BTP TECHS: (U5) Range Breakout

- RES 4: 122.35 2.500 proj of the May 14 - 20 - 21 price swing

- RES 3: 122.00 Round number resistance

- RES 2: 121.73 High Jun 13 and the bull trigger

- RES 1: 120.52 50-day EMA

- PRICE: 119.40 @ Close Sep 3

- SUP 1: 119.30 Low Sep 2

- SUP 2: 118.87 Low May 21

- SUP 3: 118.51 Low May 14 and key support

- SUP 4: 118.24 1.618 proj of the Jun 13 - Jul 25 - Aug 5 price swing

The primary trend condition in BTP futures is unchanged and the direction remains up. However, for now, a bear cycle is in play. The move down this week reinforces current short-term conditions. The contract has traded through a key support at 119.59, the Jul 25 low. The clear break of this level highlights a range breakout and reinforces a bear cycle. This opens 118.87, the May 21 low. Initial firm resistance is at 120.52, the 50-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

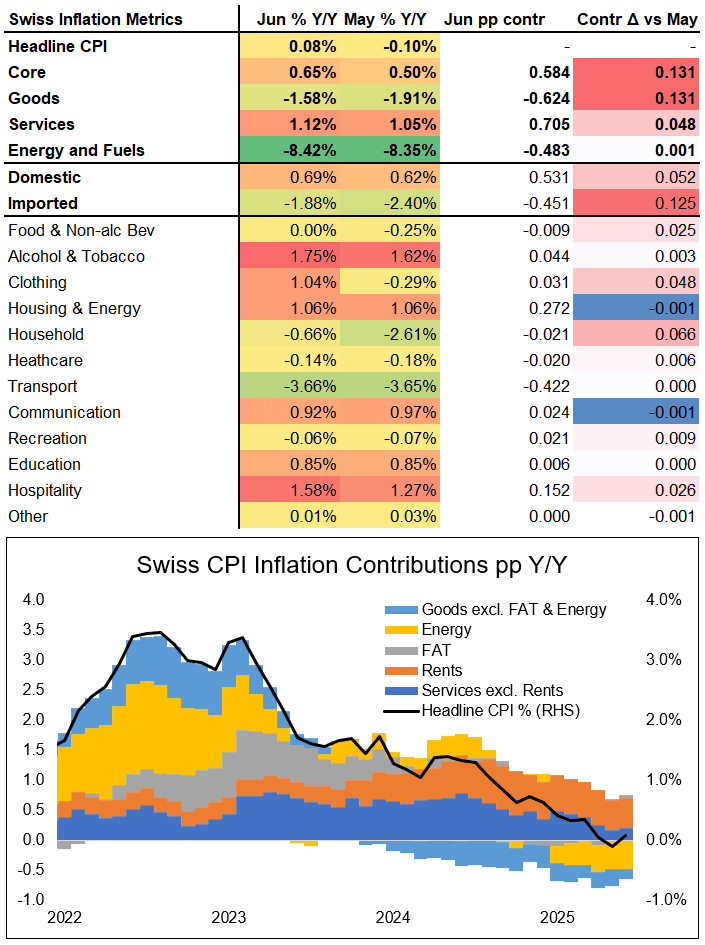

SWITZERLAND DATA: CPI Expected For Second Consecutive Print Within SNB Target

Swiss July CPI is scheduled to be published today at 0730BST/0830CEST, with consensus for an unchanged 0.1% Y/Y (-0.2% M/M).

- An inline print would mean Swiss inflation starts off Q3 in line with the SNB's latest conditional inflation forecast for this quarter, and would also represent the second consecutive month of the Y/Y measure coming in within the SNB's target range again (after having missed to the downside in May for the first time since March 2021).

- Potential continued CPI prints above 0% Y/Y would likely see markets further paring the odds of SNB easing its policy rate into negative territory against the background of Chairman Schlegel's rhetoric at the June press conference ("high bar to negative rates").

- Focus should also be on services- and domestic inflation measures, which appear to be a key input in the SNB's assessment of medium-term inflationary pressures. The measures continued to print positive throughout recent months but do both sit close to multi-year lows (at 1.12% and 0.69%, respectively, in June).

Consensus to today's print is downwardly skewed, with 6 estimates for the median 0.1% Y/Y, three analysts looking for 0.0%, and one analyst seeing -0.2%.

- UBS sees 0.1% Y/Y, commenting "we expect our definition of core inflation (headline excluding energy and food) to remain unchanged at 0.6% y/y. While energy inflation is expected to rise by 0.5pp to -7.9% y/y, its positive contribution is likely to be offset by lower food (-0.5pp to -0.5% y/y) and alcohol inflation (-0.7pp to 1.1% y/y). Overall, we think the risks to our forecast are balanced. However, as we have previously flagged, the FX pass-through from a stronger CHF so far has been surprisingly weak, implying some uncertainty for the inflation trajectory over the coming months."

US TSY FUTURES: TU/UXY Steepener Blocked

Latest block trade lodged at 06:51:06 London/01:51:06 NY:

- TUU5 4,017 lots blocked at 103-30.125

- UXYU5 1,750 lots blocked at 114-02.

- Price actions on the curve points to a TU/UXY steepener, note both legs were lodged through the offer.

- DV01 ~$150K.

EUROZONE ISSUANCE: EGB Supply (2/2)

- Spain will come to the market on Thursday to hold a Bono/Obli/ObliEi auction. On offer will be the on-the-run 3-year 2.40% May-28 Bono (ISIN: ES0000012O59), the on-the-run 10-year 3.20% Oct-35 Obli (ISIN: ES0000012P33) and the short 20-year 3.45% Jul-43 Obli (ISIN: ES0000012K95) alongside the 1.00% Nov-30 Obli-Ei (ISIN: ES00000127C8). The auction size will be confirmed this afternoon.

- As we also expected in the announcement, the auction scheduled for 21 August was cancelled (in line with precedent in recent years).

- France will conclude issuance for the week, also on Thursday by holding a LT OAT auction for E8.5-10.5bln. This is a slightly smaller auction than the E10-12bln range we have seen recently (expected, given that it is August) but what is perhaps a bit less expected is that all of the OATs on offer are off-the-run issues: the 1.25% May-34 OAT (ISIN: FR0013313582), the 1.25% May-36 OAT (ISIN: FR0013154044), the 0.50% May-40 OAT (ISIN: FR0013515806) and the 4.00% Apr-55 OAT (ISIN: FR0010171975).

NOMINAL FLOWS: This week sees E0.7bln of redemptions, of which E0.6bln is from a formerly 3-year LithGB, while coupon payments total just E0.2bln. This leaves estimated net flows for the week at positive E24.4bln, versus negative E26.2bln last week.