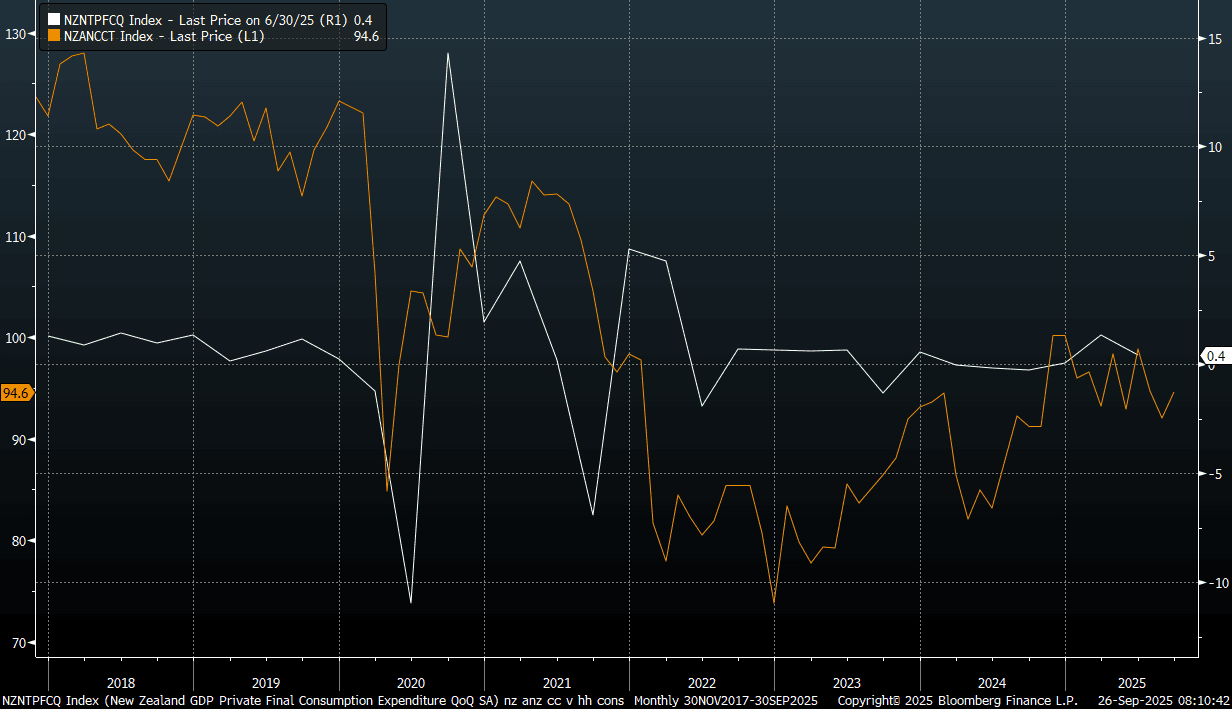

NEW ZEALAND: ANZ Consumer Sentiment Rises, But Still Sub Recent Highs

The ANZ New Zealand consumer sentiment index rose 2.8% in Sep, putting the index back up to 94.6 (from 92.0 in Aug). The improvement will be welcome, but we still sit off recent highs from late 2024. The chart below plots the sentiment index (the orange line) against the household consumption measure (q/q) from NZ's national accounts. So even after today's rise, it doesn't suggest a significant change to the broader consumer spending backdrop.

- In terms of the detail, the outlook for the economy 1yr ahead was -23, from -20 in Aug. For 5yrs ahead, the outlook improved to +6, from +3 prior. Buying a major household item was -11, versus -12 in Aug.

- Via BBG, ANZ post the release: "“Our view continues to be that the release of Q2 GDP marked peak pessimism. Easier monetary policy is starting to feed through, and we expect the economy to put in a markedly improved performance over the next 12 months than the last – though that isn’t saying a lot.”

