US FISCAL: CBO Eyes June Fiscal Surplus; Deficit Still On Track For 6.5-6.7% GDP

Jul-09 20:52

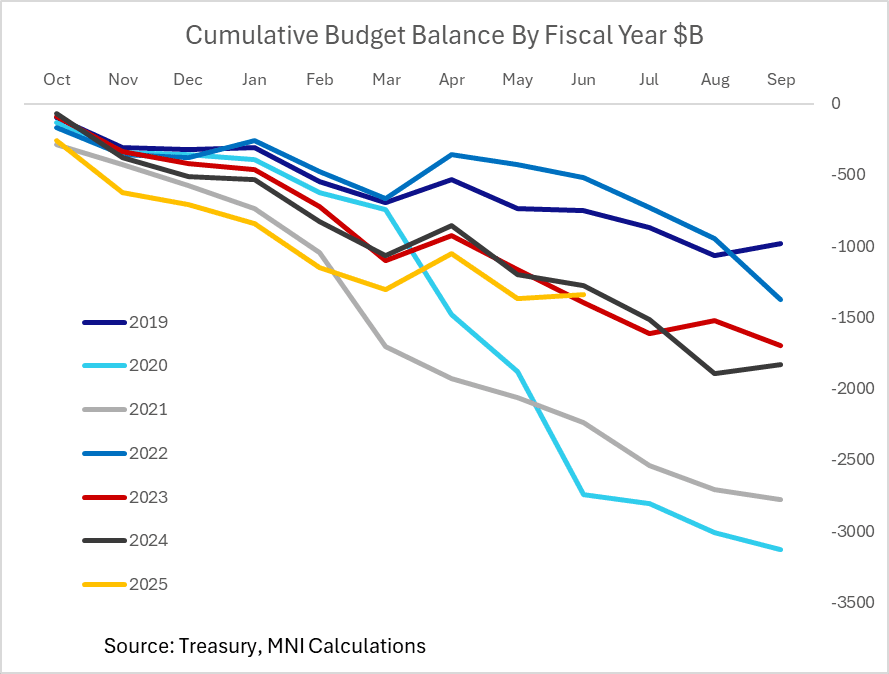

The Congressional Budget office estimates that the federal budget registered a surplus of $26B in June, vs a deficit $71B in the same month a year prior. This includes receipts of $527B and outlays of $501B.

- That's significantly different from the current Bloomberg consensus for Friday's official Treasury release which is for a deficit of $37B in June (albeit with a range of -$225B to +$69B among 13 estimates).

- However the CBO notes that if accounting for timing shifts (outlays registered on June 1 2025 moved into May), the government would have recorded a $71B deficit. Note also that this year's figures are flattered to some degree by tariffs, which raised around $28B in June, vs $7.6B a year earlier.

- In May, the CBO's estimate of the budget deficit was off by $2B ($316B vs CBO's $314B). If they're correct in this estimate, the cumulative deficit through the first 9 month of the fiscal year (Oct-Sep) will have run to just under $1.34T, vs $1.27T a year earlier, with revenues up 7% and outlays up 6% (largely due to rising mandatory spending).

- The 12-month running deficit has been narrowing very slightly as a % of GDP over recent months to 6.65% in May, and with 3 months to go in the year it looks likely to roughly meet Treasury Sec Bessent's estimated 6.5-6.7% of GDP range (was 6.4% in FY2024 and 6.2% in FY2023).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: A Warning On Core CPI Tracker Recent Accuracy

Jun-09 20:47

- Ahead of Wednesday's CPI report for May, the Cleveland Fed nowcast has headline CPI at 0.13% M/M whilst its core tracker has CPI at 0.23% M/M for a second month running (Bloomberg consensus 0.3%).

- The core tracker was very close for April as it undershot by only 1bps although the previous three months saw weaker correlation including a 20bp overshoot in March and 18bp undershoot in January.

FED: Natixis: Next Cut Pushed Back A Meeting To October

Jun-09 20:37

Natixis becomes the latest sell-side institution to push back expectations of the next Fed cut, following Friday's Employment Report. They now see easing resuming in October, vs September previously. Overall they see consecutive cuts from that point to June 2026 to 2.75-3.00% (150bp of cuts).

- "The resilience in the labor market is the primary reason for pushing out the next cut. The most recent employment report showed a labor market that is continuing to cool a bit, but with few signs of imminent cracks. This will help to confirm that the risk of continuing to wait before resuming the cutting cycle is low and pausing to observe the impact and degree of passthrough from tariffs is the appropriate path."

- Overall it appears that there will be few if any analysts who expect a cut before September, going into the June FOMC meeting next week - we will update next Monday with our overview of analyst expectations.

US OUTLOOK/OPINION: Jefferies Above Consensus On Core CPI And See Upside Risk

Jun-09 20:17

- Jefferies expect core CPI at 0.34% M/M in May for 3.0% Y/Y.

- "Core goods are expected to come in hot, up 0.6% m/m with new and used cars, up 0.6% and 2.2%, serving as the main contributors. In addition, furnishing and apparel should be firm, each up 0.25%, along with auto parts up 0.5%.”

- What's more, “[t]here is upside risk going into the print given the possibility of tariffs coming through on a broader basis.”

- “The elevated core goods figure will be offset by weak energy goods (-2.6%) due to falling gas prices. For services, car maintenance is expected to come in at 0.6% while OER will remain firm at 0.36%.”

- They see headline CPI at 0.212% M/M for 2.5% Y/Y.