US: Bessent Talks On Shutdown, Fed, China & Argentina

Oct-02 11:59

Treasury Secretary Scott Bessent has been speaking to CNBC on a number of issues.

- On the gov't shutdown, Bessent says that "We could see a hit to GDP" from the shutdown. Claims that federal layoffs are just a "talking point". On Senate minority leader Chuck Schumer (D-NY) objecting to a 'clean' continuing resolution, Bessent claims that Schumer backed the spending levels in the spring, "but now has flipped", and that his "change in position reflects his polling."

- On Fed chair: Says that he is "over the halfway point in Fed job interviews", with the first round of interviews to be completed "next week". He will then present President Donald Trump with "three to five" candidates.

- On support for Argentina, Bessent says, "We are giving them a swap line. We are not putting money into Argentina". On criticism, Bessent says "America first does not mean America alone." Calls President Javier Milei's gov't a "beacon" in the region, and says Bolivia, Ecuador, and Colombia may join forces in a similar path (dependent on elections).

- On US-China talks, Bessent says the next round of talks should show a "big breakthrough". Presidents Trump and Xi are set to meet on the sidelines of the APEC summit in South Korea at the end of Oct, Bessent says it "will be very helpful for them to speak in person", and that "what gives us comfort with China is the respect the two leaders have for each other". Comes as current trade truce expires on 10 November.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

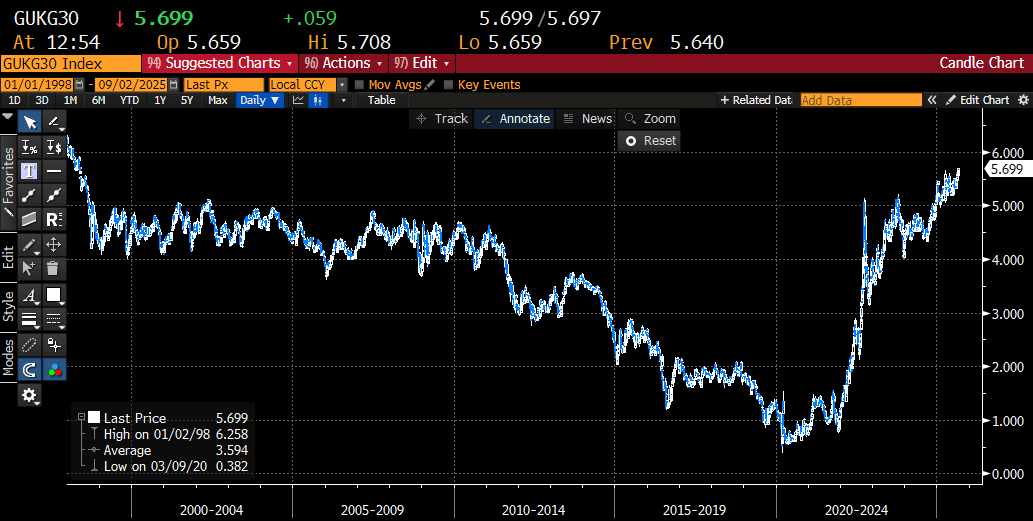

GILTS: 30-year gilt yields break to highest levels since 1998

Sep-02 11:55

- 30-year gilt yields have broken above the high of April and moved to their highest level since May 1998.

- At present the 30-year yield is up 5.7bp since yesterday's close and has also breached 5.70%. Our technical analyst notes a move to 5.74% is plausible.

- The break higher comes amid broader concern regarding UK assets with GBP FX seeing a notably selloff on the gilt open at 8:00BST this morning. The global backdrop is not favourable, of course, but with the UK fiscal position looking bleak and the date of the Autumn Budget still not yet known (and looking increasingly likely to be November or December as we noted last week). This is just adding to further uncertainty about how the UK deals with its fiscal issues with the government still pledging it will stick to its fiscal rules but also showing no appetite to break its manifesto pledges of not increasing income tax, VAT or employee national insurance (the easiest levers to increase revenues).

- However, the DMO has managed to raise a record GBP14bln in its syndicated 10-year transaction today - so there is still strong demand further down the curve if the price is right.

- Our technical analyst notes that the move higher in yields confirms a resumption of the primary uptrend now that the key resistance at 5.66%, the high print on Apr 9, has been cleared. Moving average studies are in a bull-mode position highlighting a dominant uptrend for yields. Scope is seen for a climb towards 5.74%, a 1.236 Fibonacci projection of the Jun 13 - Jul 18 - Aug 5 price swing. First key support lies at 5.55%, the 20-day EMA.

Source: MNI, Bloomberg Professional Finance LP

FOREX: NZDUSD Respects Resistance, AUDNZD Consolidating Back Above 1.11

Sep-02 11:46

- Weakness for the major equity benchmarks and the associated greenback strength has also weighed on the risk sensitive AUD and NZD on Tuesday, with weakness for the Kiwi modestly outpacing its antipodean counterpart.

- We pointed out last week that NZDUSD had extended its bounce from firm support of 0.5800 to around 2%. However, as bearish trend conditions remain overall, this might suggest that good supply would be seen into 50-day EMA resistance around 0.5930. Today’s strong move south keeps this narrative intact, and all the focus will remain on double bottom support at 0.5800, a level that has also been of pivotal significance.