Fig 1: NZ ANZ Consumer Confidence Against Q/Q Household Consumption Growth

Source: ANZ/Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

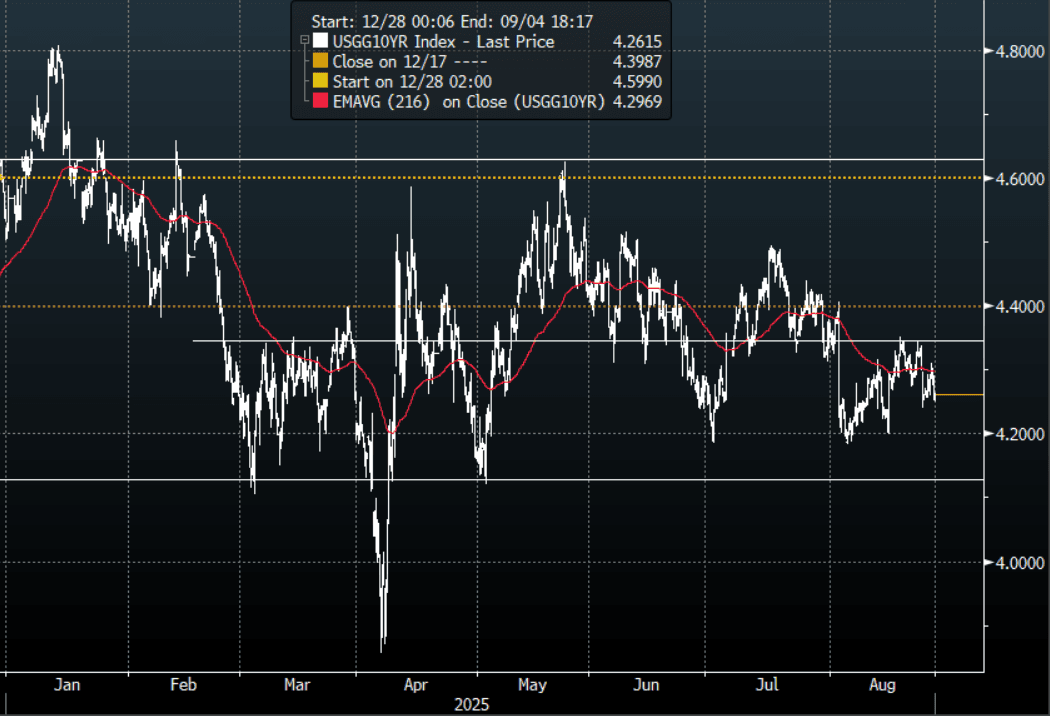

US TSYS: Yield Curves Steepen On Challenge To Fed Independence

TYU5 reopens at 112-05, down 0-01+ from closing levels in today’s Asia-Pac session.

- Overnight the US 10-year yield had a range of 4.2498% - 4.3101%, closing around 4.275%.

- Treasury yields ended mixed overnight; the front-end extended lower but the US 30-Year yield rose, this saw the yield curve extend higher again(2s10s +3.10 at 58.049, 5s30s +7.15 at 117.437).

- MNI Federal Reserve Statement: Governors Can Only Be Removed "For Cause". A Federal Reserve statement addressing the Gov Cook situation indicates that the Fed's position is that Board Governors can only be removed "for cause", and that while Cook "will promptly challenge this action in court and seek a judicial decision that would confirm her ability to continue to fulfill her responsibilities", the Fed will "abide by any court decision".

- Bloomberg - “Lawyer for Fed’s Cook Says Will File Lawsuit Challenging Firing: “President Trump has no authority to remove Federal Reserve Governor Lisa Cook,” Cook’s lawyer, Abbe David Lowell, says in a statement. “His attempt to fire her, based solely on a referral letter, lacks any factual or legal basis,” Lowell says of Trump. “We will be filing a lawsuit challenging this illegal action,” Lowell writes.”

