EM LATAM CREDIT: Colombia: Petro Administration Seeking Constitutional Changes

[MNI Macro]

Re the earlier Colombia headlines, the government has presented a bill calling for a Constituent Assembly, with details being released in a video on social media by Justice Minister Eduardo Montealegre. The link to the post is here: https://x.com/MinjusticiaCo/status/1981306191377465539

• According to the post, the document is the starting point for building upon the foundations for the transformation Colombia requires, and through the confrontation of arguments, not violence, “we will envision a new country”. The minister states it will be “the space to promote the entire social program that the cavern has prevented the first leftist government in our history from developing”.

• President Petro called for a collection of signatures this Friday for the “constituent power” in Bogotá’s Plaza de Bolívar.

• It is worth noting that the mechanism established to amend the Constitution requires, first, approval by Congress, followed by a review by the Constitutional Court, and only then, a submission to a popular vote. Therefore, any substantial progress to Petro’s social program will likely encounter plenty of short- and medium-term obstacles.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

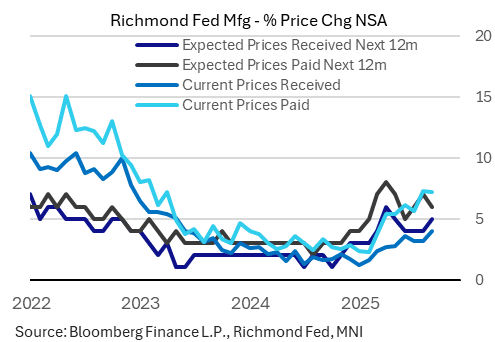

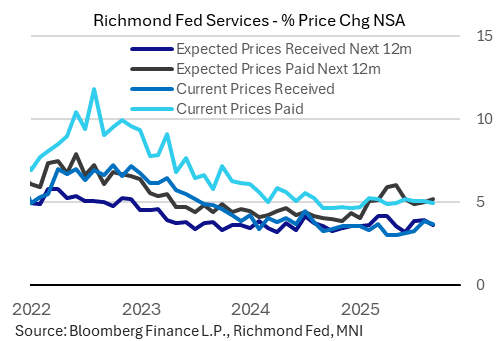

US DATA: Richmond Fed: Price Developments Mixed In September (2/2)

The Richmond Fed surveys' inflation subcomponents were somewhat mixed in September, with continued pressures more apparent for manufacturers than for services firms. Note that the Richmond Fed reports its price indices differently from the other regional banks, expressing them in percentage changes over the last / next 12 months.

- Manufacturing prices remained stubbornly high: current prices paid stayed at 7.2% for a second consecutive month (August's was a 27-month high), with prices received picking up sharply to 4.0% - the latter marking a 27-month high (and a potential sign that manufacturers are passing through tariff costs).

- Expected prices paid dipped to 6.0% however from 7.0%, with received up to 5.0% after four months at 4.0%.

- Services price inflation was better-behaved. Current paid dipped to 5.0% from 5.1%, marking a 4-month low, with prices received at a 2-month low 3.7% after August's 3.9% was the highest in over a year.

- Expected prices paid ticked up to 5.2% from 5.0%, though expected received fell to 3.6% from 4.0% for a 3-month low.

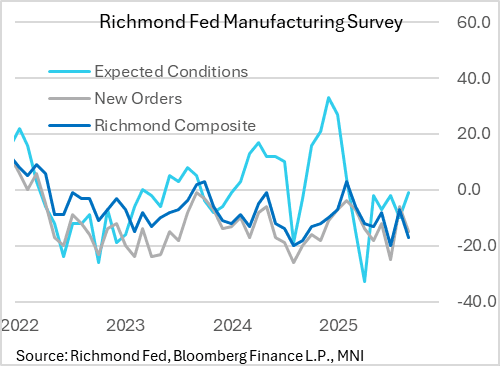

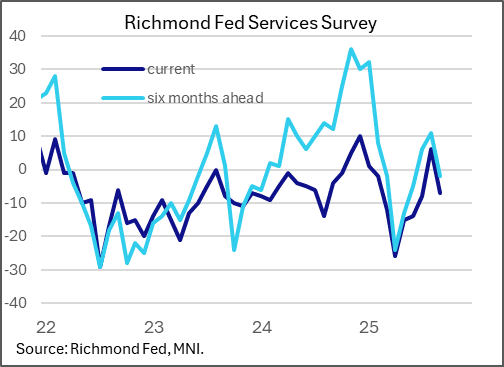

US DATA: Richmond Fed: Pickup In Activity Fails To Persist In September (1/2)

The Richmond Fed's Fifth District surveys of regional manufacturing and services firms for September showed that a nascent pickup in activity in August may have been an outlier. The headline aggregate indices as well as key sub-components weakened, though were roughly in line with averages seen over the last year.

- The manufacturing survey showed a sharp retrenchment to -17 in September from -7 prior, for the 2nd weakest headline figure since September 2024 and a full reversion of the surprise improvement in August. This was far worse than the expected improvement to -5 (Bloomberg consensus).

- The internals of the report were weak: all three of the composite sub-indices pulled back, including shipments (−20 from −5), new orders (−15 from −6), and employment (−15 from −11). In a rare bright spot, expectations improved to -1 from -10.

- The Services business activity index reverted to -7 in September after an improvement to 6 in August. Similarly the 6-month outlook fell to a 3-month low -2 from 11 prior.

- As with manufacturing, current measures were weak (revenues down to 1 from 4, demand down to 3 from 13), though employment remained steady.

EGB OPTIONS: Schatz Call Spread Seller

DUZ5 107.00/107.30cs 1x2, sold at 4 and 3.75 in 5k.