- Despite some primary signs on Friday of momentum stalling above 1.1100 for AUDNZD, dips have remained shallow and well supported, with the cross back within close proximity of last week’s highs at 1.1124. The dovish RBNZ has seen AUDNZD surge higher in recent weeks, breaking back above 1.1000 convincingly, and a break of 1.1180 would place the cross at the highest level since late 2022.

- The RBNZ is likely to cut the 3% Official Cash Rate by 25bps in both October and November, but further easing into 2026 will hinge on labour market weakness and spare capacity, a former senior RBNZ economist told MNI, adding that U.S. trade policy and the Federal Reserve could feed disinflationary pressures via currency markets.

SWEDEN: Riksbank Sep Cut In The Balance Ahead Of Flash Inflation Data

Sep-02 11:42

The Riksbank September decision is priced as essentially a coin toss between a hold at 2.00% and a 25bp cut. This pricing is justified, in our view. Thursday’s August flash inflation report is the key focus for Riksbank Executive Board members and markets, and a soft print would tilt expectations in favour of a September cut despite a better set of Swedish activity signals over the past few weeks. We will send out a more comprehensive preview of the August inflation release tomorrow.

See below for a concise update on Swedish macro developments:

- Riksbank Commentary: The August Minutes portrayed a board that is willing to deliver another rate cut this year, potentially as soon as September, conditional on spot inflation rates declining back towards the previous projections.

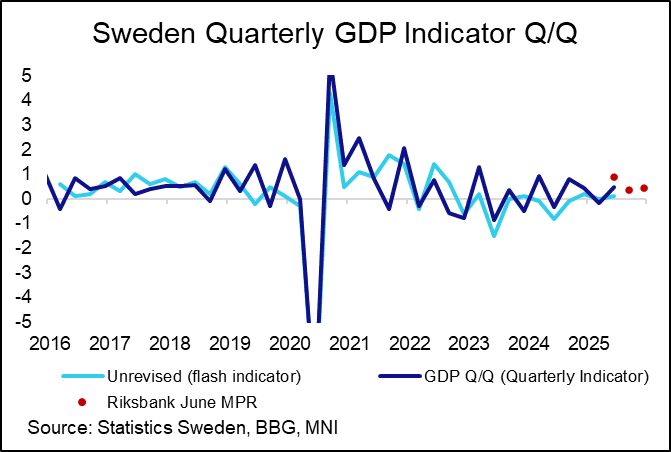

- Activity Data: Q2 GDP was upwardly revised to 0.5% Q/Q (vs 0.1% flash), but was still substantially below the Riksbank’s 0.9% projection from the June MPR. The details of the report were mixed, with positive contributions from consumption and investment, a significant positive contribution from inventories and a negative contribution from net trade. Household and business lending growth also accelerated in July.

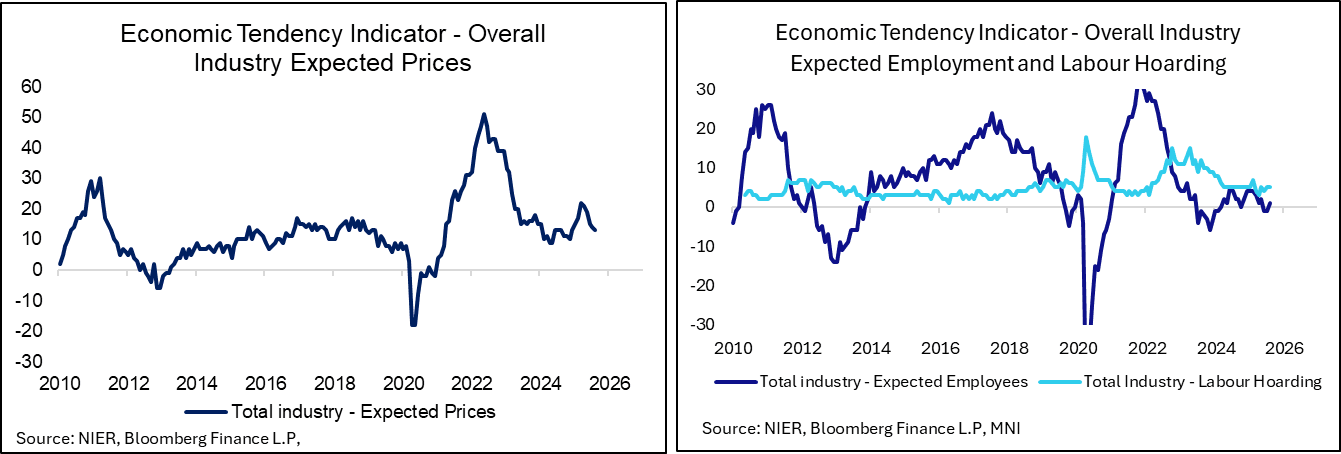

- Sentiment: The August Economic Tendency Indicator rose to a 6-month high of 96.0 (vs 94.3 prior), and the August manufacturing PMI also rose to a multi-year high of 55.3. However, more dovish signals in the Economic Tendency Survey came from another inch lower in business price plans alongside still-subdued employment expectations.

- Fiscal: Finance Minister Svantesson announced that the 2026 budget (set to be announced on Sep 22, the day prior to the Riksbank decision) will contain SEK80bln of expansionary commitments. This was well above NIER’s latest expectation of SEK34bln and also analyst estimates we had seen in recent weeks (the highest we had seen was SEK75bln from Swedbank).

- SEB have written that the proposed expansion is “unlikely to have notable impact on near-term [the] Riksbank outlook”, but “on margin reduces [the] probability of second cut this autumn”.