ASIA: Coming Up In Asia Pac Markets On Thursday

Jul-16 21:00

| 2330BST | 0630HKT | 0830AEST | Fed's Williams Speaks On Economic Outlook |

| 2345BST | 0645HKT | 0845AEST | New Zealand June Food Prices |

| 0050BST | 0750HKT | 0950AEST | Japan June trade Balance |

| 0050BST | 0750HKT | 0950AEST | Japan Weekly Investment Flows |

| 0130BST | 0830HKT | 1030AEST | Australia Bill Sale |

| 0200BST | 0900HKT | 1100AEST | Australia July Consumer Inflation Expectations |

| 0230BST | 0930HKT | 1130AEST | Australia June Jobs Data |

| 0335BST | 1035HKT | 1235AEST | New Zealand 2030, 2036, 2041 Bond Sale |

| 0430BST | 1130HKT | 1330AEST | Japan 1yr Bond Sale |

| 0600BST | 1300HKT | 1500AEST | Japan June Tokyo Condominiums For Sale |

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

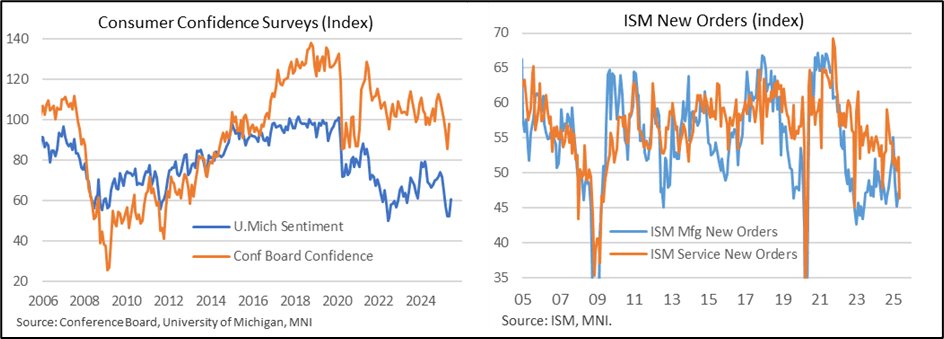

US OUTLOOK/OPINION: Macro Since Last FOMC: Growth - Mixed Shifts In Sentiment

Jun-16 20:49

- Compared with the approach to the May meeting, surveys again look weaker than the hard data but the gap has narrowed in places.

- That’s more so for the consumer, where sentiment has seen a lift since the de-escalation in US-China trade tensions on May 12, a finding supported in both U.Michigan and Conference Board surveys.

- Business sentiment has deteriorated further though, at least when looking at the ISM surveys. The manufacturing index inched another 0.2pts lower to 48.5 in May (lowest since Oct 2024) whilst the ISM non-manufacturing index fell a more notable 1.7pts to 49.9 (first sub-50 reading since Jun 2024).

- New orders stood out in the latter, sliding 5.9pts to 46.4 for their lowest since Dec 2022 at levels not sustainably seen outside of the pandemic depths or 2008-09.

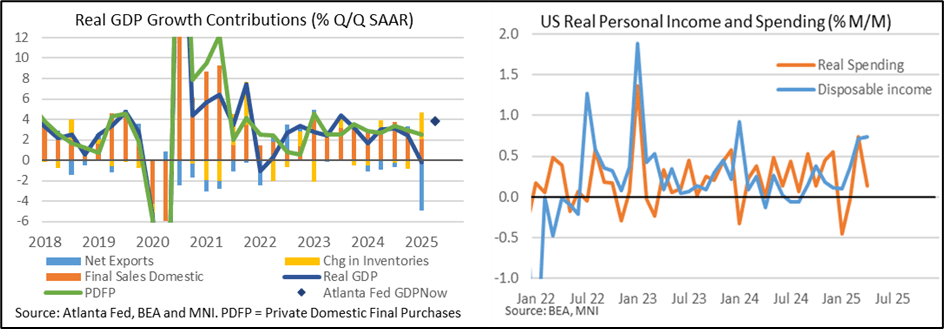

US OUTLOOK/OPINION: Macro Since Last FOMC: Growth - Slightly Softer Hard Data

Jun-16 20:47

- Whilst now particularly stale, we start with latest estimates of Q1 national accounts as the revisions in the second update made on May 29 only partly played out as Fed Chair Powell had suggested at the May press conference.

- Real GDP growth was near enough unrevised at -0.24% annualized (vs an initial -0.27%) in Q1 to confirm a sidelining in GDP after 2.4% in Q4 and 3.1% in Q3. There were large offseting revisions though; personal consumption was surprisingly cut from 1.8% to 1.2% annualized, dragging 0.4pp from GDP growth in the process, but fully offset by an even larger boost from inventories on tariff front-running. It left inventories adding 2.6pps to GDP growth compared to the huge -4.9pp drag from net exports.

