OIL PRODUCTS: China's Rising NEVs sales Further Curb Gasoline Consumption: OilCh

Oct-17 09:51

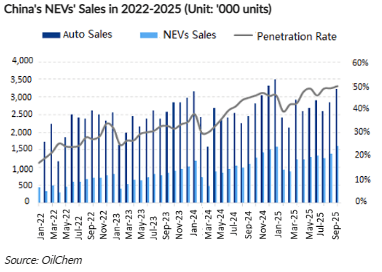

China’s new energy vehicle (NEV) sales rose in September, supported by steady overall auto demand, effective trade-in subsidies, and the upcoming end of some provincial incentives, OilChem said

- Total auto sales hit 3.226 m units in September, up 12.9% month-on-month and 14.9% year-on-year.

- NEV sales reached 1.604 m units, rising 15% month-on-month. The NEV penetration rate hit a record 53.69%, with new energy passenger vehicles reaching 56.50%.

- The growing share of NEVs has slowed fuel vehicle growth and reduced gasoline demand.

- Around 5m mt of cumulative gasoline consumption has been displaced by NEVs across Jan-Sep.

- Gasoline consumption continued to decline, down 4.06% year-on-year in September to 1.280m mt, marking 19 consecutive months of negative growth.

- Despite higher travel activity, the substitution effect of NEVs has weakened seasonal gasoline peaks.

- In Q4, auto sales are expected to rise slightly, while gasoline demand may fall 4.38% year-on-year to 13.10m mt in October.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SOFR: SFRZ5 Lifted

Sep-17 09:50

SFRZ5 paper paid 96.360 on ~5.5K, taken bid over.

FED FUNDS FUTURES: Ongoing Buying In FFV5

Sep-17 09:49

FFV5 sees another 5K lots trade at 95.945, once again bought (~30K trades there all day, price remains offered).

- Follows Monday’s 84K block buyer at the same price (which generated subsequent screen flow of ~50K lots).

- EFFR currently at 4.33%, adjusted for a 25bp cut at today's Fed decision would be 4.08%.

- Implied rate on the trades flagged above is 4.055%.

EGBS: Bund Futures Biased Higher; OAT/Bund Widens On Faure Comments

Sep-17 09:47

Bund futures are +20 ticks at 128.91, finding light support from a pullback in brent crude futures and a move away from session highs for major equity futures. An FT story suggesting China has told its tech companies to stop buying NVIDIA AI chips has weakened equities this morning.

- Trading ranges have been fairly contained with today’s risk events still ahead: The BOC decision is due at 1445BST before the more widely anticipated Fed later this evening (1900BST).

- The recovery in Bund futures from yesterday’s low underscores the corrective nature of last Friday’s pullback. Initial resistance is seen at 129.09. which shields key resistance of 129.50 (Aug 5 high).

- German yields are flat to 2.5bps lower, with the curve lightly bull flattening. Today’s long-end Bund supply was digested smoothly.

- Italy also held a sizeable E5bln buyback today, while Greece sold E250mln of GGBs.

- 10-year EGB spreads to Bunds are biased up to 1bp wider. The OAT/Bund spread widened ~1bp after Socialist Leader Faure expressed a lack of progress in latest talks with new PM Lecornu, now at ~80.5bps.

- Eurozone final August HICP saw marginal revisions relative to the flash, while the ECB’s latest wage tracker update continued to point towards easing compensation pressures.