EU BASIC INDUSTRIES: Amcor: 4Q25 Results

(AMCR; Baa2/BBB/BBB+)

Credit neutral.

• Net sales was below street consensus at $5.1B ($5.2B est.), was +43% YoY in constant currency and +1% YoY organically.

• EBITDA missed street estimates by 5% and grew by 43% YoY. Margins expanded by 6ppts to 22%.

• FCF was $599M compared to $629M in the prior year quarter, and share repurchases were modest.

• Gross and net leverage ended the quarter at 6.4x and 6.1x, respectively.

• Reiterated previously announced total synergy of the Berry acquisition of $650M by the end of fiscal 2028. $260M expected in fiscal 2026. Berry’s North America Beverage business identified for potential sale.

• FY26 FCF guidance was above estimates at $1.85B ($1.6B est.).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

INFLATION: US And Canada Y/Y CPI Expected To Pick Up In June

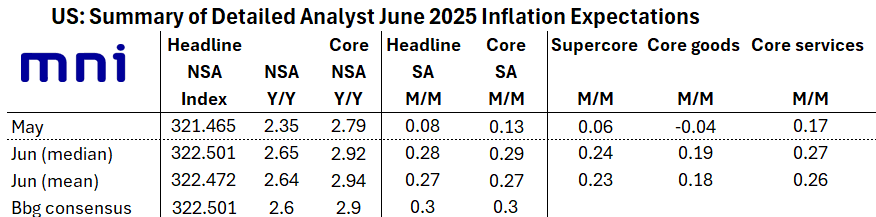

It's North American inflation day, with the US and Canada reporting CPI at 0830ET:

In the US, consensus sees core CPI inflation at a seasonally adjusted 0.3% M/M in June on a rounded basis, but with sizeable risk of undershooting at 0.2% (MNI median unrounded estimate at 0.24% M/M /average 0.25%). This would mark an acceleration from 0.13% M/M in May, with core services ticking up and core goods

more than reversing May’s unexpected M/M deflation. Y/Y core is seen up to 2.9% from 2.8%.

- Headline CPI meanwhile is seen at 0.3% M/M or 0.25% M/M unrounded after 0.08% in May, amid a bounce in gasoline-driven energy prices, with Y/Y up to 2.6-2.7% from 2.35% prior.

- Consensus table below - our full US preview is here, including category-by-category details.

