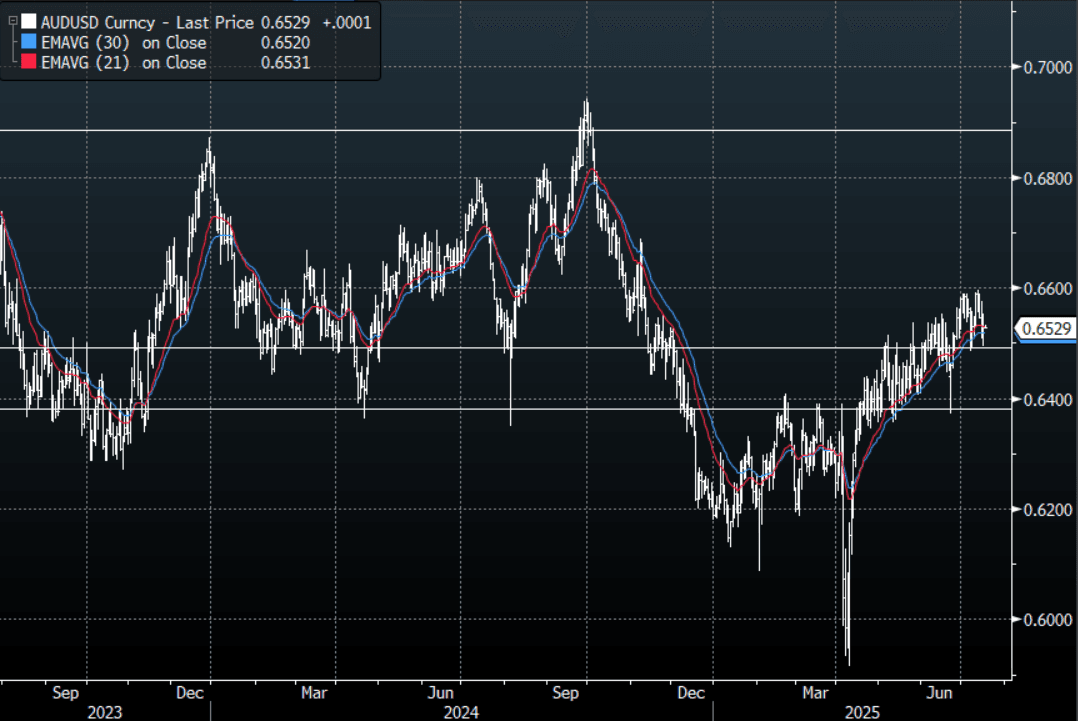

AUD: AUD/USD - Settles Just Above its 0.6500 Support After Overnight Volatility

The AUD/USD had a range overnight of 0.6495- 0.6554, Asia is trading around 0.6530. The USD had a bit of a roller coaster of a ride yesterday as rumours of a potential Powell sacking gained traction, this was later denied by Trump, though he also left the door open to Powell being dismissed for fraud. The price action was very clear though, if Powell is removed the USD will be swiftly sold. The AUD/USD found decent demand sub 0.6500 initially, a sustained break through this level is needed to open up the potential for a further pullback towards the 0.6350 area. The fortunes of the USD will obviously have a clear say in the direction this takes.

- (Bloomberg) -- “President Trump said: “I don’t rule out anything, but I think it’s highly unlikely, unless he has to leave for fraud.” A White House official, speaking on the condition of anonymity earlier Wednesday, said they expected Trump to soon move against the Fed chief. Some lawmakers also left that Tuesday evening meeting with that impression, and Trump acknowledged that he had polled the participants about dismissing Powell.”

- “Trump is softening his tone with China in hopes of securing a summit with Xi Jinping and a trade deal, people familiar said..” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6540(AUD556m), 0.6500(AUD473m). Upcoming Close Strikes : 0.6480(AUD886m July18), 0.6500(AUD739m July 21), 0.6600(AUD725m July 21)

- CFTC Data shows Asset managers added to their shorts slightly -38252, the Leveraged community pared back their shorts to -19061.

- Data/Event: Consumer Inflation Expectation, Unemployment Rate

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA DATA: Goldman's Sees Upside Risks To H1 GDP Forecast

The global bank sees upside risks to its H1 China GDP forecast post yesterday's May data outcomes, but cautions on the sustainability of stronger retail spending. It also sees further policy support is likely needed in H2. See below for more details.

Goldman Sachs: "Retail sales growth rose meaningfully in May, with year-on-year growth in home appliance and communication equipment sales value jumping to 53% and 33%, respectively from 39% and 20% in April, as an earlier-than-usual "618" online shopping festival this year has pulled forward some demand from June to May. However, we caution that such an improvement may not be sustainable in June due to payback effects and funding shortages of consumer goods trade-in program in some regions. In our view, China's May activity data highlighted the importance of government policy for domestic demand (e.g., consumer goods trade-in program), continued deflationary pressures (e.g., strong real auto production and weak nominal auto sales), and a prolonged property downturn. Incorporating April-May activity data, we see a slight upside risk to our Q2 real GDP growth forecast of 5.0% yoy. Given the persistent property weakness, increased labor market stress and the unsustainability of both consumer goods trade-in program and export frontloading, we believe additional policy easing is still necessary in H2, though the urgency for significant stimulus in the near term appears lower thanks to the better-than-feared macro data so far."

AUSSIE 10-YEAR TECHS: (M5) Bear Cycle Remains Intact For Now

- RES 3: 96.501 - 76.4% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 2: 96.207 - 61.8% of the Mar 14 - Nov 1 ‘23 bear leg

- RES 1: 95.960 - High Apr 7

- PRICE: 95.750 @ 17:12 BST Jun 16

- SUP 1: 95.415/95.300 - Low May 15 / Low Jan 14

- SUP 2: 95.275 - Low Nov 14 (cont) and a key support

- SUP 3: 94.707 - 1.0% 10-dma envelope

Aussie 10-yr futures rallied well on the RBA rate decision, reversing a small part of recent weakness. Recent price action pressured prices through to new pullback lows last week. Next support undercuts at 95.420 (pierced), the Feb 13 low, ahead of 95.275, the Nov 14 low and a key support. Clearance of this level would strengthen a bearish condition. To the upside, a recovery of recent losses would shift attention to resistance at 96.207, a Fibonacci retracement point.

US TSYS: Long-End Leads Yields Higher

TYU5 reopens at 110-16, up 0-00+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.3987% - 4.4581%, closing around 4.446%.

- Treasury yields ended higher on the night, led by the long-end helping the yield curve steepen (2s10s +2.65 at 47.559, 5s30s +2.99 at 92.046).

- MNI US DATA: Poor Activity, But Much-Improved Outlook In Empire Manufacturing Survey. The NY Fed's Empire Manufacturing survey unexpectedly saw the headline General Business Conditions index worsen in June, to a 3-month low -16.0 (-6.0 expected) vs -9.2 in April. This was a surprise as the Empire survey is conducted early in the month, and May's deterioration (-8.1 to -9.2) had been seen as not reflective of the May 12 US-China tentative tariff deal which saw sentiment improve in other surveys conducted later in the month.

- “An Israeli official said military operations will continue against Tehran’s missile and nuclear programs regardless of any talks with the US.”(BBG)

- The 10-year yield has bounced strongly off its 4.30/35% support, this area needs to hold if yields are to move higher. The range looks to be 4.30% - 4.60% for now a break either side would provide a clearer direction. It seems traders for the moment are more concerned with the move in oil and the implications it has for inflation and the FOMC this week than buying treasuries as a safe haven.