EURGBP TECHS: Monitoring Support At The 50-Day EMA

- RES 4: 0.8835 High May 3 2023

- RES 3: 0.8800 Round number resistance

- RES 2: 0.8769 High Jul 28 and the bull trigger

- RES 1: 0.8725/8751 High Oct 10 / High Sep 25

- PRICE: 0.8690 @ 16:35 BST Oct 16

- SUP 1: 0.8677/8656 50-day EMA / Low Aug 10

- SUP 2: 0.8633 Low Sep 15

- SUP 3: 0.8597 Low Aug 14 and key support

- SUP 4: 0.8562 50.0% retracement May 29 - Jul 28 upleg

The trend condition in EURGBP is unchanged, it remains bullish and recent weakness appears corrective. Support to monitor lies at the 50-day EMA, at 0.8677. It has been pierced, a clear break of this level would signal scope for a deeper retracement towards 0.8633, the Sep 15 low. Key trend support lies at 0.8597, the Aug 14 low. Key resistance and the bull trigger is at 0.8769, the Jul 28 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Busy Session For Euribor And Sonia Leans Toward Upside Tuesday

Tuesday's Europe US rates/bond options flow included:

- RXV5 127.50p, bought for 10 in 3k

- ERH6 98.125/98.25/98.4375/98.625c condor, bought for 2.5 in 5k

- ERM6 98.3125c, bought for 4 in 10k total

- ERX5 98.00/98.0625/98.125/98.1875c condor, bought for 0.75 in 3.5k

- ERZ5 98.00/97.875/97.75p ladder, sold at 3.75 in 5k

- 2RX5 97.6875/97.8125cs vs 3RX5 97.5625/97.6875cs, bought the 2yr for 1.75 and 2 in 18k total

- SFIZ5 96.15/20/25/30 call condor bought for 0.5 in 3k

- SFIZ6 97.25/97.75cs x5 vs 96.25p x1, bought the cs for 3 in 1.75k (8.75k x 1.75k)

- SFIZ6 97.25/97.75cs, bought for 4.25 in 3.75k

BONDS: EGBs-GILTS CASH CLOSE: UK Curve Belly Underperforms Pre-CPI

EGBs and Gilts traded mixed Tuesday amid key UK data releases and ahead of the Fed and BoE decisions.

- Yields picked up in morning European trade, with Gilts weighed down in particular by firmer-than-anticipated aspects of the latest UK labour market report.

- Yields would peak in early afternoon after US retail sales data printed much stronger than expected, but would subsequently subside over the rest of the European cash session, as a pullback in equities renewed a bid for core FI.

- DMO announced a reduction in the size of 30Y Gilt auctions, helping the UK curve flatten toward the end of the session.

- Elsewhere in data, Euro area industrial production increased in July in line with expectations, while the September German ZEW survey's expectations component was much stronger-than-expected.

- The German curve twist steepened, with the UK's twist flattening with underperformance in the belly. Periphery/semi-core EGB spreads were little changed on the day.

- Wednesday's European calendar highlight is the UK CPI release (MNI preview here) though there will be global interest in the Federal Reserve meeting after the close as well as multiple ECB speakers (including Lagarde), with the BoE decision looming Thursday.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.6bps at 2.002%, 5-Yr is down 1.1bps at 2.285%, 10-Yr is up 0.2bps at 2.693%, and 30-Yr is up 1.5bps at 3.275%.

- UK: The 2-Yr yield is up 1.1bps at 3.964%, 5-Yr is up 1.8bps at 4.079%, 10-Yr is up 0.6bps at 4.639%, and 30-Yr is down 0.9bps at 5.453%.

- Italian BTP spread up 0.1bps at 78.5bps / French OAT spread up 0.5bps at 79.6bps

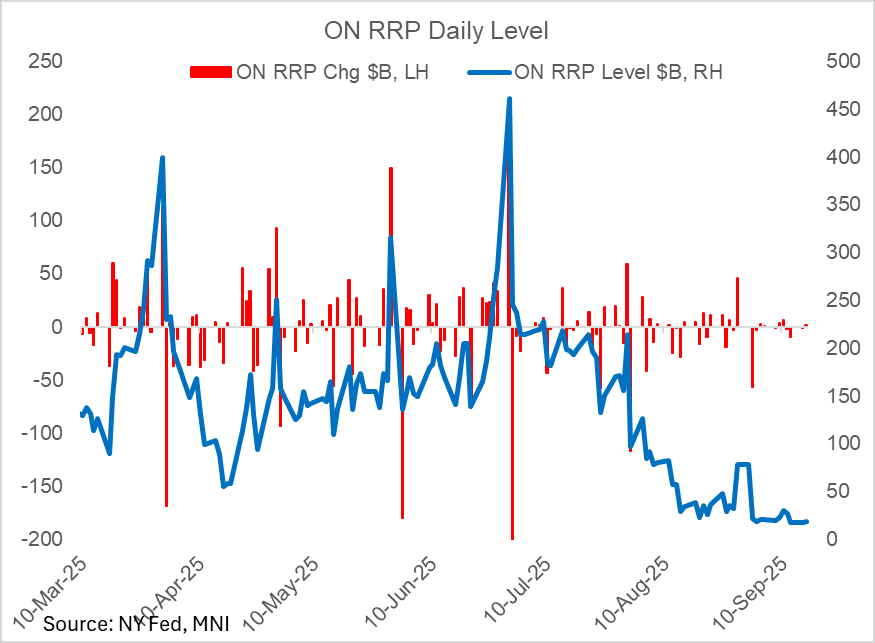

US TSYS/OVERNIGHT REPO: ON RRP Takeup Ticks Up From Multi-Year Low

Overnight reverse repo facility takeup ticked up for the first session in the last four, but remained near post-2021 lows.

- A $1.9B rise Tuesday from Monday's post-April 2021 low brought takeup to $18.8B.

- That left takeup still flatlining vs the habitual $100B+ levels seen prior to August, and is likely to remain around low levels until month-end when the usual month-/quarter-end pressures tend to increase takeup.