INDIA: August CPI Preview

Sep-11 23:18

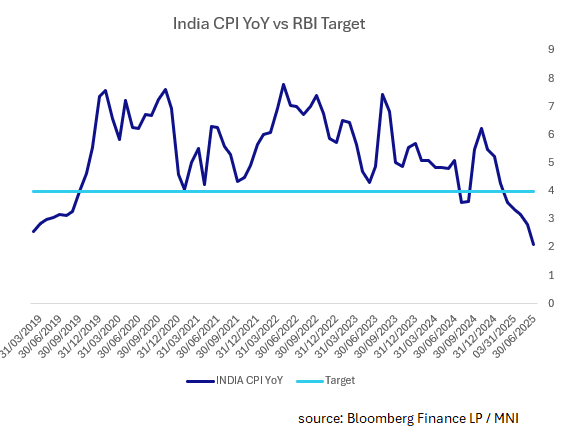

- India's August Year on Year CPI is forecast to tick higher, whilst remaining below the RBI target of 4%. The Reserve Bank of India (RBI)'s formal inflation target is 4%, with a tolerance band of 2% to 6%. As of September, this framework remains in place with the RBI working to keep headline inflation around the 4% midpoint while ensuring price stability and supporting growth in the Indian economy.

- RBI Governor Sanjay Malhotra said, “CPI inflation for the current year 2025-26 is now projected at 3.1%. This is down from 3.7% that we had earlier projected in June

- In July, CPI hit the lowest since 2017 at 1.55% and is forecast to move higher to +2.11% in the August release.

- The data is due out later today.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Weaker Overnight After US CPI Data, PPI & 5Y Supply Due

Aug-12 23:16

In post-Tokyo trade, JGB futures closed weaker, -18 compared to settlement levels, after US tsys finished with a twist steepening on Tuesday.

- The focus was on the July CPI for insight on the FOMC's policy path. That the data failed to surprise on the hotter side of expectations opened the door a little wider for a September rate cut.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- That provided a strong underpinning for Wall Street which climbed to record highs.

- (Bloomberg) -- "Japan's current benchmark 10-year government bond wasn't traded at all on Tuesday, the first such instance in more than two years, according to data from an institutional brokerage."

- Today, the local calendar will see PPI and Machine Orders data alongside 5-year supply.

AUSSIE BONDS: Twist Steepener With US Tsys, Q2 Wages Due

Aug-12 23:08

ACGBs (YM +1.5 & XM -1.0) are slightly mixed after US tsys finished with a twist steepening on Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025 (up from 57bp Monday).

- Cash ACGBs are 2bps richer to 1bp cheaper with the AU-US 10-year yield differential at -4bps.

- The bills strip is flat to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 37% probability, with a cumulative 52bps of easing priced by year-end.

- Today, the local calendar will see the Q2 Wage Price Index.

- The AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond today and A$1000mn of the 2.75% 2 1 November 2029 bond on Friday.

BONDS: NZGBS: Little Changed, US Tsys Twist Steepen After CPI

Aug-12 22:56

In local morning trade, NZGBs are unchanged after US tsys finished with a twist steepening on Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer.

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025.

- With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3.

- NZ retail card spending rose 0.2% m/m in July.

- On Friday, the July BNZ manufacturing PMI Index and July monthly price series are released including food, travel, electricity and rents.

- Swap rates are little changed.

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for August, with a cumulative 41bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.