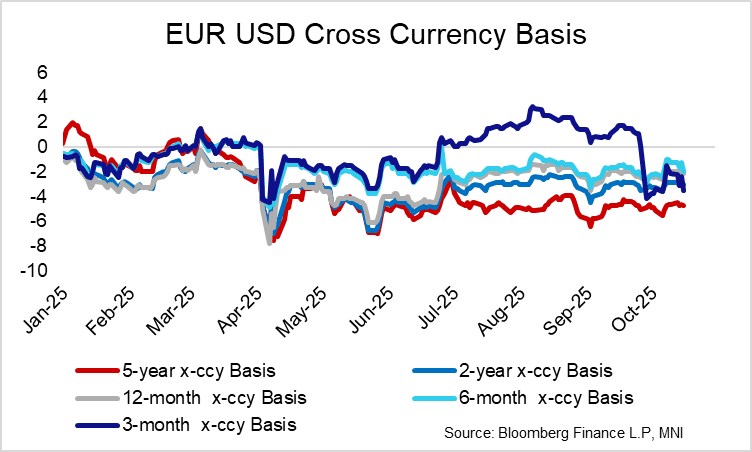

BASIS: 3-month EUR/USD X-ccy Basis Has Been Negative Since End-September

Oct-16 14:48

With US funding market pressures becoming increasingly prevalent in recent days, we highlight that the 3-month EUR/USD x-ccy basis has returned to negative territory since the end of September, after a brief time above 0 through the summer.

- The USD premium implied by the negative basis is in line with post-GFC norms, so it was notable that the 3-month basis diverged from longer tenors during the summer.

- This morning, take-up of the Fed’s Standing Repo Facility was $8.35bln, above the $6.75bln borrowed yesterday. Meanwhile, SOFR rose 10bps to 4.29% yesterday.

- Today, Fed Governor Waller appeared to agree with the conclusion of QT soon, as suggested by Chair Powell on Tuesday. See our earlier commentary for more on Waller’s comments.

- Alongside building US money market pressures, ECB QT continues to run steadily in the background, with no clear signs of stress - excess liquidity remains close to E2.6trln. ECB Executive Board member Schnabel also noted recently that "excess liquidity has come down somewhat more slowly than expected as a result of some autonomous factors".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: GBPUSD Topside Momentum Builds Following Technical Break

Sep-16 14:38

- Neither UK labour market data or US retail sales figures have been able to upset the underlying FX trends on Tuesday, emphasised by GBPUSD making further inroads above 1.36, following a significant technical breakout this week.

- Today’s broad dollar weakness remains the dominant driver of the move, however, sterling positioning dynamics linked to pessimism surrounding the UK fiscal story may be exacerbating the latest leg higher for cable. Immediate resistance comes in at 1.3681, the July 4 high. Above here, 1.3789 remains the key resistance for the pair, the July 1 high.

- UK CPI data is scheduled tomorrow morning, before Thursday’s BOE decision which should keep GBP very much in focus over the coming sessions.

- Barring a big downside shock to tomorrow's August CPI data, ING think Thursday's BoE event risk could be sterling positive. They have a year-end target for GBPUSD at 1.38, which could be met a little sooner than expected.

GILT AUCTION PREVIEW: Step down in 30-year gilt auction size

Sep-16 14:36

- Note that is a step down in the size of 30-year gilt auctions - with the 4.375% Jul-54 gilt sold for GBP2.25bln nominal at the last auction in April. That equated to GBP1.9bln in cash terms.

- The 5.375% Jan-56 gilt launched via syndication in May and this is the first reopening.

- 10s30s gilts had been flattening today and has flattened another 0.15bp on the auction size announcement.

