EURJPY TECHS: Trend Needle Points North

- RES 4: 175.43 High Jul 11 ‘24 and a key medium-term resistance

- RES 3: 174.86 1.764 proj of the Feb 28 - Mar 18 - Apr 7 price swing

- RES 2: 173.43 High Jul 12 ‘24

- RES 1: 173.24 High Jul 15

- PRICE: 172.18 @ 16:32 BST Jul 17

- SUP 1: 171.60 Low Jul 14

- SUP 2: 170.22 20-day EMA

- SUP 3: 169.32 Low Jul 3

- SUP 4: 167.50 50-day EMA

A bull phase in EURJPY remains in play and fresh cycle highs this week reinforce current conditions. The move higher also maintains the price sequence of higher highs and higher lows and note that MA studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 173.43, the Jul 12 ‘24 high. Support to watch lies at 170.22, the 20-day EMA.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Weak Restaurants Drive Pullback In PCE Estimates

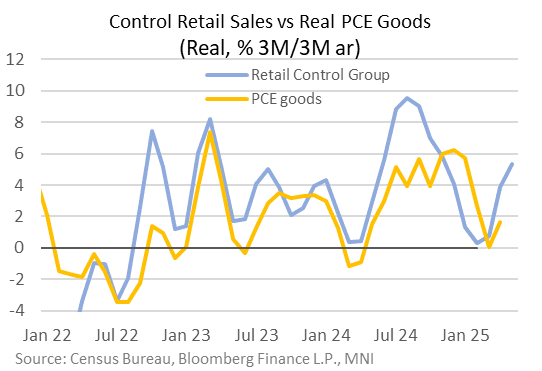

May's sequential retail sales decline sees nominal sales down for a 2nd consecutive month, but the Control Group was actually quite solid, beating expectations at 0.4% M/M and suggesting that the GDP impact of the report may be relatively limited.

- We note that today, the Atlanta Fed substantially lowered its estimate for Q2 real personal consumption expenditure (PCE) growth, to 1.9% Q/Q SAAR from 2.5% prior to this release. However real goods consumption was seen holding up relatively well, at 2.9% (a slight downgrade from 3.0% in the prior estimate).

- That's in line with what appears to be a modest pickup of Control Group momentum in May - the grouping being helped by excluding auto and gasoline among other categories which were weak (in nominal terms at least) in the month. It appears to be running at around 4.1% 3M/3M annualized, though a little stronger than that on a real basis due to recent soft non-vehicle core goods price inflation.

- In fact, the Atlanta Fed's downgrade to Q2 PCE was due almost entirely to PCE services: they slashed their growth forecast to 1.5% for the quarter from 2.2% prior. PCE goods had been seen contributing 0.6pp to GDP in the quarter, and that hasn't changed; PCE Services' expected contribution has dropped from 1.1pp to 0.7pp.

- This in turn looks driven by food services and drinking places - the only services category in retail sales - whose fall of 0.9% (biggest drop in 27 months) in May's retail sales report was a bit of a shock after strength in the prior two months (though Atlanta Fed GDPNow overall sees real PCE services ex-food services slowing in May as well). "Food services and accommodations" is over 10% of PCE services spending.

- However the strong March/April restaurant retail sales (2.5%, 0.8%) have the series running at a solid 10.6% quarterly pace of growth in May, so a major pullback in Q2 is hardly assured, at least by our calculations.

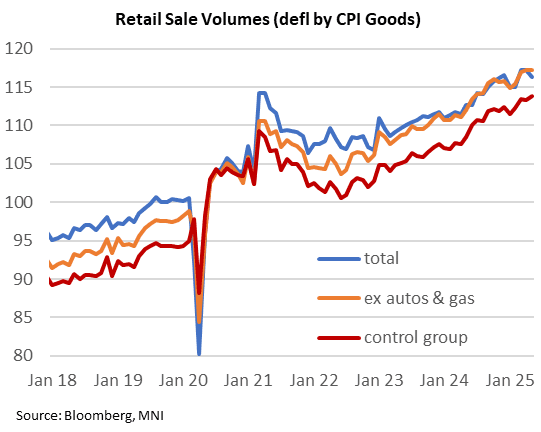

- Overall, "real" (deflated by CPI goods) retail sales volumes remain in an uptrend, notably core (ex-auto/gas and Control Group). We will watch the May PCE report at end-June with great interest to see how broader consumer dynamics are faring.

US TSY OPTIONS: 10Y Put Calendar Spread

- -5,250 TYN5/TYQ5 111.5 put spds, 35 (Aug over) ref 110-28

USDJPY TECHS: Resistance Remains Intact

- RES 4: 150.49 High Apr 2

- RES 3: 149.28 High Apr 3

- RES 2: 147.67/148.65 High May 14 / 12 and a reversal trigger

- RES 1: 145.46/146.28 High Jun 11 / High May 29 and key resistance

- PRICE: 145.23 @ 15:46 BST Jun 17

- SUP 1: 142.80/12 Low Jun 11 / Low May 27 and a key support

- SUP 2: 141.96 76.4% retracement of the Apr 22 - May 12 bull leg

- SUP 3: 139.89 Low Apr 22 and a bear trigger

- SUP 4: 138.82 1.50 proj of the Feb 12 - Mar 11 - 28 price swing

USDJPY is higher, but remains inside the broad range and below last week’s high. Recent weakness suggests the correction between Jun 3 - 11, is over. The trend direction is down - moving average studies are in a clear bear-mode position, highlighting a dominant downtrend. A resumption of weakness would open 142.12, the May 27 low. Key short-term resistance is 146.28, the May 29 high. First resistance is 145.46, Jun 11 high.