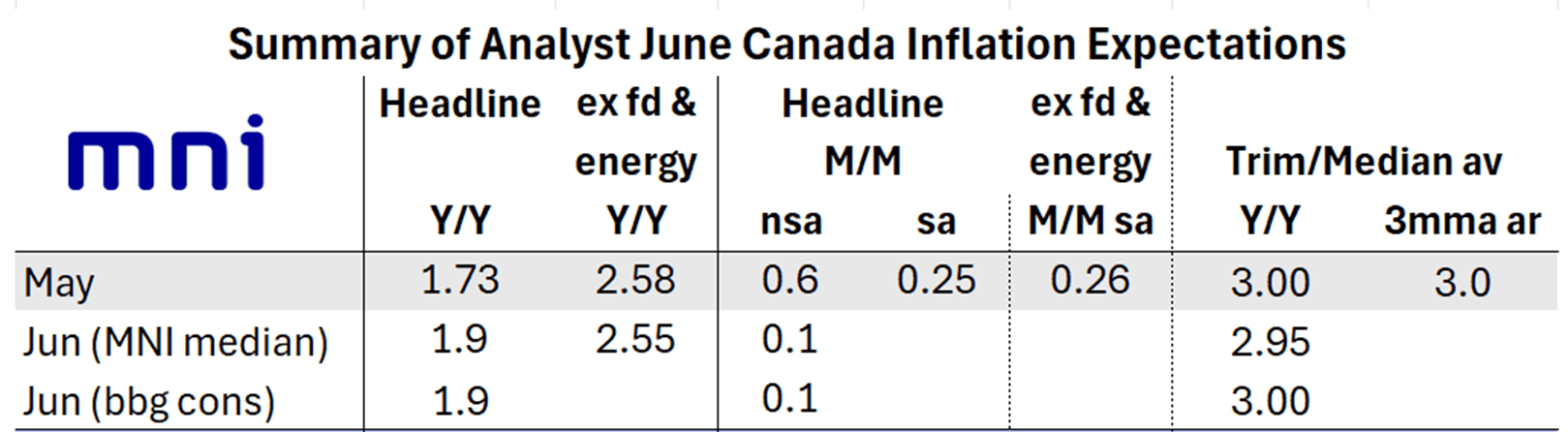

In Canada, Headline CPI is seen rising to 1.9% Y/Y in June, up from 1.73% (unrounded) in May, which would mark a 3-month high. On a M/M non-seasonally adjusted basis, CPI is seen pulling back to 0.1% from 0.6% (0.55% unrounded) prior. MNI's summary of analyst consensus is below.

- More importantly from the Bank of Canada's perspective, the average of trim/median inflation is seen basically steady, at 2.95% (MNI median, 3.00% BBG consensus), vs 3.00% in May. More specifically, Median is seen coming in at 2.9% with Trim at 3.0%. Even a soft reading is unlikely to convince the BOC to cut on July 30, though.

US: MNI POLITICAL RISK - Trump Continues Hawkish Pivot On Russia

Download Full Report Here

- President Donald Trump is eyeing investment deals at today's inaugural Pennsylvania Energy and Innovation Event.

- Former NSA Mike Waltz's appearance before the Senate Foreign Relations Committee today offers Democrats a rare chance to grill a Trump administration insider.

- House Ways and Means Republicans will meet USTR Jamieson Greer this morning and Commerce Secretary Howard Lutnick on Wednesday for trade negotiation updates.

- The EU has finalised a list of countermeasures targeting goods worth around USD$85 billion, but will refrain from retaliation while negotiations are ongoing.

- Treasury Secretary Scott Bessent said he expects to meet his Chinese counterpart in the coming weeks.

- Japanese officials say Tokyo has no plans for tariff retaliation.

- Senate Majority Leader John Thune (R-SD) could delay a first procedural vote on Trump’s USD$9.4 billion rescissions package.

- White House NEC Director Kevin Hassett, a close Trump ally, is firming as favourite to become the next Fed Chair.

- Trump increased pressure on Russia, announcing plans to send defensive and offensive weapons to Ukraine via NATO partners and issuing Russian President Vladimir Putin a 50-day ultimatum to reach a peace deal with Ukraine, or be hit by “very severe tariffs”. Thune said he would hold off on advancing a bipartisan Russia sanctions bill, in light of Trump's statement.

- Poll of the Day: Trump’s approval ratings ticked back up despite a turbulent week for his administration.

Full Article: US DAILY BRIEF

SEK: EURSEK Narrowing Gap To Resistance At July 7 High

SEK is once again underperforming the G10 basket, with EURSEK up 0.45% and narrowing the gap to resistance at 11.2784 (Jul 7 high). Clearance of this level would see the cross fully unwind the June flash CPI-induced fall, suggesting markets do not consider the print a serious impediment to future Riksbank easing. We wrote yesterday that an August Riksbank cut still can’t be fully ruled out, with another inflation report still due on August 7 (flash print, final on 14th) and growth data printing softly in recent months.

- Clearance of the Jul 7 high in EURSEK would expose 11.3203, the 76.4% retracement of the March – April selloff.

- This morning, 5-year ahead money market participant CPIF inflation expectations fell two tenths to 1.8% - the lowest since July 2021. The survey was conducted between June 30 – July 6, so did not include the stronger-than-expected flash June inflation report. The Riksbank will likely need to see several 5-year prints below the 2% target to become concerned about a de-anchoring of inflation expectations, not just in the monthly money market participant survey but also the broader quarterly survey (which includes social partners’ expectations).

- The Swedish macro calendar thins out for the remainder of this week, but we will still pay attention to the Public Employment Service’s June labour market report tomorrow – particularly data on redundancies and vacancies.