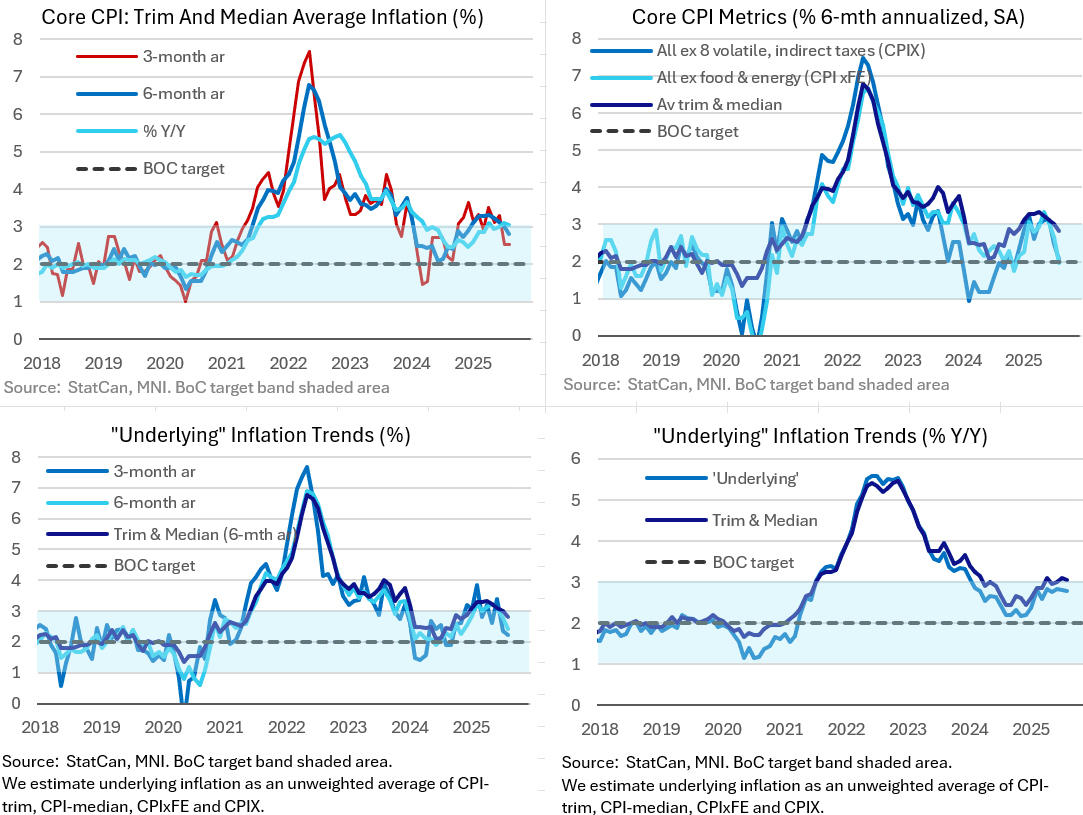

CANADA DATA: Moderating Core Inflation Trends Keep BOC On Track To Cut Wednesday

Sep-16 14:32

August's Canadian CPI data will not present an obstacle to the BOC cutting its benchmark rate on Wednesday by 25bp to 2.50%. Headline CPI printed in line with expectations, ticking up to 1.9% Y/Y after 1.7% in July. In fact, on an unrounded basis, it was on the low side of expectations: 1.85% after 1.73%. And it kept the rate below 2% for a 5th consecutive month.

- While that will keep Bank of Canada officials persuaded that price pressures are under control, their closely-watched trim/median average measure continues to show little disinflationary progress, at an in-line-with-expectations 3.05% Y/Y, trim 3.0% and median 3.1% (prior trim/median was revised up to 3.10% from 3.05% prior so technically this was a deceleration).

- Other Y/Y core measures were somewhat mixed. Ex-food and energy inflation (2.44% Y/Y unrounded) was the lowest since March (2.50% prior), while the measure of CPI ex-8 most volatile/indirect taxes was relatively steady at 2.63% (2.57% prior). Ex-mortgage interest CPI was 1.73% Y/Y, up from 1.54% prior for the highest since March.

- When we look at the sequential measures, these too were relatively tame. All-items CPI rose 0.18% M/M on a seasonally-adjusted basis (0.12% prior), with the NSA reading of -0.06% M/M the joint-softest of the year (0.30% prior).

- Ex-food and energy rose 0.13% M/M (0.06% prior). Trim decelerated to 0.19% from 0.23%, with median up to 0.23% from 0.14% (which had been a 12-month low).

- This meant that the trend rates of major aggregates moderated. Ex-food and Energy ticked down to 1.6% on a 3-month moving average annualized rate basis, the lowest since September 2024, with the 6-month at 2.0%. Ex-8 most volatile/taxes was steady at 2.3% on the 3M but fell to a 9-month low 2.1% on a 6M basis. And while the trim/median average 3mma was steady at 2.5% (a joint-10 month low), the 6-month measure was a 9-month low 2.8%, printing below 3% for the first time this year.

- We will turn to the component details in a separate note but the details showed deceleration in shelter and core goods prices (durable goods Y/Y softened), with the only major upside concern being in non-shelter services which ticked higher.

- For the BOC, the OIS rate path now shows a fully-priced September cut, with about 4bp added across the implied cuts though next summer (a 2nd 25bp cut is priced through January 2026, vs March prior to the CPI release).

- The closest we got to a view change post-CPI was RBC, which came into this week as the only major Canadian institution eyeing a hold this week, a view it appears to maintain while acknowledging it's a close call: "The BoC will also have to consider upside inflation risks from sticky core inflation, resilient consumer spending, and planned fiscal stimulus that is likely more effective at addressing the targeted economic impact of trade-related disruptions than interest rate cuts. Today’s inflation report does little to sway that assessment, and we continue to think the Bank of Canada’s decision tomorrow will be a close call between a 25 basis point cut to the overnight rate and a hold.