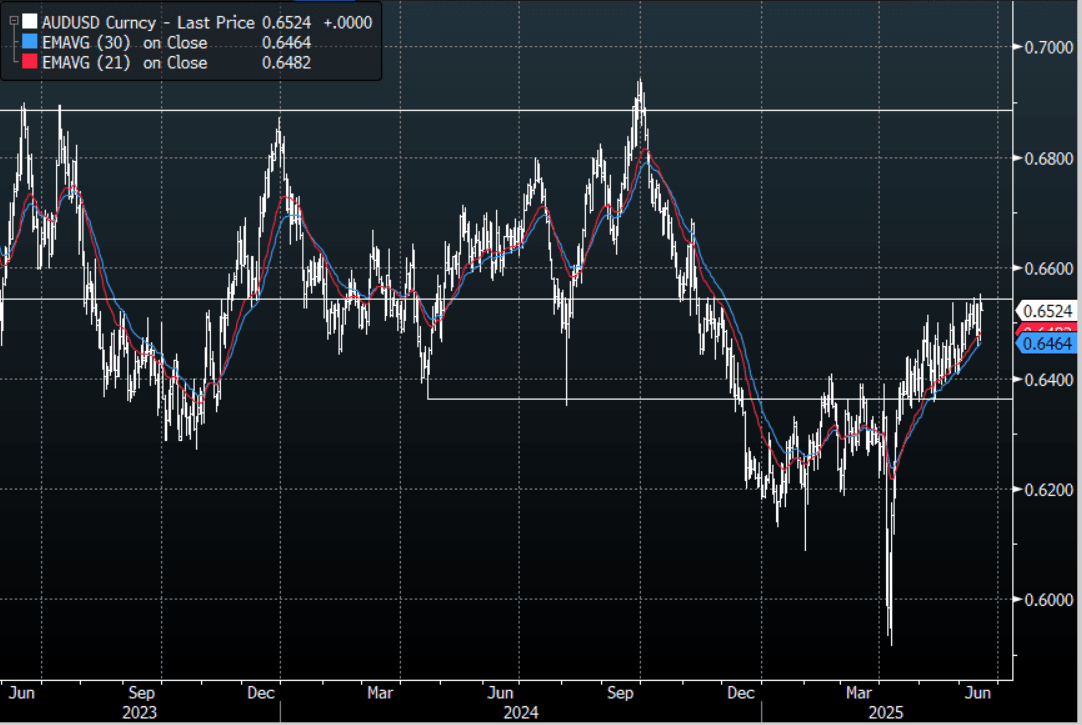

AUD: AUD/USD - Trying To Break Higher

The AUD had a range overnight of 0.6490 - 0.6552, Asia is opening around 0.6525. The AUD bounced nicely overnight and is back to retesting its recent highs. This comes as US stocks continue to confound and grind higher and the USD’s reprieve was very short-lived and has come back under pressure.

- (Bloomberg) -- Australian Treasurer Jim Chalmers notes that higher oil prices pose a risk to both inflation and global growth, and that Australia's central bank may cut interest rates to mitigate the impact of the global volatility.”

- “US State Department approves a possible foreign military sale to Australia at an estimated cost of $2 billion. The sale includes F/A-18F and EA-18G sustainment support and related equipment, the statement says.”

- The AUD saw good demand sub 0.6500 and is back to testing the 0.6550 area.

- Price remains in the 0.6350 - 0.6550 range for now, a sustained break above 0.6550/0.6600 is needed for the move higher to accelerate. The way the USD is trading across the board points to this being tested at some point.

- Expect buyers to continue to be around on dips while the support in the AUD/USD holds, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6600(AUD 1.1b June 19)

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though continued to build up their shorts again.

Data/Event: Westpac Leading Index, Tomorrow is Unemployment

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA DATA: Goldman's Sees Upside Risks To H1 GDP Forecast

The global bank sees upside risks to its H1 China GDP forecast post yesterday's May data outcomes, but cautions on the sustainability of stronger retail spending. It also sees further policy support is likely needed in H2. See below for more details.

Goldman Sachs: "Retail sales growth rose meaningfully in May, with year-on-year growth in home appliance and communication equipment sales value jumping to 53% and 33%, respectively from 39% and 20% in April, as an earlier-than-usual "618" online shopping festival this year has pulled forward some demand from June to May. However, we caution that such an improvement may not be sustainable in June due to payback effects and funding shortages of consumer goods trade-in program in some regions. In our view, China's May activity data highlighted the importance of government policy for domestic demand (e.g., consumer goods trade-in program), continued deflationary pressures (e.g., strong real auto production and weak nominal auto sales), and a prolonged property downturn. Incorporating April-May activity data, we see a slight upside risk to our Q2 real GDP growth forecast of 5.0% yoy. Given the persistent property weakness, increased labor market stress and the unsustainability of both consumer goods trade-in program and export frontloading, we believe additional policy easing is still necessary in H2, though the urgency for significant stimulus in the near term appears lower thanks to the better-than-feared macro data so far."