EQUITIES: Heavy selling Flows in the Emini

Oct-02 13:55

- Looking at the Volume flow, it looks like some 100k lots went through on the way down in the Emini since the Cash Open.

- Surprisingly not seen any type of program orders in Cash Equities to help the move, this seems centered in Futures.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

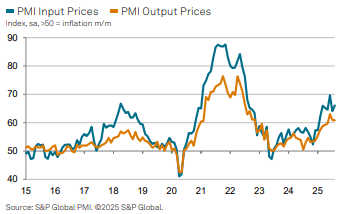

US DATA: A Still Strong Increase In Final August Mfg PMI Despite Lower Revision

Sep-02 13:52

- S&P Global US mfg PMI: 53.0 in Aug final (cons & prelim 53.3) after 49.8 in July.

- As such, it was revised modestly lower but is still the highest since May 2022 after a strong monthly increase.

Press release (link) highlights point to a similar story to that from the flash at first glance:

- “US manufacturing operating conditions improved to the greatest degree in over three years during August amid a surge in production and solid growth in new order books.”

- “Firms also took on workers to a greater degree amid evidence of capacity constraints. Inventory building in part fueled the upturn in output, with finished goods stocks rising to the greatest degree in over a year amid worries over prices and supply constraints.”

- “This was again linked to tariffs, which served to raise input costs steeply during August and, in turn, sharply drive up typical selling prices.”

BONDS: Core FI Futures Off Lows, US 5s30s Now Bear Flatter On Session

Sep-02 13:50

Global core FI futures have moved away from session lows over the past hour, with aforementioned block purchases in 10Y USTs helping the space stabilise. A ~1.5% pullback in crude oil futures may also be lending support.

- In the cash space, 10-year UST yields remain up 4.5bps today at 4.273%, albeit off session highs of 4.304%. Earlier bear steepening has given way to bear flattening in the mid/long-end of the curve, with 5s30s now -1.2bps today.

- Core FI was pressured through the European morning by a combination of fiscal/political (Japan and UK) and issuance (UK and Germany) factors, while today’s heavy post-Labour Day USD corporate issuance will have also weighed.

- In Europe, Gilts have faded earlier underperformance versus Bunds, with the 10-year Gilt/Bund spread now little changed on the session at 200bps. Outright Bund and Gilt yields are up ~4.5bps today, with both German and UK curves still leaning bear steeper.

- Markets will continue to have an eye on any potential headlines from the Fed Gov. Cook court case. US District Judge Jia Cobb on Friday asked Cook’s lawyers to file a brief today spelling out their arguments for why Trump’s firing of Cook was unlawful. This is a case that seems likely to ultimately end up in the Supreme Court.

- The US ISM manufacturing report is due at 1000EST/1500BST. The final S&P manufacturing PMI was revised down a touch to 53.0 (vs 53.3 flash).

EGB OPTIONS: Schatz Put Ladder

Sep-02 13:46

DUV5 107.20/107.10/106.90p ladder, sold at 3 in 4k.