AUD: A$ Mid-Range Performer, AUDUSD Little Changed

AUDUSD range traded through most of Wednesday to be flat on the day at 0.6613 but is still up 1.1% this week as the US dollar has struggled as hopes that a government shutdown would be avoided faded. The USD BBDXY finished slightly lower but recovered from its post ADP jobs decline as the September ISM was slightly better than expected. AUDUSD is currently trading around 0.6614.

- AUDUSD reached a high of 0.6629 after ADP jobs printed down 32k. This is now the initial resistance level with key resistance at 0.6707, 17 September high. The uptrend remains intact. Initial support is at $0.6527.

- The yen outperformed most of the G10 leaving AUDJPY down 0.6% to 97.266. It is currently at 97.24. The solid Q3 Tankan survey along with a more hawkish tone to BoJ minutes supported the yen.

- AUDNZD reached a peak of 1.1418 on Tuesday but then trended lower yesterday. The pair finished down 0.4% to 1.1369 off the intraday low of 1.1356 and is now around 1.1369.

- AUDEUR rose to a high of 0.5641 and then stabilised. The pair was slightly higher at 0.5638 and is now at 0.5636. AUDGBP fell 0.2% to 0.4907 off the intraday low of 0.4891.

- Equities were stronger with the S&P up 0.3% and Euro stoxx +0.9%. Oil prices fell with Brent -0.9% to $65.42/bbl. Copper rose 0.8% and iron ore is just under $104/t.

- Today August trade and household spending print with the surplus forecast to narrow and consumption to rise 0.3% m/m. The RBA’s Financial Stability Review is published at 1130 AEST.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

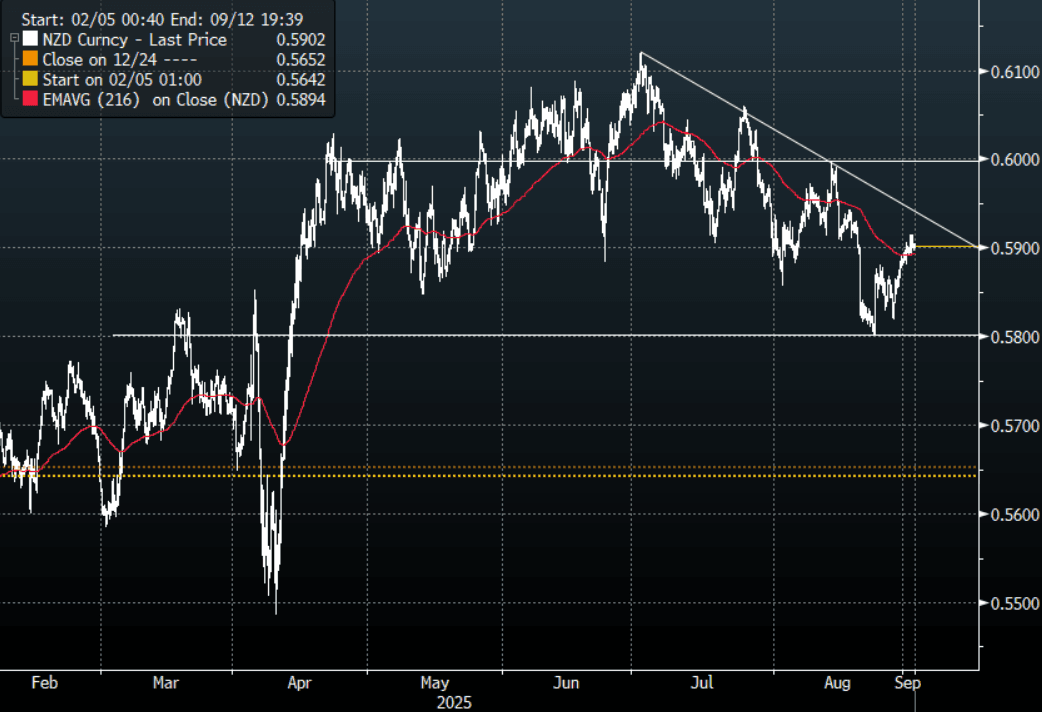

NZD: NZD/USD - Probing Above 0.5900

The NZD/USD had a range overnight of 0.5890 - 0.5915, Asia is trading around 0.5900. The NZD is consolidating around 0.5900. The NZD has bounced off its support toward 0.5800, sellers should continue to be around looking to fade the move back towards the 0.5950/0.6000 area initially. Should the USD break lower and gain momentum this would complicate this trade and then it would be prudent to rotate the NZD shorts into the crosses. US Futures have opened slightly firmer this morning, E-minis +0.15%, NQU5 +0.15%.

- MNI BRIEF: SCO Development Bank To Boost Infrastructure - FM. The establishment of a Shanghai Cooperation Organisation Development Bank will help boost infrastructure and socio-economic development amongst member states and the wider region, China’s Foreign Minister Wang Yi told reports on Monday. The establishment of an energy cooperation platform will be open to all SCO members and will support sustainable development to the region, Wang added.

- Bloomberg - “Dollar Vulnerable to Slide With Fed Rate-Cut on Menu. The US dollar is likely to sag as expectations build for Friday’s payrolls data to cement bets on Federal Reserve rate cuts. Uncertainty about the central bank’s independence, and about the legal standing for tariffs, add to the reasons for a weaker greenback.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5700(NZD500m). Upcoming Close Strikes : 0.5700(NZD384m Sept 3) - BBG

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -4743(Last -3198), the Leveraged community have almost completely exited their short -225(Last -4004).

- Data: Terms Of Trade Index

Fig 1: NZD/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Yields Firmer, Led By The Back End, Terms Of Trade Out Shortly

NZGB yields are biased higher in the first part of Tuesday trade, led again by the back end. The 2yr NZGB yield was little changed and last near 2.965%, while the 10yr is up close to 2bps, tracking towards 4.38%.

- US Treasury futures dealt mildly cheaper at the early close for Labor Day on Monday, after an unsurprisingly quiet session. Sell-off cues were taken from some mild weakness in EGBs on supply grounds. We have re-opened this morning with a negative bias, which may be aiding the NZGB yield backdrop.

- For 2yr NZGB, focus will remain on whether we can re-capture the 3% handle. Beyond this, pre-RBNZ highs were above 3.20%. For the 10yr yield we close to 4.50% in terms of pre RBNZ highs.

- The NZ 2yr swap rate is edging higher, last around 2.74%.

- Q2 terms of trade data are out today, which includes trade volumes, are released on Tuesday and expected to rise 1.9% q/q.

US TSYS: Futures Edged Lower On US Holiday

TYZ5 reopens at 112-12, down 0-04 from closing levels in today’s Asia-Pac session.

- Overnight the TYZ5 contract had a range of 112-09+ - 112-13, closing around 112-11+ down 0-05.

- US (MNI): Trump May Declare National Housing Emergency In Fall - Bessent. US Treasury Secretary Scott Bessent told the Washington Examiner that President Donald Trump may declare a 'national housing emergency' this fall to address rising house prices. The Washington Examiner notes that there hasn't been a national housing emergency declared since the 2008 recession.

- Bloomberg: “Wall Street will be bracing for a crucial stretch, with jobs numbers, inflation data and the Fed’s rate call all landing within the next three weeks, and swaps markets are pricing in roughly 90% odds that the Fed will cut them at this meeting.”

- 10-Year Yields continue to find supply toward the 4.20% area, which signals the range might continue to dominate. A break of the recent lows around 4.18% would bring the bottom of the range towards 4.10% back into focus.