BUNDS: BTP/Bund spread falls towards

Jun-06 08:03

- Further tightening bias in the BTP/Bund, this risk has been highlighted for quite a few Week, and while the spread is only showing 0.7bp tighter for today, it now drifting towards 93.00bps.

- Noted multiple times that the initial key level is at the Psychological 90.00bps, although it did print a 90.4bps low in 2021, its lowest since Mid March 2015.

- Barclays lowered their forecast to a punchy 70bps target, while Goldman also favoured further tightening without providing a level, at least from what we have seen.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

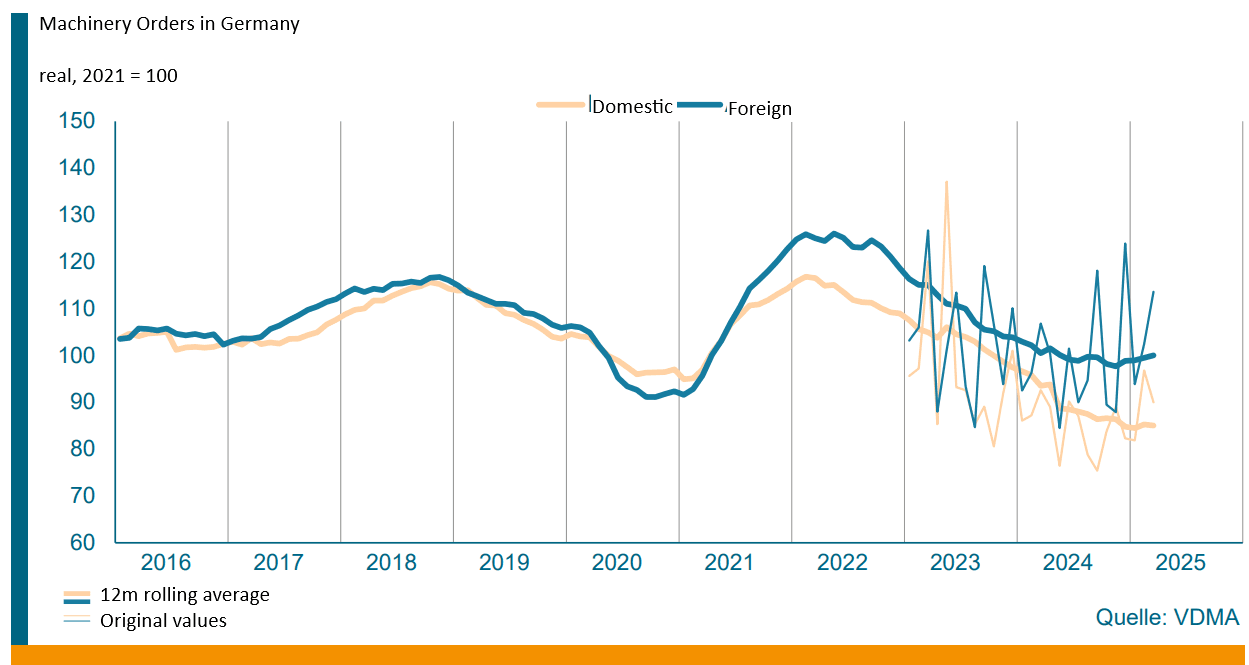

GERMAN DATA: VDMA Machinery Data Underpins Strong March Factory Orders Print

May-07 08:00

VDMA machinery orders printed +4% Y/Y in March, bringing in Q1 orders in the sector at +4% Y/Y, also. This was the first quarter since Q1'22 with an incline on the yearly rate. VDMA sees an inflection point for foreign orders but does flag uncertainty about the further trajectory there - "particularly with regard to the USA's tariff policy and possible countermeasures".

- "The weakening domestic business (minus 3 per cent) was offset by a 6 per cent increase in foreign orders", VDMA comments.

- The machinery print will have underpinned the overall factory orders print, which came in at +3.6% M/M this morning. Overall, the industrial sector in Germany appears to have seen a comparatively strong end of Q1.

EGBS: Citi Flag Global Flow Support For BTPs, Still Wary Of Widening Risk

May-07 07:49

Citi note that “the ongoing tariff de-escalation has taken our tariff hedge trade – 10yr BTP-OAT widener – to its stop this week.”

- They write “the BTP-Bund spread no longer looks rich vs European equities (though it still does vs European credit) and thus should be open to any further risk rally. However, BTP spreads are now back at pre-tariff levels with tariff risks fully priced out, and the pre-tariff hurdle at 100bp likely to come back into play”.

- Overall, they still see “risk-reward tilted towards widening. Having said this, the combination of risk factors has likely contributed to relatively flat positioning in BTPs, with potential for carry longs into summer if tariff de-escalation continues but with a relatively low bar for disappointment on that front”.

- In the meantime, they will keep an eye on “Japan flow data, for whether the new Japanese affinity to BTPs over recent months extended in March. Global portfolio flow data is already showing that 12-month rolling demand for Italian debt (not necessarily all BTPs) is now approaching that of French debt, while Spanish demand remains subdued”.

EURIBOR OPTIONS: Put spread buyer

May-07 07:44

ERK5 97.87/97.75ps, bought for 0.25 in 3k.

Trending Top

Mar-27 20:13