EM CEEMEA CREDIT: Abu Dhabi National Energy Co: new TL facility, neutral

(TAQAUH; Aa3/NR/AA)

• Neutral for credit, the new AED8.5bn Term Loan addition is supportive for liquidity. For context, as of end of Q2, TAQA had UF of close to AED12.5bn, with net cash & equiv. of close to AED7.5bn.

• "TAQA secures AED8.5 billion term loan to advance growth strategy" – Emirates News Agency/ BBG

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Slightly Bear Steeper Following Higher-than-expected Borrowing Figures

The Gilt curve has lightly bear steepened, with yields 2-3bps higher across the curve following this morning’s higher-than-expected PSNB figure for June. 10s30s is 0.3bps steeper at 82.7bps, but remains below this month’s ~85bps high.

- Yields remain below last Friday's closing levels, following a broad-based core FI relief rally and well received long-end BOE APF operation yesterday. However, the fiscal data is yet another example of the difficult situation facing Chancellor Reeves and the Labour Party.

- Gilt futures are -19 ticks at 91.59. Yesterday’s strong gains are considered corrective, with a bear cycle still intact. Initial firm resistance is the 20-day EMA at 91.97. Should this morning’s selloff extend, focus will be on support at 91.08, the July 18 low.

- BOE Governor Bailey is scheduled to testify on Financial Stability at the TSC today (1015BST). Any comments around the labour market will be in focus, following last week’s data and his recent dovish interview with the Times.

- This morning, the DMO will kick off issuance for the week with GBP1.7bln nominal of the 1.125% Sep-35 linker on offer via auction.

- Yesterday, the DMO noted that two Gilt lines (the 4.125% Jan-27 Gilt and the 0.375% Mar-62 linker) will be cancelled following a donation to the Donations and Bequests Account made during the financial year ending 31 March 2025.

- Broader UK focus remains on Thursday’s July flash PMIs.

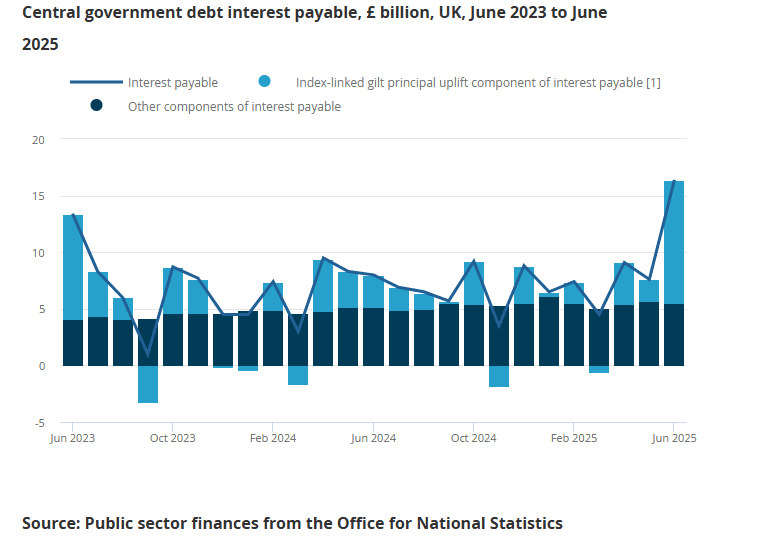

UK FISCAL: Higher Linker Interest Payments Push PSNB Higher In June

Looking a little more at this morning’s public sector finance data, the GBP20.7bln PSNB figure for June was GBP6.6bln more than June 2024 and “the second-highest June borrowing since monthly records began in 1993, after that of June 2020”, according to the ONS. The OBR projected a reading of GBP17.1bln in March 2025, with BBG consensus standing at GBP17.5bln.

- Central government current receipts were GBP5.7bln more than a year ago at GBP86.6bln. Following the change in employer NI contributions from April 2025, compulsory social contributions were up GBP3.1bln Y/Y to GBP17.4bln.

- Expenditures rose a more notable GBP12.4bln versus June 2024, totalling GBP97.1bln. This was largely due to a GBP8.4bln rise in interest payable to GBP16.4bln - GBP2.4bln above the OBR’s projection. There was a 1.7% rise in RPI between March-April 2025, which was reflected in increased linker interest payments in June (“capital uplift”).

SILVER TECHS: Bullish Price Sequence

- RES 4: $40.285 - 1.618 proj of the Apr 7 - 25 - May 15 swing

- RES 3: $40.000 - Psychological round number

- RES 2: $39.655 - 1.500 proj of the Apr 7 - 25 - May 15 swing

- RES 1: $39.132 - High Jul 14

- PRICE: $38.834 @ 08:07 BST Jul 22

- SUP 1: $37.271 - 20-day EMA

- SUP 2: $35.942 - 50-day EMA

- SUP 3: $33.967 - Low Jun 3

- SUP 4: $32.615 - Low May 22

Trend signals in Silver are unchanged and continue to point north. On Jul 11, Silver cleared a key short-term resistance at $37.317, the Jun 18 high. This confirmed a resumption of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a clear uptrend. Sights are on the $39.655 next, a Fibonacci projection. On the downside, initial support to watch lies at $37.271, the 20-day EMA.