EQUITIES: Attention on the US Cash Open

Oct-02 13:23

- The Immediate focus during the European Open was on the EU Cash open, after Futures contract on both sides of the Pond printed new record high as traders boosted Rate Cut bets following Yesterday's US Data, brushing aside some of the Government shutdown Risks.

- The Emini is still printing fresh record high at present and while the calls don't look punchy, the US Open will also be set (like the EU) to gap higher.

- Opening Calls: SPX: 6,739.5 (+0.4%); DJIA: 46,482 (+0.1%/+41pts); NDX: 24,987.3 (+0.8%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US PREVIEW: ISM Aug Manufacturing Seen Recovering Slightly From Weak July

Sep-02 13:20

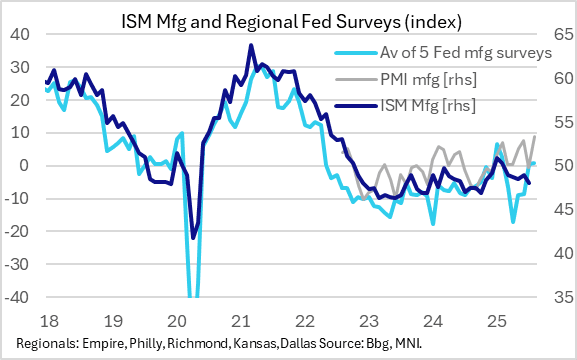

August's ISM Manufacturing PMI index (report out 1000ET) is seen by Bloomberg Consensus as showing a slight improvement to 49.0 from July's 48.0 (which was the lowest since October 2024).

- The report will be published shortly after the final release of August S&P Global Manufacturing PMI, which showed a surprisingly strong 53.3 in the flash reading. That was the highest since December and marked a 2nd consecutive improvement. There has been a divergence in the ISM vs PMI readings of late, with ISM sagging as PMIs hit new recent highs. Additionally, the MNI Chicago Business Barometer slowed 5.6 points to 41.5 in August, though the decline wasn't quite as stark based on ISM weights.

- However the theme of general improvement is evident in the regional Fed banks' manufacturing surveys, which showed a 5th consecutive month of improvement on aggregate after April's trough, albeit roughly steady from July. That said, it was a mixed bag region-by-region in August's surveys. The Kansas City Fed's reading was steady, while there were improvements in New York and Richmond, and deteriorations in Dallas and Philadelphia. One theme across most of the regional Feds (4 out of 5, Philly the exception) saw improvements in new orders, which may tip the balance toward a solid manufacturing ISM (consensus sees an uptick in ISM New Orders to 48.0 from 47.1).

- The Employment subcomponent (seen rising to 45.0 from 43.4 which was the lowest since June 2020) will garner attention ahead of Friday's nonfarm payrolls data.

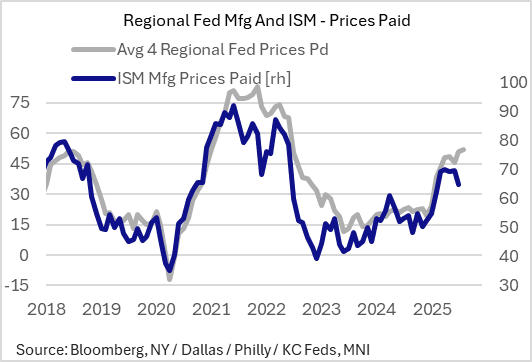

For Prices Paid, expectations are for a slight pickup to 65.0 from 64.8 prior. This looks to be on the low side versus the recent increase in regional Fed input prices indices: after a near 5-point pullback in July, we wouldn't be surprised by a rebound back toward the high 60s mark

- Admittedly the regional Fed data was mixed: Philly and Dallas Fed gauges pushed to multi-month highs, though KC and Empire moderated slightly. Our gauge below doesn't include the Richmond Fed which uses a different metric: a 12-month % chg lookback, which leaped to a 28-month high in the month. Additionally, the S&P Global flash PMI report noted that in August "the manufacturing cost rise was especially large, being the second-steepest since August 2022", suggesting a resumption of upside price pressures.

US TSY FUTURES: BLOCK: Dec'25 10Y Buy

Sep-02 13:16

- +10,000 TYZ5 112-01, buy through 112-00.5 post time offer at 0859:36ET, DV01 $654,000.

- The 10Y contract has finally rebounded after several Block buys this morning, TYZ5 trades 112-04 last (-12)

BTP: Large Calendar spreads go through

Sep-02 13:00

- Noted on the Eurex Roll, that the BTP was behind the pace, now some 22.72k spread trades in a 3 minutes Window.

- The BTP spread has been lifted in the past 30 minutes, and has moved from a 89 low to a 92 high at the time of typing.