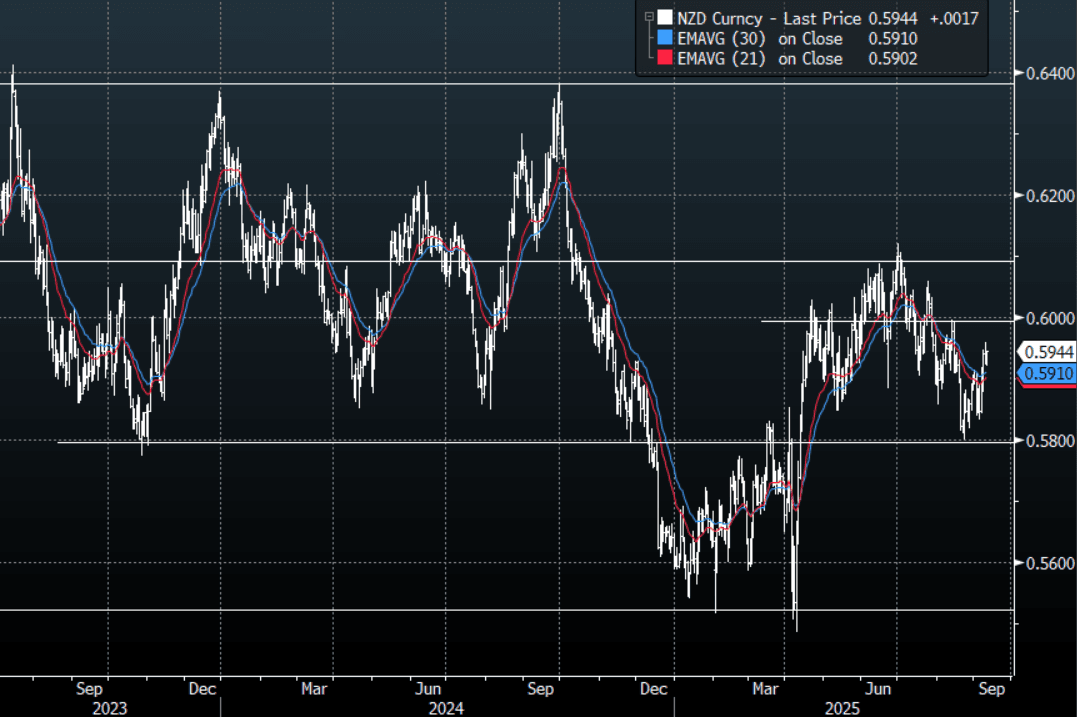

NZD: Asia Wrap - NZD/USD Bounces As Risk Moves Higher Into US Inflation Data

The NZD/USD had a range of 0.5921 - 0.5946 in the Asia-Pac session, going into the London open trading around 0.5945, +0.30%. US stocks are back at their highs even after record revisions to the payrolls data, nothing stops this train. The NZD has bounced into what should be the perfect zone to fade for bears, the price action for the USD though gives me pause. CFTC Data shows light positioning in a market that is struggling for a strong trend as we move back into the middle of the recent 0.5800-0.6100 range.

- MNI: RBNZ Leadership Woes Present Reform Opportunity. Suzanne Snively, a former board member and chair of the independent experts panel that led the 2017–22 RBNZ Act review, said the government may revisit the balance between RBNZ independence and ministerial control, with Finance Minister Nicola Willis likely to reopen debate over governance structures that were examined in the 2017–22 Act review.

- "NZ JULY NET MIGRATION ESTIMATE +2,060(Jun revised up to 1930 from 1670), NEW ZEALAND ANNUAL NET IMMIGRATION PICKED UP TO 13,066 IN JULY" - BBG

- On Thursday, Governor Hawkesby gives “brief remarks” at the Financial Services Council conference and again there will be no new information on the economy or the August MPC decision but there will be Q&A.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5800(NZD515m), 0.5870(NZD320m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225)..

