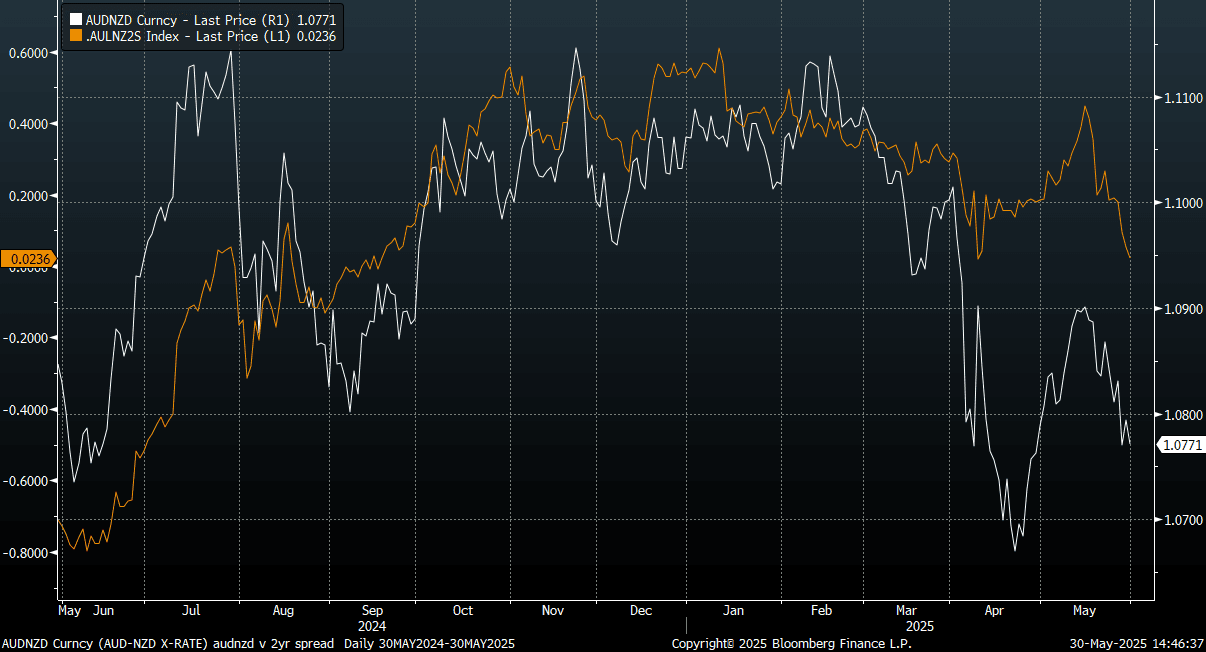

AUDNZD: AUD/NZD Down For 2nd Straight Week, AU-NZ 2yr Spread Near Flat

The AUD/NZD cross is holding near 1.0770 in latest dealings. We are tracking down 0.65% for the past week, the second consecutive weekly drop. The pair has moved lower in line with AU-NZ 2yr spreads. This spread is back close to flat, which is where we got to in early April. A clean break lower would take us back to levels last seen in Sep last year, see the chart below (the 2yr spread is the orange line).

- This saw the RBNZ cut25bps and lower the OCR outlook, but a follow up cut at the July meeting is not a done deal. In Australia we have had mixed data, with slightly stronger CPI but softer Capex and retail sales.

- Next week, greater focus will rest on Australia, with highlight including RBA minutes on Tuesday, the Q1 GDP on Wednesday.

- For AUD/NZD bears, downside focus is likely to rest on a retest back sub the 1.07 level. On the topside, the 20-day EMA is back near 1.0825, the 50-day close to 1.0855.

Fig 1: AUD/NZD Versus AU-NZ 2yr Spread

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

THAILAND: Growth Outlook Likely To Drive Another BoT Rate Cut

The Bank of Thailand (BoT) decision is later today and 17 out of 21 analysts on Bloomberg expect it to cut rates 25bp to 1.75% (see MNI BoT Preview). In its February statement, it said that it would be monitoring the impact of “trade policies of major economies”, Thai manufacturing activity and loan growth/credit quality. These factors and the stronger THB plus March’s earthquake signal that the central bank is likely to revise down its growth forecast from “around 2.5%”.

