US TSYS: Cash Open

TYU5 is trading 111-23+, down 0-01 from its close.

- The US 2-year yield opens around 3.75%.

- The US 10-year yield opens around 4.308%.

- (Bloomberg) - “Bloomberg Economics expects Federal Reserve Jerome Powell to unveil changes to the central bank's monetary policy framework, including axing flexible average inflation targeting (FAIT) and returning to a balanced 2% target.”

- “If the Fed re-weights its dual mandate in the revised framework, that could reset the bar for future rate cuts, and markets may be too confident about a rate cut at the September FOMC meeting.”

- Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area in 10-Year yields found solid demand overnight helped by the S&P rating, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

- Data/Events: MBA Mortgage Applications, FOMC Meeting Minutes

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Yen Selling Dominant Feature Of CFTC Update

The most notable shift in Friday's CFTC FX positioning update was JPY selling. For the week ending last Tuesday (July 15) we saw just over 35.5k in net JPY selling, see the table below. The split was roughly even between leveraged players and asset managers. For leverage players this now brings them back into an outright short. This is the first time this segment has been net short since late March of this year. Asset managers are still net long, but have cut back positioning by over 55k from the peak long position (end April). Yen sentiment has turned more bearish amid better US data outcomes, while locally political uncertainty is more elevated post the LDP coalition losing its majority. The BoJ is also seen firmly on hold in the near term.

- Elsewhere, yen selling appeared to benefit the EUR, with both leveraged players and asset managers adding to existing longs. GBP was mixed, with positive leveraged inflows, but asset managers expanded their net shorts.

- AUD and NZD positioning was little changed in aggregate. Leveraged players and asset managers are still running a net short position for the AUD.

Table 1: CFTC Positioning Update - Weekly Changes, Outright Positions By Major Currencies

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -17830 | -12606 | -17721 | 71610 |

