FOREX: AUD/NZD Uptrend Stalls Post AU Jobs Data, Dollar Down But Up From Lows

The USD has stayed on the backfoot, albeit away from worst levels. The BBDXY is down a further 0.10% to 1209/10, fresh lows in around a week for the index. Carry over USD weakness following Powell rhetoric (labor market softening concerns) remains a theme, although the 4.00% level continues to hold for the US 10yr. The USD/CNY fix was also set lower again but USD/CNH has struggled to break lower. The AUD has been the exception to these broader softer USD trends, with a rise in the Sep unemployment rate (more than forecast) pushing us back under 0.6500 and underperforming on key crosses.

- AUD/USD got lows of 0.6480 (last near 0.6490), off 0.35%. Recent lows at 0.6440 remain intact for now. Labour market conditions eased in September. with the jobless rate now at 4.5%, fresh highs back to 2021. This makes a November rate cut more likely but given the RBA's inflation concerns, Q3 CPI on 29 October remains the key input.

- The AUD/NZD cross has tested back under 1.1300, fresh lows for Oct and sub 20-day EMA support. We get Q3 CPI for NZ next Monday. AU-NZ 2yr swap rates sit around 8bps off recent highs, last +97bps, which is not implying further sharp AUD/NZD downside.

- NZD/USD couldn't test above recent highs near 0.5760 (last 0.5740, still +0.30% higher).

- USD/JPY got to lows of 150.51, before support emerged. We were last 150.90/95 only down marginally versus end Wednesday levels. The following option expiries may be influencing spot: Y150.50($729mln), Y151.00($511mln).

- BoJ hawk Tamura reiterated his hawkish outlook, which may have benefited the yen at the margins. We do hear from the Deputy Governor tomorrow. US Tsy Bessent stated that USD/JPY will settle at the appropriate level if BoJ conducts the right policy (via BBG). FinMin Kato also noted they were seeing rapid FX moves in a weak yen direction, leaving intervention risks on the table.

- Japan core machine orders were weaker, implying some downside capex risks. It was also reported that Ishin leaders will make a decision on the coalition with the LDP. Takaichi PM odds sit near 92 per Polymarket.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Quiet Session

The TYZ5 range has been 113-11 to 113-14 during the Asia-Pacific session. It last changed hands at 113-13+, down 0-01+ from the previous close.

- The US 2-year yield has edged lower trading 3.533%.

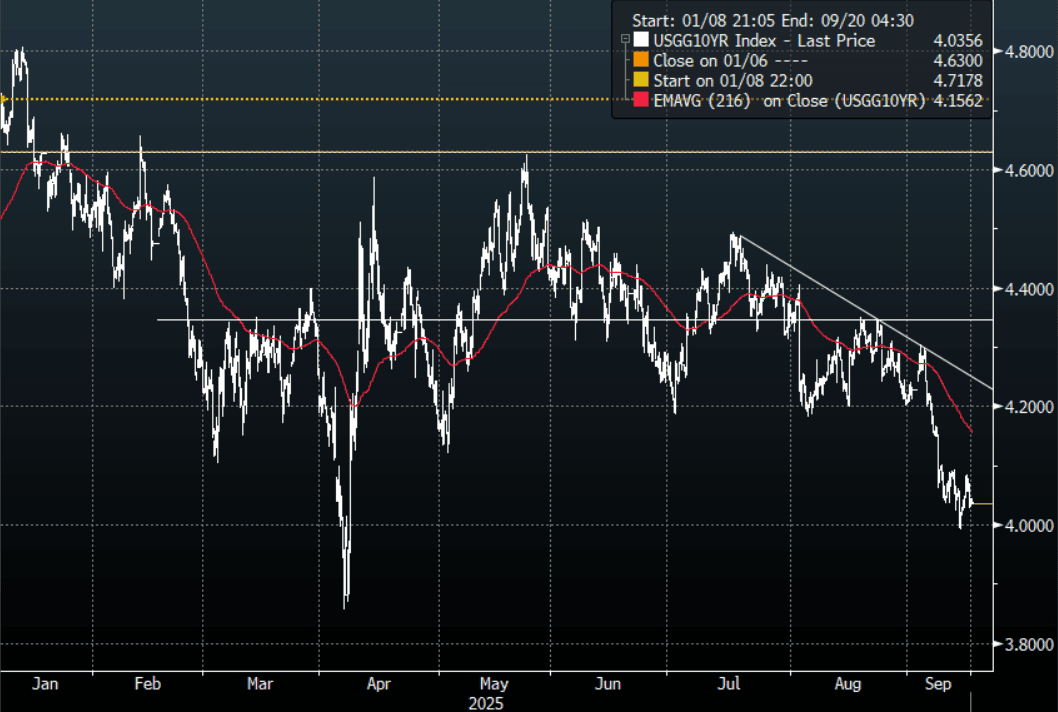

- The US 10-year yield is trading around 4.035%.

- 10-Year Yields continue to do work just above 4.00% as the market looks towards the FOMC this week. The first buy-zone is now back towards the 4.20% area where I suspect decent demand should return initially. A sustained break through 4.00% is needed for the focus to then turn towards the 3.80% area. The market does seem confident of a dovish outcome, the risk is Powell does not deliver.