- Powell had said that it’s “very likely you'll have restatements of the first quarter. It'll turn out that consumer spending was higher. It will turn out that inventories were higher. And so you'll see -you'll see those data revised up. It may actually go into the third quarter, too. And so I think it's going-this whole process is going to, a little bit, make it harder to make a clean assessment of U.S. demand." One takeaway that can we make though is that private domestic final purchases - a category Powell has previously focued on – is now estimated to have increased 2.5% annualized in Q1 vs the 3.0% referenced by Powell at the last meeting for what at the time had impressively looked like no moderation from the 3.0% averaged through 2024.

- New data also reveal that gross domestic income contracted -0.2% annualized in Q1, the weakest in nine quarters for a sharp reversal from Q4’s twelve-quarter best of 5.2%, in signs of broader economic weakness that can’t just be attributed to lower net exports.

- More timely hard data meanwhile have shown resilience in consumer spending and especially incomes, although softer business activity.

- Specifically, real consumer spending was a little better than expected and still managed to increase 0.1% M/M in April after a strong 0.7% M/M in March, whilst real personal disposable incomes surprisingly increased a second consecutive 0.7% M/M. While there were some worrying signs in terms of latest consumer momentum, particularly in services purchases, the employee income growth which has driven much of the economic expansion has not shown any signs of abating going into Q2. The May retail sales report lands on day one of the two-day FOMC meeting.

- On the capital goods side, core shipments saw a modest pullback with -0.1% M/M in April after two strong months that match tariff front-running more broadly. However, core orders point to more notable weakness ahead in production with -1.5% M/M for the single weakest month since early 2023. Add in a larger than expected correction lower in imports in April after Q1’s surge and the Atlanta Fed’s GDPNow currently projects real GDP growth rebounding with 3.8% annualized in Q2.

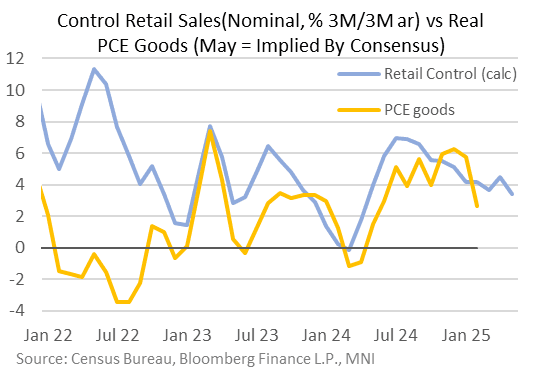

US OUTLOOK/OPINION: Analysts See Control Group Picking Up M/M In May (2/2)

Jun-16 20:21

As usual we expect the GDP-input Control Group sales to be the most closely watched part of the retail sales release - many analysts are centered around a 0.3% M/M (SA) advance in May's report. That would be an improvement from -0.18% but would still see the quarterly rate (3M/3M SAAR) pull back to a 13-month low 3.4%, after 4.5% in April, albeit those are both in nominal terms.

- A few comments by analysts, in alphabetical order:

- BofA (Control Group 0.0%): "Still in limbo...we forecast flat readings on both retail sales ex-autos and the control group"

- Citi: "We expect total retail sales to decline by 0.6%MoM mainly due to auto sales normalizing after some front loading in March and April. Control group sales should hold up better with strength driven narrowly by nonstore sales...A combination of trade-related uncertainty and pay-back from front-loaded activity should lead to softer economic conditions in coming months."

- Deutsche (Control Group +0.3%): Headline sales (-1.0%) should be pulled down by the drop in unit motor vehicle sales last month, while ex-autos (Unch) will likely see a drag from gasoline prices. However, we expect retail control (+0.3%) to rebound. As always, it will be important to pay attention to revisions."

- NatWest (Control Group +0.3%): "We expect (nominal) retail sales likely fell by -1.0% in May..we expect weakness in auto sales and gasoline station receipts weighed... In contrast, core retail sales which exclude autos and gas, likely rose by 0.3%m/m in May... we suspect retail sales in line with our forecasts are likely to translate into a small positive increase in real spending for May. This would put quarter-to-date (through May) average up at a strong 3.0%q/q, ar pace versus Q1 average (though slightly lower than the 3.7%q/q, ar pace at end of April)."

- TD (Control Group +0.3%): "Contracting auto sales will weigh on total US retail sales in May despite our expectation for a 0.3% m/m rebound in the control group segment. Auto sales are in the process of normalization following the front-loading of spending that lifted the series in March and April. Food services spending (bars & restaurants) likely also fell as well following firm increases in the last two reports."

- UBS (Control Group +0.3%): "We expect retail and food services sales fell 0.2% in May, with the headline held back by weaker auto sales...Ex-autos should look better, up 0.2% in May, with a similar 0.2% increase for ex-autos and ex-sales at gasoline stations...looking at the seasonal patterns in recent years, we have tended to see relative strength in control group sales in the month of May. However, this year the risks are more two sided."