EM LATAM CREDIT: Codelco: JV With Anglo American - Positive

(CDEL: Baa2/BBB+/BBB+)

"Codelco, Anglo American to Announce Final Deal Next Week:Tercera" - Bbg

A deal that has been in the works for over six months appears to be coming to fruition now as govt-owned Codelco will jointly develop with global miner Anglo-American two copper mines near Santiago>

This is one of a number of joint ventures Codelco is establishing with the goal of boosting production with less investment.

Codelco is also seeking to join SQM in developing Lithium reserves in Chile.

CDEL 36s were last quoted T+148bp, 12bp tighter since June 30th and 14bp tighter YTD.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR OPTIONS: SFRU5 Put Buyer

SFRU5 95.8125 put, bought for 3.75 in 12.5k

SOFR OPTIONS: Outright Put buyer

SFRU5 95.8125p, bought for 3.75 in 12.5k

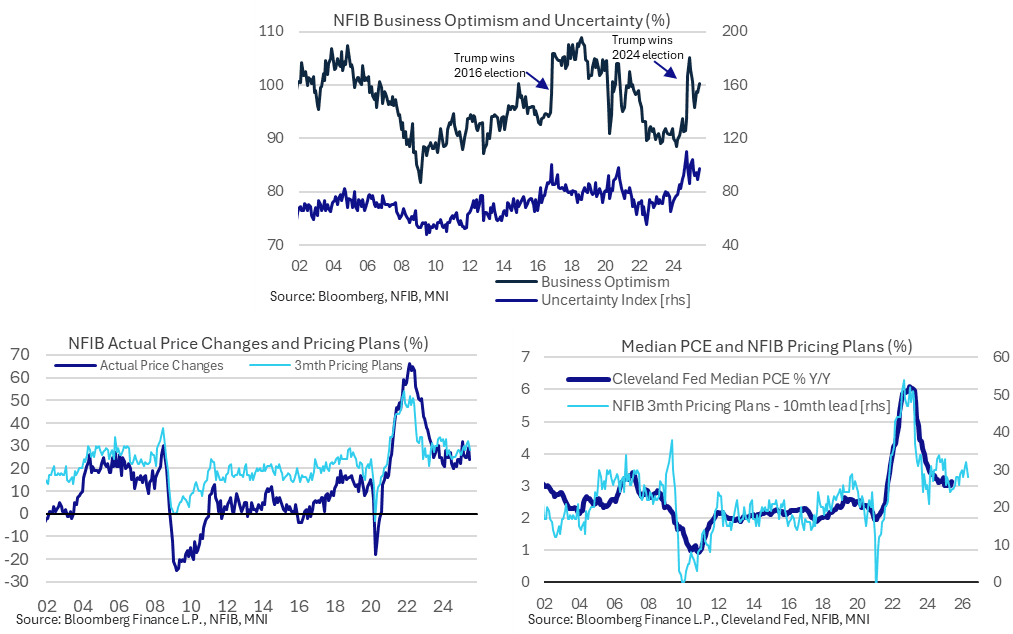

US DATA: NFIB Small Business Price Plans Cool

The NFIB small business index was stronger than expected in July despite weakness in the already published jobs details. Notably despite this slightly firmer backdrop, price plans cooled rather than accelerating further.

- The NFIB small business index was higher than expected in July as it increased to 100.3 (cons 98.9) after 98.6 in June for a five-month high.

- The 100.3 compares with the April low of 95.8 on the announcement of reciprocal tariffs, a high of 105.1 in December fully reflecting US election results and an average of 93 in 2024. The series has a very long-term 52-year average of 98.

- Impressively, seeing as the already published jobs report had shown multiple points of weakness in July, six of the ten components for this broader index improved.

- A net 36% of owners expect better business conditions, +14pps from a month earlier and the most this year. A net 16% said now is a good time to expand their business, the largest share since January.

- Ahead of today’s US CPI report for July, price plans remain relatively elevated but contained, and with some moderation compared to May and June levels.

- Specifically, a net 24% increased prices over the past three months vs 29% in June and a recent high of 32% back in February. This is in line with the 23% average seen in 2024 but remains above pre-pandemic averages of ~12%.

- A net 28% expects to increase prices over the next three months vs a recent high of 32% in June. It’s in line with the 28% averaged in 2024 but remains above the 22% averaged pre-pandemic.

- As such, it’s still pointing to some stabilization in inflation at above-target rates but the pace hasn’t accelerated further as might have been seen if small firms were planning to increasingly pass on tariff cost increases.