- MNI BRIEF: Senate Confirms White House's Miran As Fed Governor. The Senate late Monday confirmed White House Council of Economic Advisers Chair Stephen Miran to join the Federal Reserve Board of Governors, serving the final four months of a 14-year term vacated by Adriana Kugler. The vote was 48 to 47. Miran in an unprecedented arrangement is taking an unpaid leave of absence from the White House while serving out the remainder of Kugler's term

- MNI BRIEF: Trump Cannot Fire Fed's Cook, Appeals Court Rules. President Donald Trump cannot fire Federal Reserve Governor Lisa Cook, according to the U.S. Court of Appeals for the D.C. Circuit, a ruling the Justice Department will likely appeal to the Supreme Court. The ruling means that Cook, a member of the Fed’s board of governors, can participate in the two-day FOMC meeting that begins Tuesday.

- Data/Events: Retail Sales, New York Fed Services Business Activity, Industrial Production, NAHB Housing Market Index

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: Bond Futures Lowers in Morning Trade

- China's bond futures moved lower this morning, taking back some of yesterday's gains.

- The 10-Yr is lower by -0.10 at 107.74, below the 20-day EMA of 107.89.

- The 2-Yr is lower by -0.01 at 102.35, below all major moving averages.

- The 10-Yr CGB is up at 1.80%.

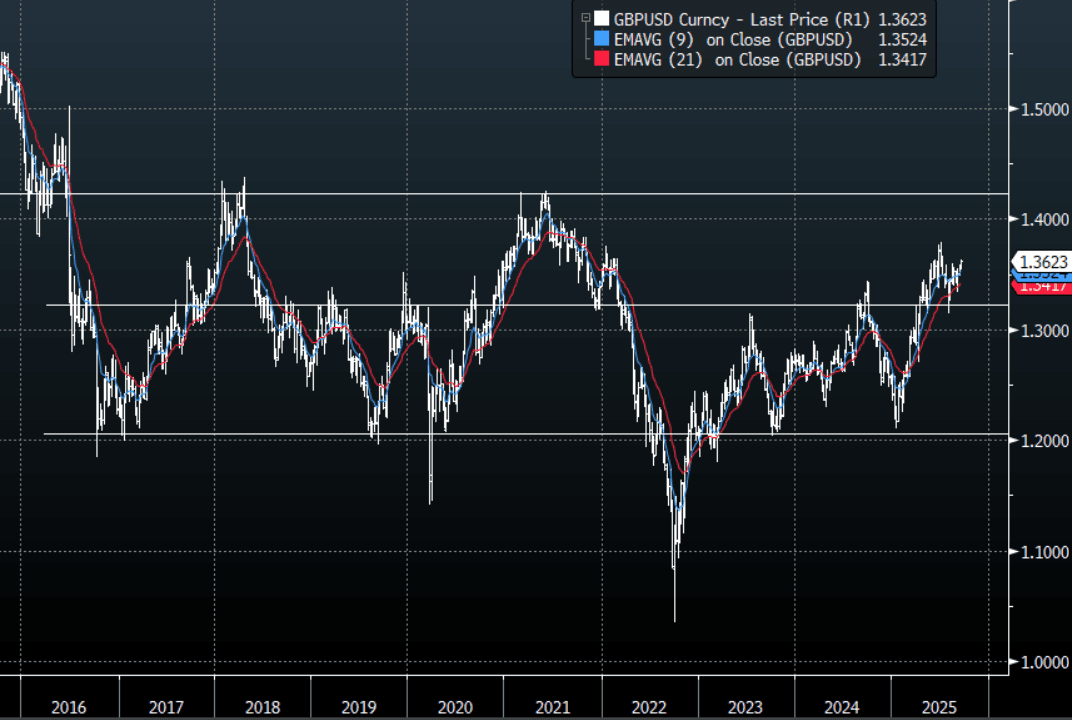

GBP: GBP/USD - Trying To Regain Its Upward Momentum, Employment Today

The GBP/USD had a range overnight of 1.3553-1.3620, Asia is trading around 1.3615. Cable looks to be trying to regain its momentum higher and break back through the 1.3600/50 area. A big week for event risk, unemployment today, then CPI and the BOE, and a sprinkle of FOMC just to add some spice. Should the market get the scenario it is hoping for from the FOMC the USD could begin to regain its momentum lower. This could potentially then see GBP/USD break out of its multi-month 1.3150 -1.3650 range and begin another leg higher. The initial target is the year's highs just below 1.3800, a sustained break above here would target the 1.4200/1.4300 area.

- MNI UK DATA PREVIEW: September 2025 CPI and Labour Release. Both labour market data and CPI data will have already been released to MPC members this morning, and both data releases are important for future monetary policy despite markets pricing in only around a 1/3 probability of a rate cut this year (and not fully pricing a 25bp cut until April 2026). We think that both Governor Bailey and Deputy Governor Ramsden are very much focused on the labour market print (probably a little more so than inflation). Along with Breeden, all three members are likely needed on board in order for another rate cut this year to materialize. We think that the market focus will switch back to AWE private regular pay data. Both the median and mean estimate from the previews that we have read is that this will fall to 4.65%Y/Y in the 3-months to July.

- MNI BOE WATCH: Seen Slowing QT And Holding Policy Rate. The Bank of England is widely expected to leave its policy rate unchanged at 4.0% at its September meeting and to keep its guidance intact while voting to ease back on gilt sales. The MPC vote split will, as ever, be in the spotlight with the most common view that it will be seven-two for no change, with independent members Swati Dhingra and Alan Taylor, who have both highlighted the fragility of economic activity rather than inflation persistence, voting for a 25bp cut. Taylor initially backed a 50bp cut in August.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 1.3600(GBP401m). Upcoming Close Strikes : 1.3250(GBP401m Sept 19) - BBG

- Data/Event: Unemployment, CPI Tomorrow, BOE Thursday

Fig 1: GBP/USD spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P