EM CEEMEA CREDIT: Aramco: multi year agreement for drilling with Baker Hughes

Oct-24 12:05

"*BAKER HUGHES, ARAMCO TO EXPAND UBCTD OPS ACROSS SAUDI ARABIA" - BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT PAOF RESULTS: The PAOF for the 4.375% Mar-30 Gilt was not taken up.

Sep-24 12:02

- GBP1.1875bln have been on offer.

- This leaves GBP45.215bln of the gilt in issue.

STIR: Repo Reference Rates

Sep-24 12:00

- Secured Overnight Financing Rate (SOFR): 4.12% (-0.02), volume: $2.877T

- Broad General Collateral Rate (BGCR): 4.09% (-0.02), volume: $1.160T

- Tri-Party General Collateral Rate (TCR): 4.09% (-0.02), volume: $1.127T

- (rate, volume levels reflect prior session)

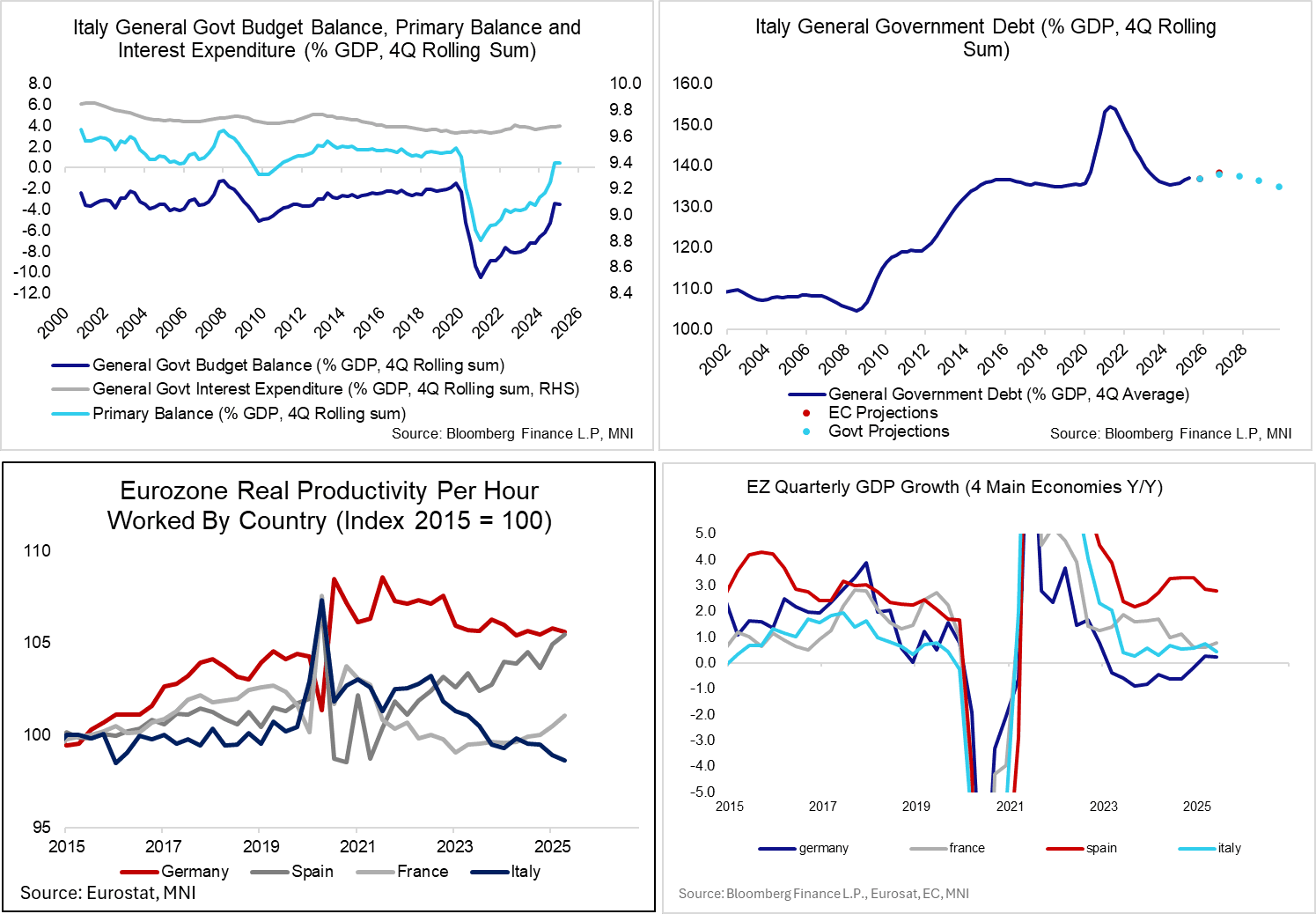

BTP: Domestic Macro/Fiscal Progress May Be Needed For Further Narrowing (2/2)

Sep-24 11:46

Additional Italy-Germany spread narrowing may require support from domestic macroeconomic/fiscal factors.

- Fiscal: Q2 Italian fiscal data is due on October 3. Recent fiscal consolidation has culminated in the first primary surpluses (on a 4Q rolling basis to GDP) since Q1 2020. Persistent primary surpluses are a necessary condition for the debt/GDP ratio to start easing in line with Government/EC projections from 2027. Looking ahead to the fiscal trajectory beyond this year:

- Bloomberg reported earlier this month that lower bond yields have created E13bln of extra fiscal space across 2025/26.

- Meanwhile, the Government is still trying to find a concrete way of raising revenue from the banking sector. It recently drafted plans to raise E1.5bln from banks through postponing tax deductions. This has historically been a politically difficult issue to navigate for Meloni.

- Furthermore, the FT reported this morning that the Government is considering a freeze in the retirement age of 67. The current retirement age is linked to life expectancy improvements, so has automatically crept higher over the past decade. Freezing the retirement age could put pressure on public finances, and worsen Italy’s existing demographic problems.

- Growth: Q2 real GDP growth was -0.1% Q/Q, and growth momentum has waned in recent quarters as the Superbonus tax credit tailwinds faded. However, analysts expect sequential growth rates to pick up in Q3 (0.1% Q/Q - flash print due October 30) and Q4 (0.2% Q/Q), which will be necessary for continued improvements in fiscal metrics as a % of GDP. That said, Italy’s weak productivity and demographic problems continue to limit potential growth rates.

- Ratings: Fitch upgraded Italy’s sovereign rating to BBB+ last week. S&P are due to provide a review on October 10th, but we don’t expect a ratings update given they already upgraded Italy to BBB+ in April. There’s more interest in Moody’s review on November 21. An upgrade from the current Baa3 rating appears likely, but we wouldn’t exclude a 2 notch upgrade to Baa1 to align with S&P and Fitch, particularly if the Q2 fiscal and Q3 flash growth data are encouraging.