- 10-Year Yields found buyers above 4.30% again overnight. While the 4.35% area continues to hold, bounces should be met with demand, with the 30-Year taking the brunt of the selling related to challenging the Fed independence. First target is the recent lows around 4.18% then the bottom of the range towards 4.10% comes back into focus.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

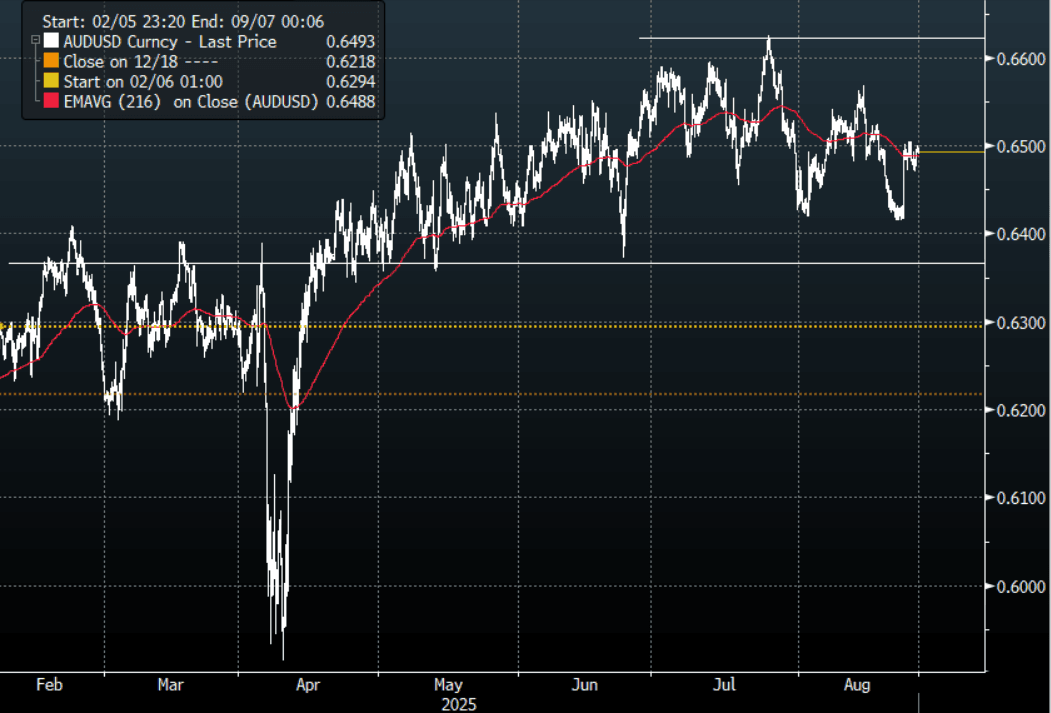

AUD: AUD/USD - Consolidates Around 0.6500, Month-End Approaches

The AUD/USD had a range overnight of 0.6470-0.6501, Asia is trading around 0.6490. US equities once again found buyers on the dip and the USD traded a little soft. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 and will need a clearer direction from both the USD and risk to embark on a decent move in either direction. We are approaching the corporate month-end so there could be some demand for USD today or tomorrow which is worth looking out for.

- (Bloomberg) - “Australia’s July CPI print is set to show inflation ticking up to 2.3% year-over-year, still toward the lower end of the RBA’s 2%-3% target band. The data should support expectations of another 25-bp rate cut in September, according to Bloomberg Economics.”

- “Australia’s corporate regulator said it will boost surveillance of private markets, with focus areas including insider trading and systemic compliance failures by large financial institutions.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD695m). Upcoming Close Strikes : 0.6400(AUD571m Aug 28), 0.6500(AUD782m Aug 29), 0.6455(AUD555m Sept 1) - BBG

- CFTC Data last week shows Asset managers continue to add to their shorts -72904(Last -67449), the Leveraged community though again reduced their own shorts -7818(Last -10121).

- Data/Event: Westpac Leading Index, CPI, Construction Work Done

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: US Crude & Product Inventories Lower Last Week

Bloomberg reported that US crude inventories fell 1mn barrels last week with a 500k drop at Cushing, according to people familiar with the API data. Products were also lower with gasoline down 2.1mn and distillate 1.5mn. The official EIA data is out on Wednesday.