USDCAD TECHS: Trades Through The 50-Day EMA

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6603 High Nov 11 ‘24

- RES 1: 0.6595 High Jul 11 and the bull trigger

- PRICE: 0.6483 @ 16:34 BST Jul 17

- SUP 1: 0.6455 Low Jul 17

- SUP 2: 0.6435 23.6% retracement of the Sep 9 - Jul 11 bull leg

- SUP 3: 0.6373 Low Jun 23 and a bear trigger

- SUP 4: 0.6357 Low May 12

The trend set-up in AUDUSD remains bullish, however, a corrective cycle remains in play for now. Spot sold off on softer jobs numbers, taking out important support at 0.6490, the 50-day EMA. A clear break of this EMA would highlight a stronger reversal and signal scope for an extension initially towards 0.6435, a Fibonacci retracement. Key short-term resistance has been defined at 0.6595, a break of it would resume the uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

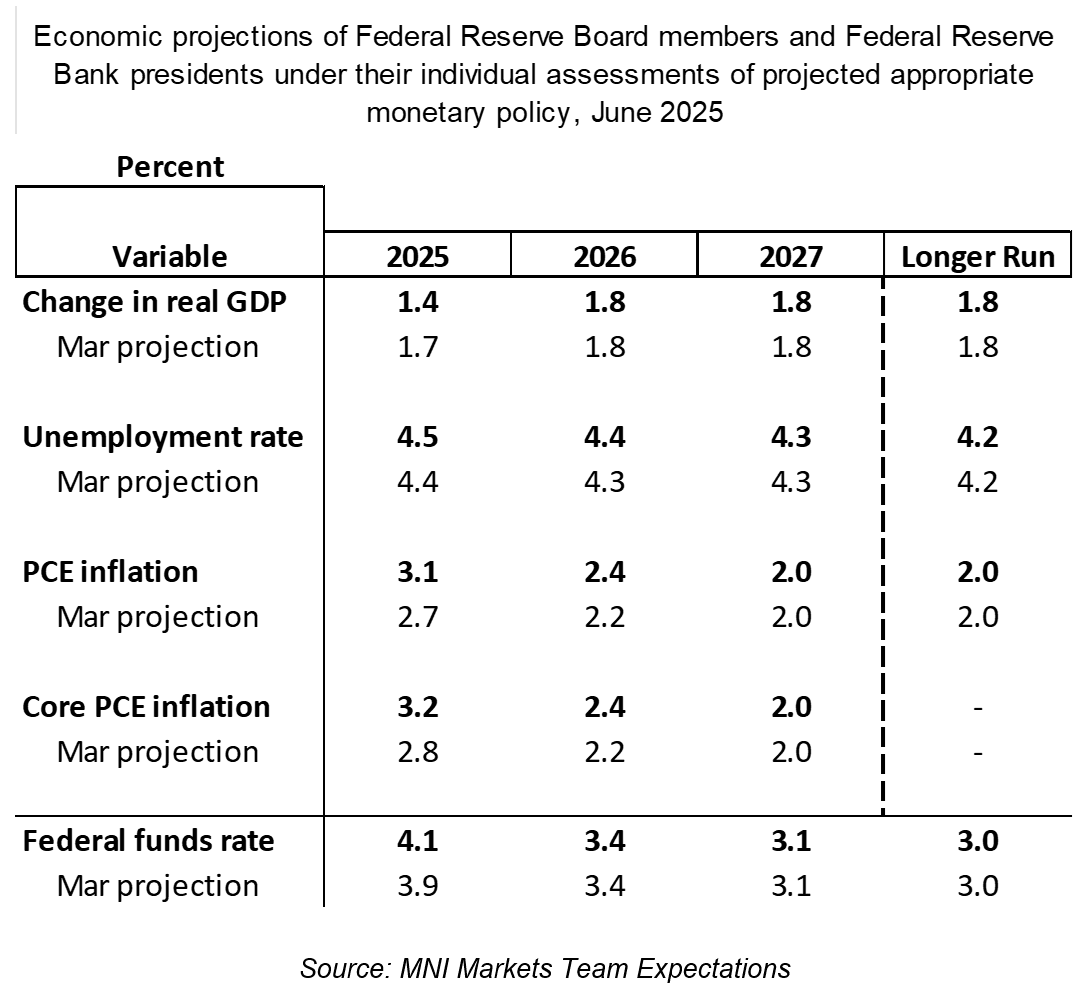

FED: Summary Of Economic Projections: Weaker Growth, Higher Inflation (2/4)

The MNI Markets Team’s expectations for the updated Economic Projections are below.

- As of the May meeting, the Federal Reserve staff – whose outlook tends to be broadly shared by the median Committee member – revised their forecasts for growth weaker in 2025 and 2026, “as announced trade policies implied a larger drag on real activity relative to the policies that the staff had assumed in their previous forecast. Trade policies were also expected to lead to slower productivity growth and therefore to reduce potential GDP growth over the next few years. With the drag on demand expected to start earlier and to be larger than the supply response, the output gap was projected to widen significantly over the forecast period. The labor market was expected to weaken substantially, with the unemployment rate forecast moving above the staff's estimate of its natural rate by the end of this year and remaining above the natural rate through 2027."