| EUR | 13418 | 15261 | 9455 | 384260 |

| GBP | 7826 | 48469 | -12173 | -26467 |

| AUD | -987 | -20048 | -15 | -38267 |

| NZD | 1910 | -6744 | -1037 | 8192 |

| CAD | 2592 | -26393 | -7669 | -49939 |

| CHF | -1575 | -159 | 3252 | -34022 |

| MXN | 4586 | -748 | -1244 | 43075 |

Source: Bloomberg Finance L.P./CFTC/MNI

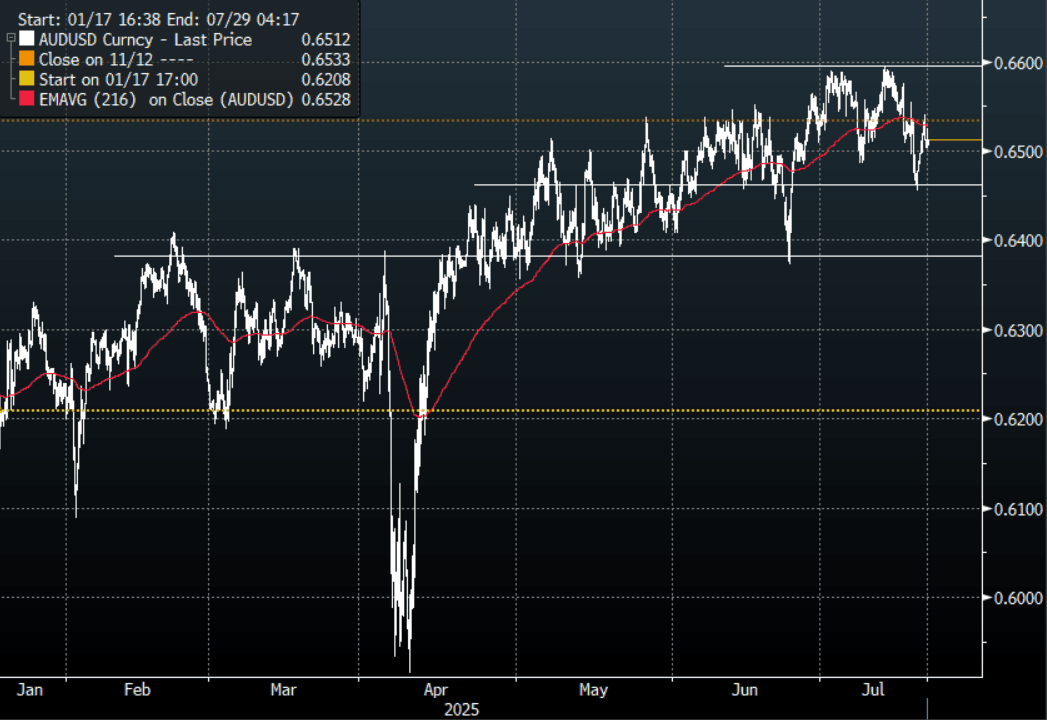

AUD: AUD/USD - Consolidating In A 0.6450 - 0.6600 Range For Now

AUD/USD - Continues To Consolidate

The AUD/USD had a range Friday night of 0.6498- 0.6541, Asia is trading around 0.6510. The pair found decent supply back towards 0.6550 again On Friday. The follow through below 0.6500 is quite disappointing for AUD shorts but with Stocks making new highs and risk outperforming, it makes it a hard environment for AUD/USD to collapse in. The Pair looks to be consolidating in a 0.6450 - 0.6600 range as we await a catalyst to provide clearer direction.

- (Bloomberg) -- “Indonesia is set to issue its first Australian dollar-denominated debt as the two countries strengthen their financial partnership.”

- “Aussie Banks' Credit, Cost Headwind to Prompt 2026 Profit Misses: Australian banks are on track for profit misses up to 15% in fiscal 2026, prompted by normalizing credit, cost-inflation and surging investment expenses that'll push up cost-to-income ratios. These factors will accentuate margin pressure from Reserve Bank of Australia rate cuts that are unlikely to offset expected strong loan growth.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD729m), 0.6500(AUD821m) . Upcoming Close Strikes : 0.6650(AUD495m July 24) - BBG

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

Fig 1: AUD/USD spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

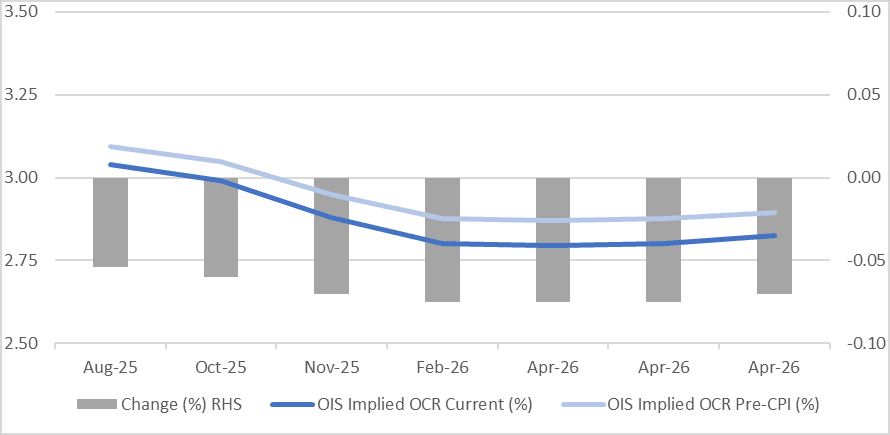

STIR: RBNZ-Dated OIS Softer After Q2 CPI Miss

RBNZ-dated OIS pricing is 5-8bps softer across meetings following today’s Q2 CPI data.

- While Q2 NZ headline CPI picked up 0.2pp to 2.7% y/y, it was less than expected and only 0.1pp above the RBNZ’s May forecast, and so well within usual errors. Thus, the RBNZ is likely to cut rates 25bp when it announces its decision on August 20.

- There was also a moderation in domestically driven non-tradeables inflation to its lowest in four years.

- 21bps of easing is priced for August, with a cumulative 37bps by November 2025 versus 16bps and 30bps before the data.

Figure 1: RBNZ Dated OIS Post-CPI vs. Pre-CPI (%)

Source: Bloomberg Finance LP / MNI