- The baht has strengthened around 8% y/y both against the US dollar and in trade weighted terms. This is likely to weigh on exports and the important tourism sector, which saw a 6.9% y/y decline in arrivals in February and is likely to be impacted by the earthquake.

- Q1 customs export growth improved to 15.1% y/y from 10.5% in Q4, but it is highly exposed to the US with 20% of 2024 exports going there worth 11.4% of its GDP, only second to Taiwan in the region. Its exposure to China is a lot less but not immaterial at 12.7% of exports and so they could be impacted directly and indirectly from US trade policy. April S&P Global manufacturing PMI prints on May 2 and may show early impacts on the region given Thailand’s exposure.

US proposed tariffs & country exposure to the US

Source: MNI - Market News/LSEG/US Treasury

- The manufacturing PMI eased to 49.9 from 50.6 in March and the Q1 average at 50.0 was down from 50.5 in Q4 and is signalling stagnation in the sector. Orders are soft with export orders contracting.

- March manufacturing production fell 0.7% y/y, this is not as weak as it has been over recent months, while capacity utilisation rose to 63.7 from 59.0, the highest in two years.

- BoT noted in February that “loan growth and credit quality showed signs of stabilising”. This has generally continued but there was a slight softening in lending.

Thailand manufacturing

FOREX: G10 Wrap - USD Trying To Bounce, Market Remains Bearish

The BBDXY has had an Asian range of 1220.99 - 1223.27, Asia is currently trading around 1222. Bloomberg - “ The European union has made tangible offers to Donald Trump's administration in an effort to return stability to the global economy, according to the bloc’s commissioner for international partnerships”. “The ECB’s Yannis Stournaras urged caution with any additional rate cuts due to global uncertainty, but said the deposit is expected to be trimmed to 2%”. US President Trump has spoken at a rally in Michigan, which marks his first 100 days in office. The speech was big on rhetoric, but policy related areas of interest for the market remained light.

- EUR/USD - Asian range 1.1355 - 1.1396, Asia is currently trading 1.1370. Intra-day support is around 1.1300, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3382 - 1.3415, the GBP momentum seems to be stalling towards the decent Weekly resistance around 1.3500. Intra-day support 1.3280 area.

- USD/JPY - Asian range 142.17 - 142.55, has drifted higher for most of the Asia session. On the day the 143 handle should once again offer supply, then more importantly the 145/146 area should once more offer good levels for sellers to reengage. A break back below 142.00 and the market will once again turn its focus on the pivotal 140.00 area.

- USD/CNH - Asian range 7.2619 - 7.2761, the USD/CNY fix printed lower again at 7.2014. Will need to get back above 7.3000 again to start thinking about moving higher again. The longer it stays below there the higher the chance of weaker longs being forced to pare back exposure.

- Cross asset : SPX -0.44%, Gold $3303, US 10-Year yield 4.16%, BBDXY 1222, Crude oil $59.68.

- Data/Events : French & Italian GDP, US ADP private jobs data, GDP, Chicago PMI, PCE and Home Sales.

Fig 1: USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg

GOLD: As Trade Tensions Ease, Gold Softens

- The push pull of the USD overnight as a stronger dollar saw gold soften.

- As market expectations around tariffs now easing permeated through investor thinking the dollar had a better night which makes gold’s purchase price more expensive

- Gold opened in Asia USD3,315.26 and declined steadily throughout the day to $3,303.06

- Gold continues to sit above all major moving averages with the nearest the 20-day EMA of $3,245.48

- The Thai Central Bank meets today and according to the BOT governor at a ceremony yesterday Thailand needs to brace for a ‘storm’ from the trade war and has increased their gold holdings accordingly.

- Gold ETF’s have experienced six straight days of outflows according to BBG.

- Gold remains one of the best performers year to date up 27% and the recent softening in prices appears likely driven by profit taking than a fundamental change in the outlook for bullion.