- On inflation, "The staff's inflation projection was higher than the one prepared for the March meeting. Tariffs were expected to boost inflation markedly this year and to provide a smaller boost in 2026; after that, inflation was projected to decline to 2 percent by 2027."

- Our expectations for these changes fall somewhere in between those projections and the March SEP – a slightly higher unemployment rate, substantially higher inflation in 2025 but to a lesser extent in 2026, and weaker GDP growth this year. Longer-run variables should be unchanged.

FED: FOMC Meeting Expectations: Patience Mostly Seen In New Projections (1/4)

We expect that the June meeting communications will reflect an increasingly patient attitude since May and certainly since March’s projections. Our full meeting preview, including analyst expectations, is Here.

- With the Statement in need of only mark-to-market edits, and Chair Powell’s commentary unlikely to be much different from May’s press conference, this patience will be mostly reflected in the new SEP.

- There is a fairly low bar to the 2025 rate median to shift up to show 1 cut instead of March’ 2, and that seems like the most likely outcome.

- Overall despite its patience, the FOMC’s easing bias remains, perhaps aided to some extent by recent inflation data coming in softer than feared. This will be reflected in the 2026-27 dots which will show that the destination remains more or less the same, just with a delay.

- This may mean an awkward message alongside the new economic forecasts, which are likely to show a significant upward revision in near-term inflation which doesn’t quite subside to target by end-2026, alongside an unemployment rate that doesn’t rise significantly.

- Squaring the circle there is the likelihood that participants’ risk assessments for growth and inflation will remain elevated and could even increase further from March’s extremes.

- Put another way, the situation is fluid. In the meantime, the FOMC sees policy as being in a position to react according to developing circumstances.

US TSYS: Late SOFR/Treasury Option Roundup: Leaning Bullish

SOFR & Treasury option flow leans bullish Tuesday as Middle East tensions spurred risk-off support in rates. Breadth of moves rather modest as markets also await Wednesday's FOMC policy annc. Despite the rally, curves bull flattened while projected rate cut pricing retreated from morning's levels (*) as follows: Jun'25 at 0.0bp, Jul'25 steady at -3.6bp, Sep'25 at -17.7bp (-19.5bp), Oct'25 at -29.6bp (-32.6bp), Dec'25 at -45.2bp (-48.8bp).

- SOFR Options

- -10,000 SFRZ5 95.56/95.68/95.81 put trees, 2.125

- +5,000 SFRZ5 96.25/96.50/96.75 call flys, 2.0 ref 96.11

- -15,000 SFRU5 95.75/95.87 2x1 put spds 2.0 over SFRZ5 95.62/95.75 2x1 put spds

- +10,000 0QZ5 96.75/97.00/97.50/97.75 call condors, 6.0 ref 96.695

- Block: -9,000 SFRZ5 97.00/97.25/97.75/98.00 call condors, 0.75 ref 96.09.5

- -10,000 0QZ5 97.50/97.62 call spds, 1.75 vs. 96.73/0.05%

- +2,500 SFRZ5 96.37/96.75 call spds vs. 0QZ5 97.25/97.50 call spd, 1.5 net/steepener

- +2,500 SFRN5 95.37/95.68 put spds, .37

- -4,000 SFRU5 95.68/95.81/96.25/96.37 call condors, 5.25 ref 95.875

- 2,000 0QU5 96.75/97.00/97.25 call flys ref 96.68 to -.675

- 3,000 SFRN5 96.00/96.12/96.75 broken call trees ref 95.885

- +13,500 SFRQ5 95.62/95.75 put spds 2.5

- 2,000 SFRZ5 96.37/96.75 call spds vs. 0QZ5 97.25/97.50 call spds

- +1,250 SFRZ5 96.25/96.37/96.62/96.75 call condors, 1.75 ref 96.13

- +2,000 0QZ5 97.00/97.31 call spds, 8

- Treasury Options

- -5,250 TYN5/TYQ5 111.5 put spds, 35 (Aug over) ref 110-28

- 8,000 TYN5 110.75/111 call spds, 6 ref 110-25

- 10,000 TUQ5/TUU5 104 call spds, 4.5 ref 103-20.25

- 3,500 TYN5 111/111.5 call spds ref 110-25

- 5,000 wk4 TY 110.75 straddles, 56 ref 110-25.5 (exp 6/27)

- 3,000 TUN5/TUQ5 103.75 call spds 8 ref 103-20.88

- 2,000 TYN5 110.5 straddles, 38.0

- +2,000 FVN5 108.5 calls, 5 vs 108-03/0.24%

- +5,000 TUQ5 103/104.125 call over risk reversals, 4 ref 103-20

- +3,000 FVQ5 107.25/109 call over risk reversal, 1 ref 108-01.5

- +2,500 TYU5 111.5 calls, 54 vs. 110-22/0.22%

- +3,000 Wed wkly 111/111.25 call spds, 3 ref 110-18.5 (exp tomorrow)

- +2,000 FVN5 108.25 calls, 7 vs. 107-31.25/0.30%