CNH: Back Under Key EMAs, 7.1000 Re-Test May Be Slow, Oct Trade Data Today

Nov-06 22:13

USD/CNH got close to 7.1200 in Thursday trade but couldn't test lower, we track just above this level in early Friday dealings. USD/CNH is back under all key EMAs, albeit just, with the 20-day near 7.1240. Downside focus is likely to rest on a re-test sub 7.1000, but it is likely to be a steady grind rather than dramatic fall.

- CNH was up close to 0.15% for Thursday's session, lagging broader USD index losses, DXY down 0.50%, BBDXY off 0.30%. Spot USD/CNY did finish up sub 7.1200, while the CNY CFETS basket tracker was close to unchanged near 98.00. Further USD downside may see the basket slip as crosses like CNH/JPY retrace lower.

- The broader macro backdrop favoured safe havens like yen as Thursday trade unfolded. US yields fell amid US job concerns (6-8bps lower for US Tsys), while US equities also faltered. CNH/JPY is back under 21.50, with supported eyed at 21.40, the 20-day EMA, on further downside risks. Such trends saw CNH outperform higher beta plays though, AUD/CNH got close to a 4.6000 test but tracks near 4.6145 in early Friday dealings.

- The China to world equity ratio has stabilized, but USD/CNH is fairly aligned with this ratio at this stage.

- Today on the local data front we have Oct trade figures. The y/y print is forecast at 2.9%y/y (versus 8.3% prior). The early Oct holiday period in China is seen as a headwind, while shipping data points to weaker trends as well. Imports are forecast at 2.7%y/y (prior 7.4%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer With US Tsys

Oct-07 22:12

ACGBs (YM +1.5 & XM +3.0) are stronger after US tsys finished 2-3bps richer across benchmarks.

- MNI BRIEF: Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long-term interest rates flow from success in achieving the central bank's dual mandate goals. "Most people think that achieving moderate, long-term interest rates will naturally come out of achieving maximum employment and stable prices," he said in Q&A at an event hosted by the Managed Funds Association. "I agree with that. I could imagine there being sort of tail scenarios of the world in which that's not the case. But I don't think that any of those tail scenarios are remotely describing a reality that I see now, or that I would expect to see."

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +24bps.

- The bills strip is +1 to +2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 40% probability, with a cumulative 14bps of easing priced by year-end.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond today.

- Today, the local calendar will also see Foreign Reserves data.

US TSYS: US Yields Turn Lower

Oct-07 22:04

TYZ5 reopens at 112-21, down 0-00+ from closing levels in today’s Asia-Pac session.

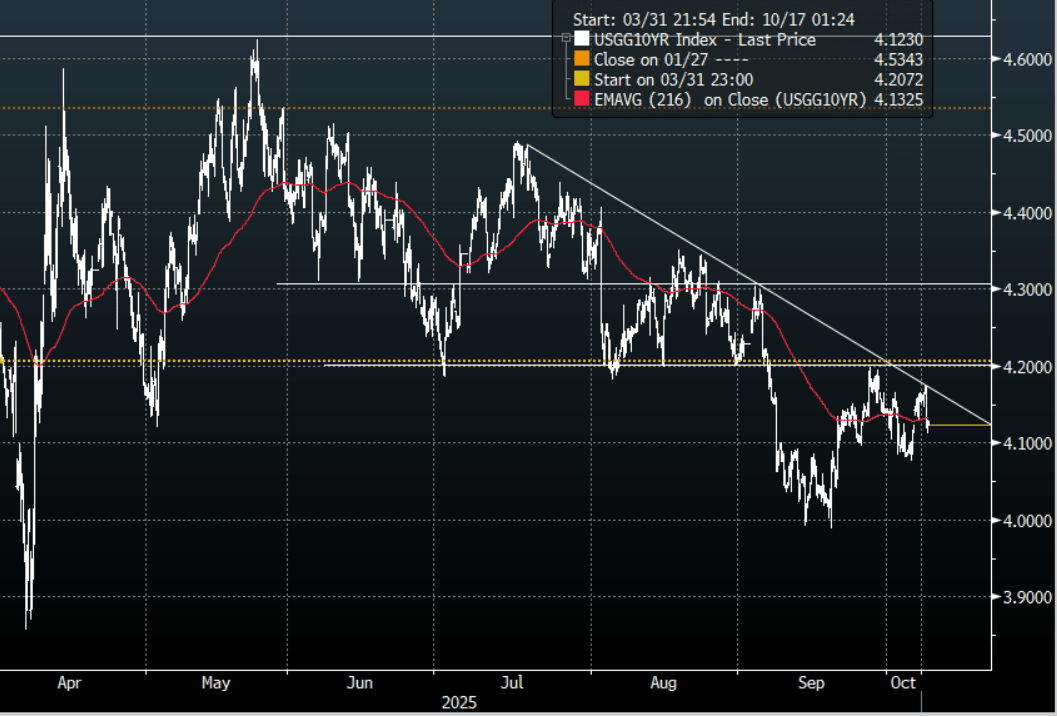

- Overnight the US 10-year yield had a range of 4.1114% - 4.1753%, closing around 4.127%.

- Treasury yields moved broadly lower overnight; (2s10s -0.63 at 55.730, 5s30s +0.85 at 102.031).

- 10-Year yields bounced to start the week on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around the 4.20% area initially and look to fade any move higher for now.

- MNI BRIEF: Third Mandate Flows From Dual Mandate Success-Miran. Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long term interest rates flow from success in achieving the central bank's dual mandate goals. "Most people think that achieving moderate, long term interest rates will naturally come out of achieving maximum employment and stable prices," he said in Q&A at an event hosted by the Managed Funds Association. "I agree with that. I could imagine there being sort of tail scenarios of the world in which that's not the case. But I don't think that any of those tail scenarios are remotely describing a reality that I see now, or that I would expect to see."

- MNI US DATA: Consumer Inflation Expectations Firm Mildly In September - NY Fed. The NY Fed consumer survey saw inflation expectations on balance increase in September. 1Y and 3Y expectations remain comfortably rangebound whilst the 5Y approach is at the high end of its short historical range.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Little Changed Ahead Of RBNZ Policy Decision, Market On 25BP/50BP

Oct-07 21:59

In local morning trade, NZGBs are little changed despite US tsys finishing with a solid gain.

- US government shutdown extended into a 7th day, and a lack of breakthrough by the end of this week will begin to prompt furloughed workers to miss pay checks, adding pressure to lawmakers to come to a resolution.

- NZ's fortnightly dairy price auction, via GDT saw a further correction lower overnight. The whole milk powder price fell 2.3% and is now back to levels from Q4 2024.

- After Q2 GDP fell 0.9% q/q, more than the RBNZ's -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- Two MPC members voted for a 50bp rate cut at the last meeting, but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed slightly softer across meetings. 36bps of easing is priced for tomorrow, with a cumulative 63bps by November 2025.

- Swap rates are slightly mixed.

- RBNZ dated OIS pricing is little changed across meetings. 35bps of easing is priced for today, with a cumulative 62bps by November 2025.