- AUD/NZD range for the session has been 1.1108 - 1.1122, currently trading 1.1115. The Cross is consolidating around 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Uncertainty Over US Gold Tariffs Pressuring Market

Gold prices are 0.6% lower at $3378.7/oz during today’s APAC session. They fell to a low of $3367.79 before stabilising. The yellow metal has sold off as markets wait for clarification on the tariff-status of US gold imports. Stronger risk appetite with equities rallying is also pressuring bullion. In addition, President Trump and Putin are scheduled to meet on Friday in Alaska to discuss a peace deal for Ukraine potentially reducing geopolitical risks.

- Gold was exempted from US tariffs in April but last week officials stated that 100oz and 1kg bars would face import duties introducing increased uncertainty into the market and risking the seamless operation of trade, according to Bloomberg.

- The disappointing July US jobs data returned bullion close to the top of its recent range and corrections are still seen as corrective. Today’s trough remained above initial support at $3268.2, 30 July low. Initial resistance is at $3409.2, 8 August high.

- Silver is down at -0.7% to $38.08 off the intraday low at $37.924. The trend remains bullish though and the metal is trading above initial support at $36.216, 31 July low. Initial resistance is at $39.655.

- The US dollar is weaker (BBDXY -0.2%). Equities are rallying with the S&P e-mini up 0.2%, Hang Seng +0.2% and TAIEX +0.5% but KOSPI flat. Oil prices continue trending lower with WTI -0.7% to $63.43/bbl. Copper is flat.

- There are few events coming up on Monday. Italian July CPI and June trade are released later. US CPI on Tuesday will be the main focus of the week but Friday’s July retail sales and preliminary August Uni of Michigan consumer sentiment will also be monitored.

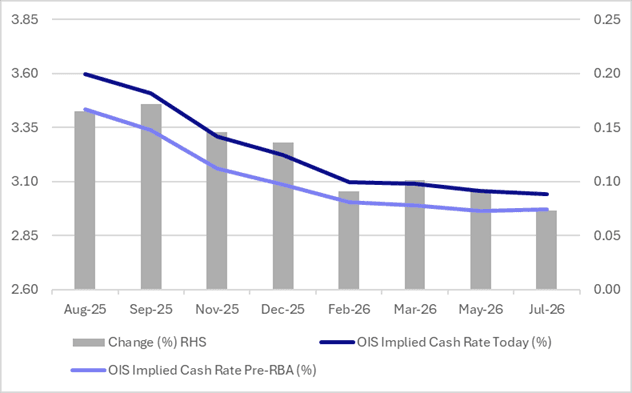

STIR: RBA Dated OIS Little Changed Ahead Of Tomorrow’s RBA Decision

At the time of writing, RBA-dated OIS pricing is little changed on the day across meetings ahead of tomorrow’s RBA Policy Decision.

- A 25bp rate cut this week is given a 97% probability, with a cumulative 62bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Notably, pricing remains 7-16bps firmer than levels before the July 8 RBA Meeting.

Figure 1: RBA-Dated OIS – Current Vs. Pre-RBA (July)

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Subdued Data Light Start To Week

NZGBs closed little changed, with benchmark yields flat t 1bp higher, after a subdued start to the trading week.

- Cash US tsys were closed during today’s Asia-Pac session, with Japan out for a holiday.

- Swap rates closed unchanged.

- With the next RBNZ meeting approaching (August 20), this week contains a number of high frequency releases that the MPC monitors and should give a sense for how the economy began Q3.

- July card spending is out Wednesday and while it is off its lows, growth has remained soft. There could be some payback in the month following the 0.5% m/m rise in June.

- On Friday, July monthly price series are released including food, travel, electricity and rents. Food and power price inflation have been trending higher while petrol and rents have been moderating.

- The July BNZ manufacturing PMI also prints on Friday. It returned to contractionary territory in May after five months signalling growth in the sector. In June, the pace of decline moderated with the index at 48.8 after 47.4.

- RBNZ dated OIS pricing closed unchanged across meetings. 23bps of easing is priced for August, with a cumulative 41bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$200mn of the 3.00% Apr-29 bond and NZ$250mn of the 2.75% Apr-37 bond.